This trading firm appears to be trading at a discount, but the market may already be clued in

The commodity trading industry is a specialized part of the economy. The grain trading industry is an even more specialized niche. Today’s firm is one of the major players in this space.

Looking at as-reported numbers, investors might think this company is trading at an attractive valuation. However, looking through the accounting noise shows this may not be the case.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

The world of grain trading is controlled by only four companies. Unlike equity, bond, or even other popular commodity trading, the market is small and cannot sustain more than a handful of players.

The four companies which dominate the industry are known as the ABCD quartet. They are Archer-Daniels-Midland (ADM), Bunge (BG), Cargill, and Dreyfus.

Each company is deeply entrenched in the grain trading industry. All four are over 100 years old. Bunge was founded in 1818, and Cargill is now the second largest private firm by revenue in the United States.

The quartet also has the infrastructure necessary to succeed. They each have offices around the world and tens of thousands of employees.

Even with their impressive relationships and infrastructure, the firms generate below average returns. This is because at the end of the day, these are still literal commodity businesses.

On the positive side, returns are fairly consistent, as there is always demand for commodities like grain.

With such a predictable, albeit low-return business, this is not your typical earnings growth-style investment. Rather, investors would need either a deep discount or a significant dividend yield to invest in this type of name.

Currently, Archer-Daniels-Midland is trading at a 14.1x P/E, which seems like a steal in the current market for such a stable business.

However, this depiction of the firm’s valuation is not accurate. GAAP is distorting the firm’s earnings through line items like interest income and maintenance capital expenditures, among others items.

This is causing the firm to look cheaper than as-reported metrics suggest.

Uniform P/E for the firm is 23.0x, right near market averages. This is also at a level which is similar to where it has traded in the past.

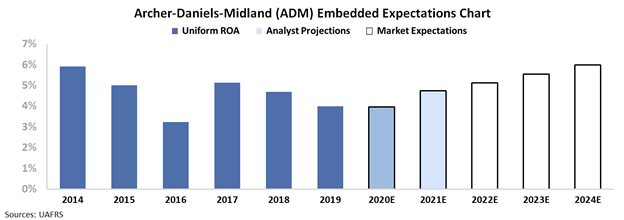

To understand how these valuations translate to market expectations, we can use our Embedded Expectations Framework.

Most investors determine stock valuations using a discounted cash flow (DCF) model. Investors build a DCF model using assumptions about the future, which then produces the “intrinsic value” of the stock.

However, here at Valens, we know models with garbage-in assumptions only come out as garbage. This is why we turn the DCF model on its head in the below chart. Here, we use the current stock price to solve for what returns the market expects the firm to make.

The dark blue bars represent the historical corporate performance levels, in terms of ROA. The light blue bars are Wall Street analysts’ expectations for the next two years. Finally, the white bars are the market’s expectations for how ROA will shift in the next five years.

The Embedded Expectations confirm the firm looks to be fairly valued, or even slightly overvalued. Wall Street analysts expect Uniform ROA to stay near current levels. Then, the market is pricing in marginal improvement in Uniform ROA to 6% by 2024, in line with peak profitability.

Uniform Accounting is able to sniff out this value trap. Investors may see Archer-Daniels-Midland as trading at a discount. However, the market has already priced in the firm as a stable business, a nuance lost on most investors.

SUMMARY and Archer-Daniels-Midland Company Tearsheet

As the Uniform Accounting tearsheet for Archer-Daniels-Midland Company (ADM:USA) highlights, the Uniform P/E trades at 23.0x, which is around the global corporate average valuation levels and its historical average valuations.

Average P/Es require average EPS growth to sustain them. In the case of Archer-Daniels-Midland, the company has recently shown a 17% decline in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Archer-Daniels-Midland’s Wall Street analyst-driven forecast is a 2% EPS shrinkage in 2020 and a 30% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Archer-Daniels-Midland’s $50 stock price. These are often referred to as market embedded expectations.

In order to justify current stock prices, the company needs Uniform earnings to grow 5% each year over the next three years. What Wall Street analysts expect for Archer-Daniels-Midland’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

Furthermore, the company’s earning power is below the long-run corporate averages. However, cash flows and cash on hand are above its total obligations—including debt maturities, capex maintenance, and dividends. Altogether, these signal low credit and dividend risk.

To conclude, Archer-Daniels-Midland’s Uniform earnings growth is in line with its peer averages, and the company is also trading in line with its peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research