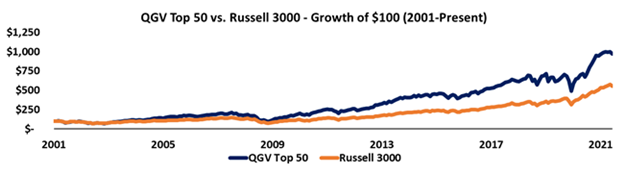

This list of 50 stocks consistently beat the market for the past 20 years

History has shown that the world’s greatest investors, past and present, understand the simple fact that as-reported financial metrics are unreliable

To be successful, they account for arbitrary accounting rules by adjusting the financials, providing a true picture of economic reality and allowing them to find companies that exhibit three characteristics: high quality, strong growth potential, and low valuations.

Today, we highlight our QGV 50, which emulates this investment strategy to produce outsized returns in excess of the market over long periods of time.

We’ll take a look at one company in particular on this month’s QGV 50, describing how as-reported metrics distort economic reality and can lead investors to miss significant opportunities.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Investors who get caught up only investing in the latest fad, be it cryptocurrency, clean energy, cybersecurity, or any number of other popular themes, often do so at their own expense.

While there are always hidden gems in the midst of the hype, most investors find themselves staring down overvalued companies that have made some big promises. Without being able to separate the wheat from the chaff, investors often end up overpaying for name recognition.

The world’s best investors don’t often spend their time picking out the most popular companies, but rather look for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

That’s exactly what we’ve set out to do with the QGV 50, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300bps per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

To be clear, you can only see how powerful Uniform Accounting truly is by looking at the data, and one of this month’s top companies on the QGV 50, AmerisourceBergen (ABC), is a perfect example.

AmerisourceBergen is a pharmaceutical distribution business, sourcing brand-name and generic drugs, over-the-counter healthcare products, and home healthcare supplies from manufacturers and sending them to hospitals, retail pharmacy chains, and many other customers.

On top of the pharmaceutical distribution business, AmerisourceBergen also operates a small veterinarian distribution segment, making the combined enterprise a rather standard, easy-to-understand, and frankly boring business that is unlikely to excite investors.

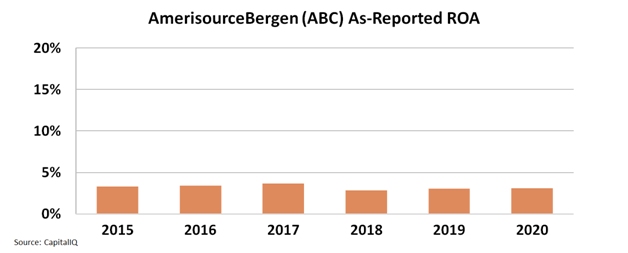

Looking at as-reported financial metrics, which suggest AmerisourceBergen generated a return on assets (“ROA”) of only 3% in 2020, well below average cost of capital levels in the U.S. at around 4.8%, investors would probably assume this pharmaceutical distributor isn’t just a boring company, it’s actually a bad business.

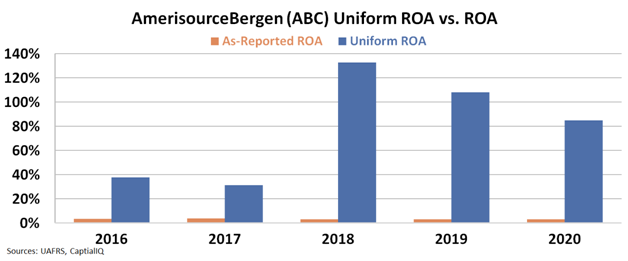

In reality, Uniform Accounting metrics show that being a dominant distributor of vital healthcare products, along with churning through inventory that is bought and then sold immediately, actually makes for a fantastic business.

This is especially true if you have the right scale, which AmerisourceBergen does by being one of the three biggest players in the space, along with McKesson (MCK) and Cardinal Health (CAH).

Thanks to its strong operations, AmerisourceBergen actually generated a Uniform ROA of 85% in 2020, not the below cost of capital levels suggested by as-reported metrics. Moreover, the company has recently been re-investing in itself, growing its asset base almost 10% in 2019 and over 35% in 2020.

With a Uniform price-to-earnings ratio (“P/E”) of just 16.5x, AmerisourceBergen trades well below market averages as well, making it a compelling name checking off all the boxes of quality, growth, and value.

Finding great companies with growth potential trading at favorable prices shouldn’t be this easy, especially in the current market environment. Yet, with Uniform Accounting it is, and that’s why the QGV 50 has had such tremendous success beating the market over the years.

To learn more about the QGV 50 and see the other 49 companies on the list, click here to get full access today.

SUMMARY and AmerisourceBergen Corporation Tearsheet

As the Uniform Accounting tearsheet for AmerisourceBergen Corporation (ABC:USA) highlights, the Uniform P/E trades at 16.5x, which is below the global corporate average of 24.3x, but above its historical P/E of 13.8x.

Low P/Es require low EPS growth to sustain them. In the case of AmerisourceBergen, the company has recently shown a 49% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AmerisourceBergen’s Wall Street analyst-driven forecast is a 29% EPS shrinkage in 2021 and a 24% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AmerisourceBergen’s $120 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 2% annually over the next three years. What Wall Street analysts expect for AmerisourceBergen’s earnings growth is below what the current stock market valuation requires in 2021, but is above that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 14x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

Lastly, AmerisourceBergen’s Uniform earnings growth is below peer averages and the company is also trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research