Ratings agencies don’t seem to have learned their lesson from the Great Recession, that a strong asset backing alone can’t guarantee refinancing

The Great Recession and the recent struggles of MLPs have demonstrated that even asset-backed credit markets can dry up, restricting debt-laden firms from refinancing.

Moody’s may still be under the impression that this firm’s strong asset backing will always allow it to refinance. However, Uniform Accounting demonstrates that the firm has material debt headwalls in each year going forward, suggesting that credit holders are undercompensated.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Back in the summer of 2016, we published an article on Seeking Alpha, focusing on the credit risks for AerCap Holdings (AER).

For those who don’t know, AerCap leases aircraft to airlines for them to use in their operations.

We highlighted how the company’s credit risk was being materially understated at the time, because the market was failing to fully capture refinancing risk.

Our concern wasn’t that AerCap was an imminent bankruptcy risk that investors needed to steer clear of. Instead, we simply suggested that investors were being undercompensated for the risk they were taking on related to its consistent debt maturities.

The article launched a healthy discord with a reader in the message board section. We refuted his claim that the firm’s strong asset backing from airplanes suggested that they could always refinance.

Our concern was, if the market was ever frozen for refinancing, they could be in trouble. A risk we didn’t highlight…if AerCap’s customers lost all their revenue, even with AerCap’s asset backing, the company could see cash flow disruptions that could spook credit markets.

In fact, similar to our conversation about Avis a couple months ago, there is historical evidence that sometimes a strong asset base is insufficient to access credit markets to refinance, especially when a firm may need it most.

In particular, MLPs, generally oil & gas transportation and storage companies who get a tax advantaged status thanks to their asset-based income strategy, offered a great warning signal to investors who wanted to depend on asset-backed lending to help avoid a short-term cash crunch.

In 2015-2016, during the oil price glut, more than 100 asset-intensive oil-related companies filed for bankruptcy; 2008 was a similar mess. And MLPs were certainly not spared either. It seemed that, when the firms needed refinancing the most, credit markets dried up.

More recently, as COVID-19 has ravaged the demand for oil, and oil prices have collapsed, many MLPs find themselves in the same position, desperately searching for cash, while sitting on assets that have lost much of their appeal.

AerCap now faces the same potential risks, if demand for airlines is reduced for a period of time.

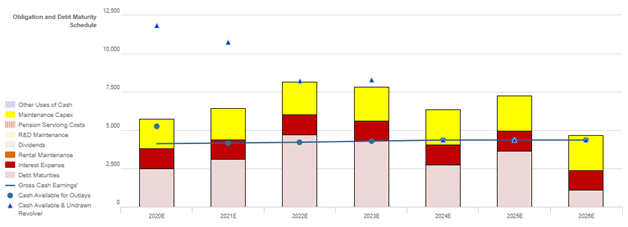

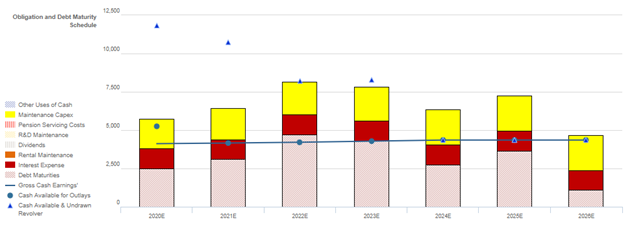

When looking at the firm through a Uniform Accounting lens, as demonstrated in the chart below, it becomes evident that AerCap is reliant on refinancing to sustain its operations.

Aercap has material debt maturities in each year going forward, which its combined cash flows and cash on hand will fall short of covering starting this year.

Although the firm has had success in the past refinancing its debt, should creditors sour on the value of its assets considering recent disruptions, the firm could face an imminent liquidity crunch.

It is clear that the firm should be viewed as a higher credit risk, but it seems that ratings agencies, such as Moody’s, may have bought into the same idea as our reader, that AerCap “will always be able to refinance.”

Just like Moody’s looked the other way for the last asset-based lending bubble, the mortgage crisis of the Great Recession, it looks like it is looking away now, giving AerCap a fairly favorable Baa3, or crossover rating, based on the asset backing.

But in reality, if the credit market ever froze, as it did during the Great Recession, and as it did for MLPs more recently, this company and its peers would be left in dire situations. Hence, this firm should be looked at as a high-yield name, which is why we give it a HY1 (equivalent of a Ba2 rating).

Once again, instead of looking at the fundamentals of a company, Moody’s is making the same mistake that cost investors greatly in the past. Only using Uniform Accounting can the extent of this error be identified.

AER’s Consistent Debt Maturities and Operational Sustainability Indicate Both a Ratings Downgrade and a Tightening of Bonds Spreads Are Likely Going Forward

Credit markets are grossly overstating AER’s credit risk with a YTW of 8.227%, relative to an Intrinsic YTW of 4.237% and Intrinsic CDS of 450bps.

However, Moody’s is materially understating AER’s fundamental credit risk, with their Baa3 credit rating five notches higher than Valens’ HY2 (B2) rating.

Fundamental analysis highlights that AER’s cash flows should service operating obligations in each year going forward. However, AER faces consistent material debt maturities that will cause cash flows and cash on hand to fall short of servicing all obligations including debt maturities starting in 2020, when the firm faces a material $2.5bn debt headwall.

Although the firm has some capex flexibility to free up liquidity in the near-term, it will have to refinance in order to avoid a liquidity crunch.

In addition, despite the firm’s sizeable market cap and history of successful refinancing, AER only has a neutral 40% recovery rate on unsecured debt, indicating that it may struggle to refinance at favorable rates.

Incentives Dictate Behavior™ analysis highlights that most management members, aside from CEO Kelly, are not material holders of the firm’s equity, implying that they may not be well aligned with shareholders for long-term value creation.

In addition, there is no publicly disclosed information on AER’s compensation framework, making it difficult to understand how well management is aligned in terms of overall value creation for the business.

Earnings Call Forensics™ of the firm’s Q4 2019 (2/13) earnings call highlights that management is confident that their consistent earnings growth is a result of their platform and processes.

However, they may be exaggerating their expectations for a ratings upgrade, the strength of their credit profile, and their ability to deal with airline defaults.

Moreover, they may lack confidence in their ability to sustain mid-life and older aircraft sales, continue their share repurchase program, and improve their book value per share.

Finally, they may be concerned about their recent aircraft purchases, the sustainability of a stock valuation arbitrage, and gradual declines in demand for current aircraft technology.

AER’s operational sustainability and a history of successful refinancing indicate credit markets are overstating the firm’s credit risk, while consistent debt maturities and a neutral recovery rate indicate that Moody’s is understating risk.

Therefore, a ratings downgrade and a tightening of credit spreads are both likely going forward.

SUMMARY and AerCap Holdings N.V. Tearsheet

As the Uniform Accounting tearsheet for AerCap Holdings N.V. (AER) highlights, the company trades at a 16.1x Uniform P/E, which is below global corporate average valuation levels, but around its historical average valuations.

Low P/E’s only require low EPS growth to sustain them. That said, in the case of AER, the company has recently shown a 27% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AER’s Wall Street analyst-driven forecast projects a 34% shrinkage in earnings in 2020 followed by 6% growth in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $24 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for AER, the company would just have to have Uniform earnings shrink by less than 9% each year over the next three years.

Wall Street analysts’ expectations for AER’s earnings growth are above what the current stock market valuation requires in 2021.

Meanwhile, the company’s earnings power is 1x corporate averages. Despite this, total obligations—debt maturities, maintenance capex, and dividends—are above total cash flows, signaling an average risk to its dividend or operations.

To summarize, AER is expected to see below average Uniform earnings growth in 2020, which is expected to rebound in 2021. However, as is warranted, the company is trading below peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research