AI is making this retail giant’s best business even better

Amazon (AMZN) is shifting from hiring to automating. AI is taking over coding, inventory planning, and customer support, and CEO Andy Jassy plans corporate staff cuts as these tools scale.

The change matters most in AWS, which sells cloud and AI services and already drives the lion’s share of profit, about 17% of sales but more than 58% of profits last year.

AI use should both cut AWS costs and spur more customer demand for its capacity and tools.

Yet the market is only pricing in a marginal profitability improvement, leaving upside if AWS leverage pushes returns higher. Investors who see this gap may be rewarded.

Investor Essentials Daily:

Thursday News-based update

Powered by Valens Research

Amazon’s (AMZN) days of expansion are over, but not in the way you might think…

For decades, the e-commerce giant has expanded and hired thousands of employees to support its retail and cloud businesses. It employs more than 1.5 million people around the world.

Now, AI is taking over much of that work. Tasks that once required whole teams—like writing internal software, predicting inventory needs, and answering customer questions—are handled by software instead.

And this is only the start. CEO Andy Jassy announced last month that the company will cut corporate staff over the next few years as it rolls out more AI tools.

This move is certainly a way to save money. But it’s more than that. Amazon’s future layoffs reflect a bigger change in how the company operates, especially in its most profitable business, Amazon Web Services (“AWS”).

The segment makes money by renting out server space and more importantly, by selling software, cloud services, and support on top of that.

This combination earns far more than Amazon’s retail side. AWS has been the company’s main source of profit for years. In 2018, it made up roughly 13% of sales and around 52% of profits.

And those numbers are rising as the AI revolution takes hold.

Every time a customer uses AWS storage, computing power, or advanced tools, Amazon earns revenue.

As businesses adopt AI, they need even more cloud capacity. Amazon already sells AI tools that help customers build and run their own models which drives even more demand for AWS.

Meanwhile, the company is cutting costs inside AWS. It’s using AI to handle everything from coding to customer service and saving money in the process.

AWS brought in 17% of total sales last year and more than 58% of profits. In other words, as AWS uses AI more, it’s getting even more profitable for Amazon.

But while Amazon embraces AI, investors aren’t all that excited. They don’t seem to understand this Big Tech mainstay’s transformation.

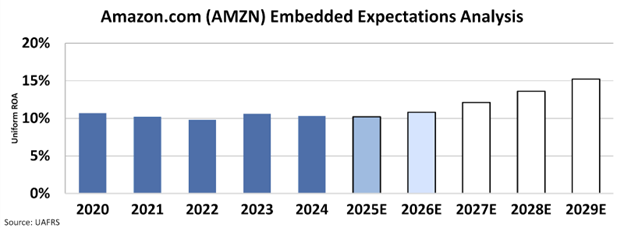

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Amazon’s Uniform return on assets (“ROA”) has held steady around 11% for the past five years, and now the market only expects a marginal improvement towards 15%.

We’ve already seen how much more profitable AWS can be in a few years. As Amazon rolls out more AI within the business, it should blow these expectations out of the water.

It’s rare for such an obvious AI winner to have such low expectations. It may not have the flashiest models or the most prominent AI hardware like some of its biggest peers, but Amazon is a clear winner in the AI race.

As AWS grows and earns more of Amazon’s profit, investors who understand what’s happening today could see solid gains in the years ahead.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research