The liquidity surge in March and April has saved today’s company, Uniform Accounting shows the bond market still hasn’t caught on

In the beginning of the pandemic, many credit investors feared firms would be unable to pay their bills and be forced into bankruptcy.

However, due to the aggressive liquidity provided by the Fed and other central banks, many firms were able to build a safe runway of capital through the crisis. Today’s firm has raised debt to cover its operating obligations, but its bonds still are priced as though it didn’t.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

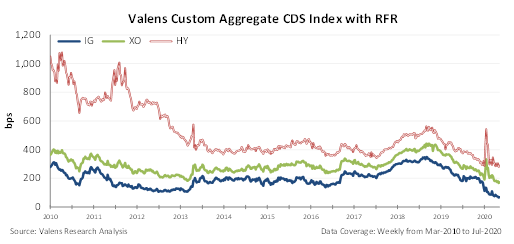

Back in March, in the midst of the pandemic, panic ruled the markets. Even as we highlighted limited debt maturity headwalls for companies that could have created a liquidity crisis, investors sold off securities. Yields in both investment-grade and high-yield stocks shot higher.

Debt investors’ concerns were not based around the timing of upcoming debt maturity headwalls. Rather, the pandemic could have been a rare situation where companies could default because they would not be able to pay any of their bills. Investors feared the lockdown would cause corporate revenue to dry up completely.

Then, this was averted as central banks globally opened the liquidity spigot to help bridge the short-term “demand strike” that occurred. Over $1.25 trillion of investment-grade and $250 billion of high-yield corporate bonds have been issued in the US in the past few months.

As corporate and bank debt was drawn down, the short-term liquidity risk was removed, and spreads came down.

As we’ve highlighted previously when analyzing macroeconomic indicators, the cost to borrow for corporates, which we look at by looking at aggregate credit default swaps (“CDS”) plus the risk-free rate (“RFR”), the treasury yield, rose from sub 4% for high yield companies to almost 6% in March. It subsequently came down massively.

The market understood that these initiatives had de-risked corporations.

One of the many companies that benefited from this liquidity was Adient plc (ADNT).

An auto parts producer, Adient was initially at risk of revenue shock. Adient might not have seen any revenue for the foreseeable future, as auto production froze. Without much needed liquidity, it might not have been able to keep the lights on.

Any and all potential concerns of bankruptcy were abated as the company raised capital once the floodgates of liquidity opened.

Adient raised $800 million in extra cash moving into the end of March, boosting its cash balance up to $1.6 billion. This much needed infusion has given Adient the ability to survive this period of revenue pressure.

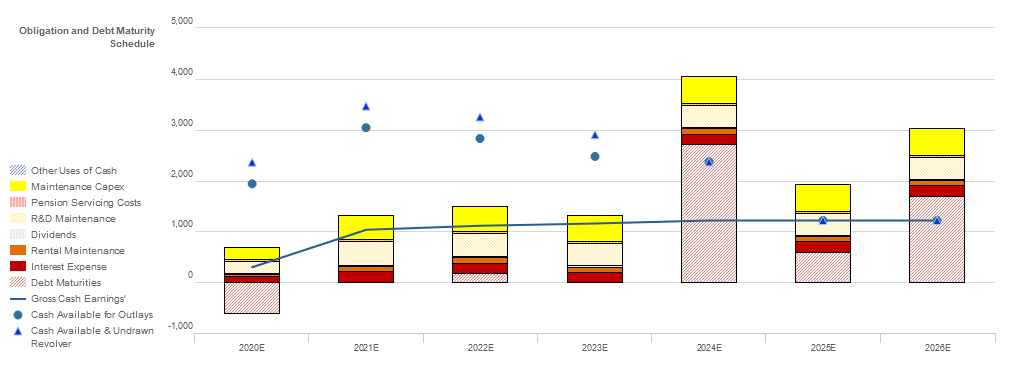

As you can see from the Credit Cash Flow Prime, Adient does not have cash flow to cover their obligations in the current environment. The blue line, cash flow each year, is below the total stacked obligations because of the challenging environment.

However, its cash on hand thanks to the loans it raised is more than enough to cover all obligations through the next three years.

While Adient’s position has improved dramatically, the markets haven’t priced Adient like everything is ok. The bond markets appear to still be focused on how the pandemic is impacting things in the short-term and have not fully grasped how much Adient’s position has improved.

Bond yields for Adient are currently at 6.5%, well into the high yield space. For a company that doesn’t have any liquidity issues, even if their markets remain closed, for some time, that just doesn’t make sense.

The market is looking at Adient as a firm in danger of being unable to pay its bills, and it is priced accordingly. Due to this, the credit yield may be overstating the company’s true fundamental credit risk.

Tightening of Credit Market Spreads Likely as ADNT’s Multi-Year Debt Runway Continues to be Overlooked

Credit markets are grossly overstating ADNT’s credit risk with a YTW of 6.528%, relative to an Intrinsic YTW of 3.068% and an Intrinsic CDS of 280bps. Additionally, Moody’s is overstating ADNT’s fundamental credit risk, with its Ba3 credit rating three notches lower than Valens’ XO (Baa3) rating.

Fundamental analysis highlights that ADNT’s cash flows would fall short of meeting operating obligations in each year going forward. That said, following its recent debt issuance, ADNT’s cash flows plus its substantial cash buffer would be sufficient to cover all obligations including debt maturities until 2024, when the firm faces a material $2.7bn debt headwall.

In addition to this multi-year debt runway to improve operations, the firm has some capex flexibility to free up liquidity in the near-term which should allow it to service operating obligations as necessary. Moreover, the firm boasts a robust 149% recovery rate on unsecured debt, indicating that it should be able to access credit markets to refinance, if necessary.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for creditors. ADNT’s compensation framework should drive management to focus on all three value drivers: asset utilization, margin expansion, and top-line growth, which should lead to Uniform ROA improvement and increased cash flow available for servicing obligations going forward.

In addition, management has low change-in-control compensation relative to their average annual compensation, indicating that they are unlikely to pursue a sale or buyout of the firm, reducing event risk.

However, management members are not material holders of ADNT equity relative to their annual compensation, indicating that they may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (5/5) highlights that management generated an excitement marker when saying the coordination of state governments provided OEMs the opportunity to return to work, and they are confident they were able to maintain EBITDA at historical levels and that production stability will have a dramatic impact on fixed and variable cost reduction efforts.

Earnings Call Forensics™ of the firm’s Q2 2020 earnings call (5/5) highlights that management generated an excitement marker when saying the coordination of state governments provided OEMs the opportunity to return to work, and they are confident they were able to maintain EBITDA at historical levels and that production stability will have a dramatic impact on fixed and variable cost reduction efforts.

Moreover, they may lack confidence in their ability to emerge from the coronavirus crisis as a stronger company, drive improvements in their SG&A spend and EBITDA, and execute new product launches.

Furthermore, they may be concerned about their production restart, metals and mechanisms business safety procedures, and their burn rate in an uncertain production environment.

ADNT’s substantial cash buffer, multi-year debt runway, and robust recovery rate indicate that credit markets and Moody’s are overstating credit risk. As such, both a ratings improvement and tightening of credit market spreads are likely going forward.

SUMMARY and Adient plc Tearsheet

As the Uniform Accounting tearsheet for Adient plc (ADNT:USA) highlights, the company trades at a -19.1x Uniform P/E, which is way below global corporate average valuation levels and its historical average valuations.

Negative P/Es only require low EPS growth to sustain them. That said, in the case of Adient, the company has recently shown a 41% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Adient’s Wall Street analyst-driven forecast projects 120% earnings growth in 2020, followed by a 67% shrinkage in 2021.

Furthermore, the company’s earning power is below corporate average levels. Also, cash flows and cash reserves will be sufficient to cover the company’s debt maturities only up until the fifth year, when the firm faces consistent material debt headwalls.

Its earning power and debt maturities, together with the company’s intrinsic credit risk being 280bps above the risk-free rate, signal an average risk to its credit.

To summarize, Adient is currently seeing above average peer Uniform earnings growth. However, the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research