Ratings agencies are missing the risk inherent in today’s company that Uniform Accounting makes apparent

It is important to look at a company’s debt obligations in addition to the macroeconomic environment, as external factors can affect a firm’s cash flows immensely.

Today’s firm faces pressures from both the coronavirus and its customer base. However, with all the headwinds the company faces, S&P continues to believe the firm is at very little risk of default.

Below, we show how Uniform Accounting restates financials for a clear credit profile. We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Since 1980, 205 airline companies have declared bankruptcy in the United States alone. The reason for their bankruptcies have varied; some issues have come from their debt, pension funding, or elevated costs from gate contracts.

With their experience of bankruptcies, the existing airlines have understood how to use bankruptcy to their advantage. They have accumulated a deep knowledge of the workings of bankruptcy courts and have used it to get out of obligations when they can’t support paying anymore.

For example, Delta declared bankruptcy in September of 2005, citing rising fueling costs. The firm emerged 19 months later as a vastly more improved company. The firm was able to reduce net debt by roughly half and grow its Uniform ROA to above cost-of-capital levels.

The airline industry’s intimate knowledge of bankruptcy puts Air Lease Corporation (AL) in a precarious scenario. Air Lease does not fly any planes itself. Instead, it leases out its fleet of nearly 250 planes to airline companies around the world.

All of the firm’s airline customers are running severely reduced schedules, and are muddling through a prolonged recovery process. One way airlines might try to reduce capacity is to do everything in their power to get out of Air Lease’s leasing contracts. And yet, Air Lease still trades at a roughly 3% yield and has a BBB rating from S&P.

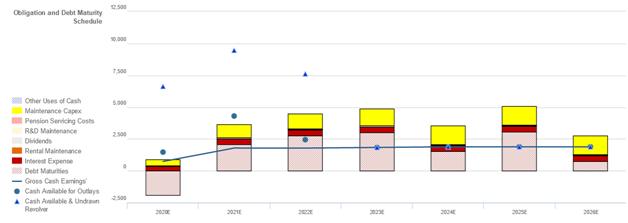

Air Lease’s Credit Cash Flow Prime (CCFP) shows that the firm cannot allow airlines to question the value of its planes by shirking contracts. In the past, Air Lease has avoided liquidity issues due to its strong asset backing. However, given the changing market driven by the coronavirus, this might not be enough.

The firm has the cash on hand to pay off next year’s obligations thanks to its debt issuances this year. Furthermore, the firm should be able to use its revolver to pay off 2022 obligations.

However, 2023 and beyond all bring challenges. It will be essential for Air Lease to be able to refinance its debt maturities, thanks to its plane inventory, to be able to survive.

Even with all of these troubles looming, S&P still rates Air Lease as an investment grade security, implying under a 2% chance of default over the next five years.

Rating agencies are completely missing the mark and are not taking into account consistent debt maturities and macroeconomic headwinds for the company. Comparatively, we give the firm a HY1 (equivalent to BB) rating, 3 notches lower than S&P’s rating.

Understanding a firm’s upcoming obligations and how the larger economy can affect the firm are vital to gauge bond risk. When analyzing Air Lease through that lens, it is clear that credit rating agencies are undervaluing the firm’s current fundamental credit risk.

AL’s Consistent Debt Headwalls Will Likely Lead to a Ratings Downgrade

Credit markets are accurately stating credit risk with a cash bond YTW of 2.985% relative to an Intrinsic YTW of 2.765% and an Intrinsic CDS of 245bps. Meanwhile, S&P is understating AL’s fundamental credit risk, with their BBB rating three notches higher than Valens’ HY1 (BB) rating.

Fundamental analysis highlights that AL’s cash flows should roughly match operating obligations in each year going forward.

However, even after their recent debt issuances, consistent debt headwalls indicate the firm’s cash flows and cash on hand would likely fall short of servicing all obligations starting 2022, and AL will need to refinance to avoid a liquidity crunch. That said, the firm’s moderate 80% recovery rate and sizable market capitalization should allow them to access credit markets to do so.

Incentives Dictate Behavior™ analysis highlights mixed signals for creditors. Although management’s compensation framework focuses them on all three value drivers; top-line growth, margin expansion, and asset efficiency, rewards based on ROE suggest management may be biased towards growing their revenue and asset base through significant leverage.

Even so, most management members are material owners of AL equity, indicating that they are likely well-aligned with shareholders for long-term value creation. Additionally, management has relatively low change-in-control compensation, indicating they may not be incentivized to pursue a sale or accept a takeover of the firm, limiting event risk.

Earnings Call Forensics™ of the firm’s Q1 2020 earnings call (5/7) highlights that management is confident in the possibility of buying aircraft and offering sale leasebacks, and in the prospects of their work with current customers. However, they may be concerned about airline insolvencies, the strength of their balance sheet, and continued weakness in volumes.

Consistent debt maturities indicate that S&P is understating credit risk. As such, a ratings downgrade is likely going forward.

SUMMARY and Air Lease Corporation Tearsheet

As the Uniform Accounting tearsheet for Air Lease Corporation (AL:USA) highlights, the company trades at a 30.0x Uniform P/E, which is above global corporate average valuation levels and its historical average valuations.

High P/Es require high EPS growth to sustain them. That said, in the case of Air Lease, the company has recently shown a 17% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Air Lease’s Wall Street analyst-driven forecast projects a 51% and 57% EPS decline in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Air Lease’s $29 stock price. These are often referred to as market embedded expectations.

The company can have Uniform earnings shrink by 1% each year over the next three years and still justify current prices. What Wall Street analysts expect for Air Lease’s earnings growth is well below what the current stock market valuation requires in 2020 and in 2021.

Furthermore, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. This signals high credit and dividend risk.

To conclude, Masonite’s Uniform earnings growth is below peer averages and the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research