COVID-19 made it tough to analyze the medical industry, further blurring this pharma giant’s real performance

The medical industry has been an interesting one to invest in this year. Hospitals have been overwhelmed, but many elective procedures have been postponed this year. It’s difficult to paint the industry with a broad brush as a result.

Due to fewer people going to the hospital for check-ups and elective procedures, today’s stock performed poorly before news about a vaccine broke. However, Uniform Accounting shows why this may be unfounded.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We have repeatedly talked about how the pandemic is affecting myriad industries.

Some are more obvious, like the air travel industry. The industry has been crushed by the pandemic as demand has decreased.

The restaurant industry has also faced challenges as indoor dining is difficult during the pandemic. As we have discussed, this has caused Americans to cook more at home.

The pandemic has also disrupted the REIT industry, as businesses have been eliminating unneeded office space.

Another industry that has changed this year is the medical industry. One of the greatest dangers of the pandemic is the overcrowding of hospitals, making it difficult to treat patients who have contracted the coronavirus.

Due to this capacity issue and the fear of contracting the virus, many people have deferred regular check-ups and elective procedures. Some people have also chosen to forego medical advice for smaller issues.

This has not only affected hospitals, but pharmaceutical companies as well. With fewer prescriptions being written up, investors have been weary of firms in this supply chain.

Specifically, investors have been worried about AbbVie (ABBV). Spun-off from Abbott Laboratories (ABT) in 2013, AbbVie is a research-focused biopharmaceuticals company. The firm focuses on a variety of conditions and diseases, including blood cancer, Parkinson’s, and cystic fibrosis.

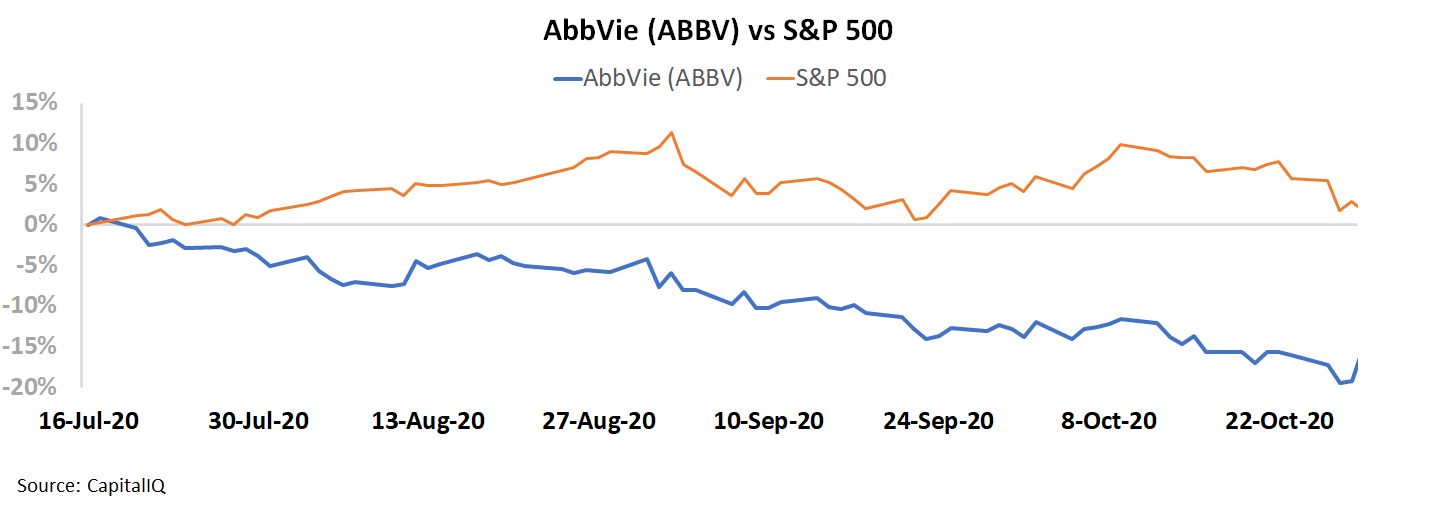

Driven by the slowdown in non-COVID medical care, the market was worried about AbbVie before news regarding the vaccine came out. Between mid-July and when the vaccine news broke, AbbVie was down over 15% while the S&P 500 was roughly flat.

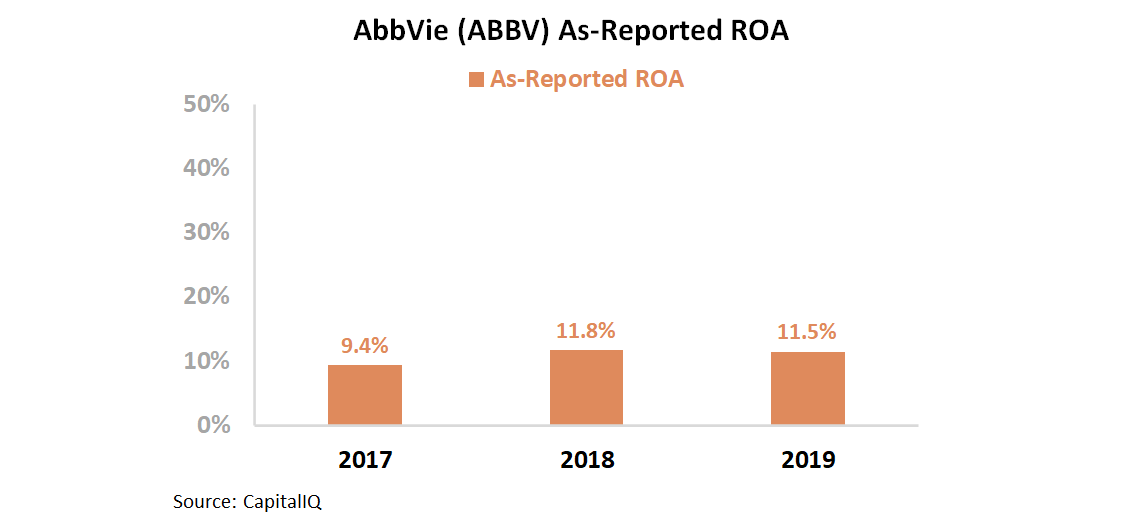

After all, as-reported ROA was already weak for the company. This is surprising, given the sheer amount of intellectual property the firm has under its control.

As-reported ROA appears to be only near corporate averages, ranging between 9% and 12% from 2017 to 2019.

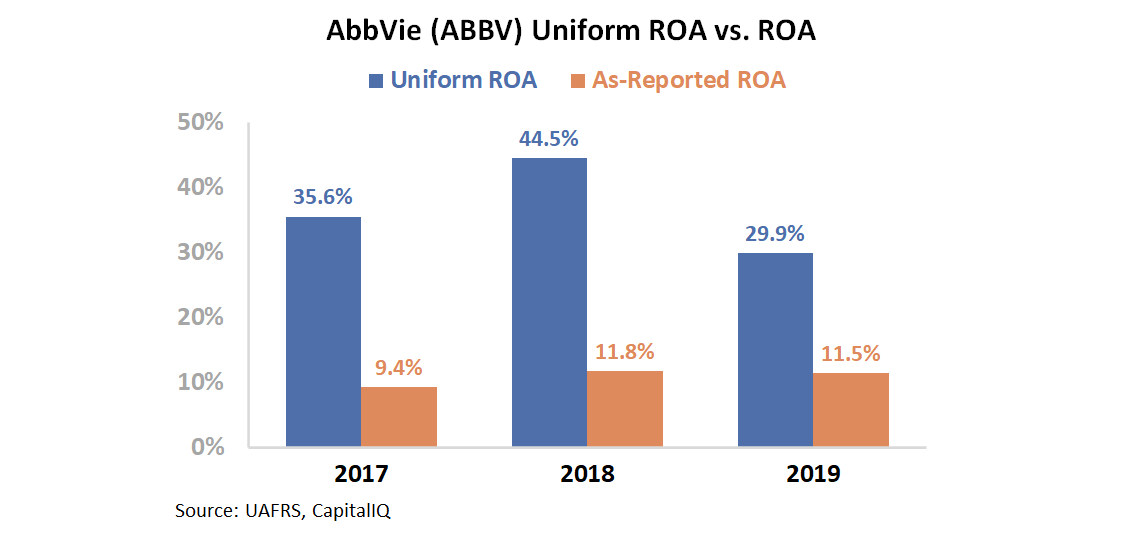

However, as-reported metrics are not showing the full extent of AbbVie’s profitability and efficiency. GAAP’s treatment of special items and goodwill, among other distortions, is suppressing the firm’s profitability.

In reality, AbbVie has been able to sustain a high ROA. The firm’s multiple successful drugs, including HUMIRA (adalimumab) and MAVYRET (glecaprevir/pibrentasvir), have been able to sustain robust returns.

Uniform ROA has ranged between 30% and 45% over the past 3 years.

The final piece of information we need to evaluate are the expectations. To understand what the market is pricing in, we can use our Embedded Expectations Analysis Framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model. A DCF model uses investors’ assumptions about the future, which then produces the “intrinsic value” of the stock.

However, this method requires perfect forecasting of the future, which is unreasonable. Therefore, we turn the DCF model on its head in the below chart. Here, we use the current stock price to solve for what returns the market expects the firm to make.

The dark blue bars represent the historical corporate performance levels in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how ROA will shift in the next five years.

Wall Street analysts expect AbbVie to sustain Uniform ROA levels in 2020 and even improve ROA to 33% in 2021. However, the market is pricing in Uniform ROA to collapse to 12% by 2024.

It’s clear the market is looking at the wrong metrics to evaluate the firm. In reality, AbbVie’s products are in demand whether there is a pandemic or not. With the firm’s most profitable drug still on the market (HUMIRA) and multiple exciting drugs in the pipeline, expectations for Uniform ROA to more than halve appear too pessimistic.

Uniform Accounting is able to show how successful AbbVie truly is. Although the pandemic has adversely affected parts of the Healthcare industry, AbbVie’s products have remained in demand.

With expectations for Uniform ROA to deteriorate exceedingly bearish, it may be a company investors want to keep an eye on.

SUMMARY and AbbVie Inc. Tearsheet

As the Uniform Accounting tearsheet for AbbVie Inc. (ABBV:USA) highlights, the Uniform P/E trades at 10.9x, which is below the global corporate average valuation levels, but around its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of AbbVie, the company has recently shown a 12% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AbbVie’s Wall Street analyst-driven forecast is a 4% EPS decline in 2020 and 32% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AbbVie’s $105 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 6% per year over the next three years and still justify current stock prices. What Wall Street analysts expect for AbbVie’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 5x the corporate average. Also, cash flows and cash on hand are around 2x its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals a low credit and dividend risk.

To conclude, AbbVie’s Uniform earnings growth is in line with peer averages, while their valuations are traded in line with its average peers.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research