ACM Research doesn’t need to make semiconductors itself to see a huge windfall

As the semiconductor sector sees an uptick in demand, so do companies that act as suppliers to the sector.

One of those companies is ACM Research (ACMR), which sells cleaning supplies to semiconductor manufacturers.

However, as-reported metrics seem to miss the tailwinds ACM Research is seeing, and make it appear the company has low profitability.

That’s why this company showed up on our FA Alpha Screen. Its strong profitability, high growth, and attractive valuations make it a compelling company.

Investor Essentials Daily:

Tuesday FA Alpha 50

Powered by Valens Research

Most of the time, when analysts dig into an industry with massive multi-year tailwinds, it’s impossible to find a compelling stock in the universe, since everything is already priced for perfection.

Right now, the semiconductor sector is seeing massive tailwinds from record demand and limited supply. Semiconductors are omnipresent in many of today’s electronics, including computers, smartphones, cars, and appliances.

The need for supply expansion has never been higher, especially with US companies talking about nearshoring production. This all means the industry is struggling to ramp up quickly enough.

This higher demand means firms like ACM Research (ACM) are more compelling than ever, which is an essential part of the supply chain for semiconductors.

ACM Research sells wet processing technology along with products that streamline the manufacturing process for the companies that produce semiconductors.

Yet, as-reported metrics seem to be missing the role ACM Research plays in supporting the increased production of semiconductors.

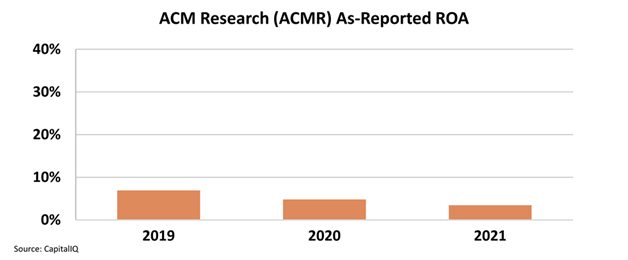

As-reported metrics make it appear that return on assets (“ROA”) has been generally declining over the past three years and is stuck near cost-of-capital levels. In 2021, it looks as though ROA has dropped to historical lows of just 5%.

For a company so crucial to improving the pipeline of semiconductors, this low profitability would come as a surprise. However, Uniform Accounting, which gets rid of the accounting distortions of GAAP metrics, shows us a different picture.

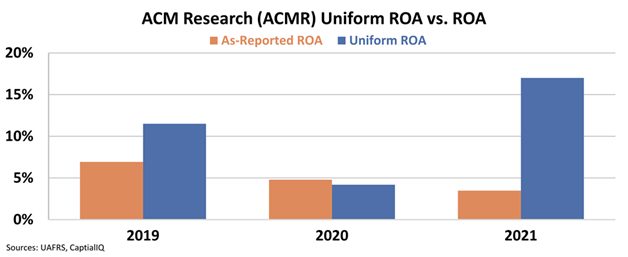

We can see that ACM Research actually saw a massive surge in profitability as demand skyrocketed. Uniform ROA jumped from 4% in 2020 to 17% in 2021, clearing both cost-of-capital levels and corporate averages.

As the semiconductor sector saw the need to expand, it’s clear companies turned to ACM Research to make that happen.

However, the market seems to be missing these tailwinds, with ACM Research being priced with a Uniform P/E of 10.1x, telling us it’s actually fairly cheap. And it doesn’t seem the demand for semiconductors will be going down any time soon, so we can expect strong profitability and performance to continue in the near future.

But you can only see this impressive performance if you look at the right Uniform Accounting data.

As-reported metrics hide ACM Research’s strong ROA, which combined with its comfortable growth and low valuations, makes it a compelling company and an interesting FA Alpha 50 name.

Throughout financial market history, many of the world’s most successful investors have been candid in their belief that Generally Accepted Accounting Principles (“GAAP”) distort economic reality.

Warren Buffett, for example, once said investors should “concentrate on the world of companies, not arcane accounting mathematics.”

Investors who neglect the very real issues with as-reported accounting can find themselves caught up investing with the crowd, blindly following hot “themes” without a thorough grasp of how to understand the businesses in question.

The only true way to focus on the “world of companies,” as Buffett suggests investors do, is to present a clear picture of how a business operates, something that can only be done by adjusting financial statements to reflect the arbitrary nature of certain accounting rules that leave much to discretion.

The world’s best investors understand the need to make these adjustments, which allows them to focus not on picking out the most popular companies, but rather on looking for great names in sleepy areas that the market isn’t paying much attention to. From there, the goal is to then identify quality companies with significant growth potential at reasonable prices.

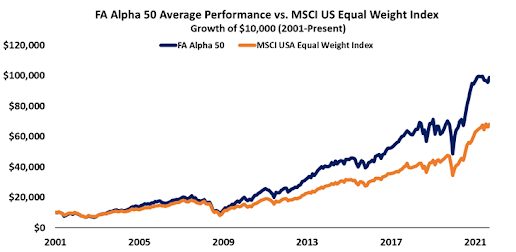

That’s exactly what we’ve set out to do with the FA Alpha, our monthly list of 50 companies that rank at the top for quality, high growth, and low valuations.

This list has outperformed the market by 300 basis points per year for over 20 years now, effectively doubling the performance of the market by focusing on the real fundamentals and valuations of companies with our proprietary Uniform Accounting framework.

See for yourself below.

If you’re interested in seeing the other 49 names on this month’s FA Alpha, click here to learn more.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research