Rating agencies may have been too quick to upgrade this power company

Up until last year, there were no investment grade companies in the independent power industry. Just recently, one company in this industry saw its credit rating upgraded into the investment grade world.

But were rating agencies too early to judge?

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

The three main rating agencies, Moody’s, Fitch, and S&P, play particularly important roles when analyzing companies and issuing credit ratings.

Many equity and credit investors often revert to credit ratings when doing due diligence on a specific credit name.

They often also keep an eye out for upgrades or downgrades issued for a particular name based on some news or events that occurred.

However, these ratings are often dogmatically applied. The three rating agencies have long-standing memories for tumultuous industries, holding back on changing ratings even when conditions change. Additionally, they can often refuse to change certain company ratings.

For example, throughout the later decades in the 20th century, independent power production companies saw many booms and busts, with surging demand, and plant developments, followed by bankruptcies.

The industry was going through such a quick cycle the rating agencies essentially forbade any company within the industry from receiving an investment grade rating.

Any nuanced analysis was taken out of the process for this industry. It no longer mattered how great a company’s cash flows were or how strong their credit risk picture was.

Companies operating in the independent power production industry could not earn a rating that entered the BB/BBB or Ba/Baa threshold for the S&P and Moody’s.

That was only the case up until last year.

One of the biggest independent power production companies received stellar news.

The AES Corporation (AES) debt was upgraded to a BBB- by the S&P. It appears the major rating agencies are easing restrictions on this troubled industry.

While this achievement is noteworthy for AES and the industry as a whole, it may seem S&P was too early to give this investment grade rating.

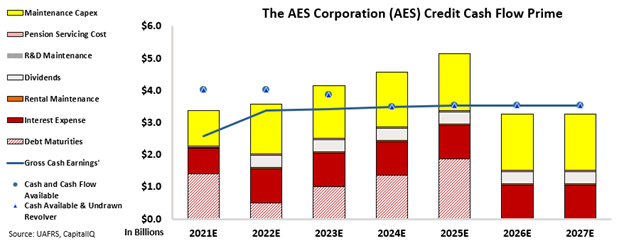

Our Credit Cash Flow Prime (CCFP) analysis is able to get to the heart of the firm’s true credit risk.

When taking a look at this picture, it appears S&P did jump in on AES letting it be the one to get upgraded to soon.

In the below chart, the stacked bars represent the firm’s obligations each year for the next five years. These obligations are then compared to the firm’s cash flow (blue line) as well as the cash on hand at the beginning of each period (blue dots) and available cash and undrawn revolver (blue triangles).

As depicted, the company’s massive investment in moving towards green operations and away from coal means it has a lot of debt coming due that it will need to refinance.

AES’ cash flows also do not exceed all of the company’s non-debt operating obligations, particularly its capital expenditures over the next 5-7 years.

Additionally, the company’s cash on hand, coupled with available cash to draw down from its revolver, only exceeds all obligations through 2022, not giving the company much time to refinance its upcoming debt.

Rather than the first investment grade rating in quite some time for this industry, AES is actually a name with great pressure on cash flows. This is why S&P’s BBB- investment grade rating, with a 2%+ risk of default expectation does not make sense.

Using the CCFP analysis, Valens rates AES as a high yield HY2 rating. This rating corresponds with a default rate near 25% within the next five years, a more realistic projection once a holistic understanding of the company’s risk is taken into account.

SUMMARY and The AES Corporation Tearsheet

As the Uniform Accounting tearsheet for The AES Corporation (AES:USA) highlights, the Uniform P/E trades at 65.0x, which is above the global corporate average of 23.7x and its own historical average of 55.4x.

High P/Es require high EPS growth to sustain them. In the case of AES, the company has recently shown a 15% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AES’ Wall Street analyst-driven forecast is a 5% EPS growth in 2021 and 1% EPS decline in 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AES’ $25 stock price. These are often referred to as market embedded expectations.

AES is currently being valued as if Uniform earnings were to grow by 21% per year over the next three years. What Wall Street analysts expect for AES’ earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is below the long-run corporate average. Also, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high credit and dividend risk.

To conclude, AES’ Uniform earnings growth is below with its peer averages but the company is trading well above average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research