COVID-19 vaccines have been in the spotlight for AstraZeneca, but its recent acquisition should be the real story getting investors’ attention

Today’s company, Alexion Pharmaceuticals (ALXN), is an innovative pharmaceutical that specializes in rare-disease treatment, which offers a potentially great avenue for diversification of AstraZeneca’s existing portfolio.

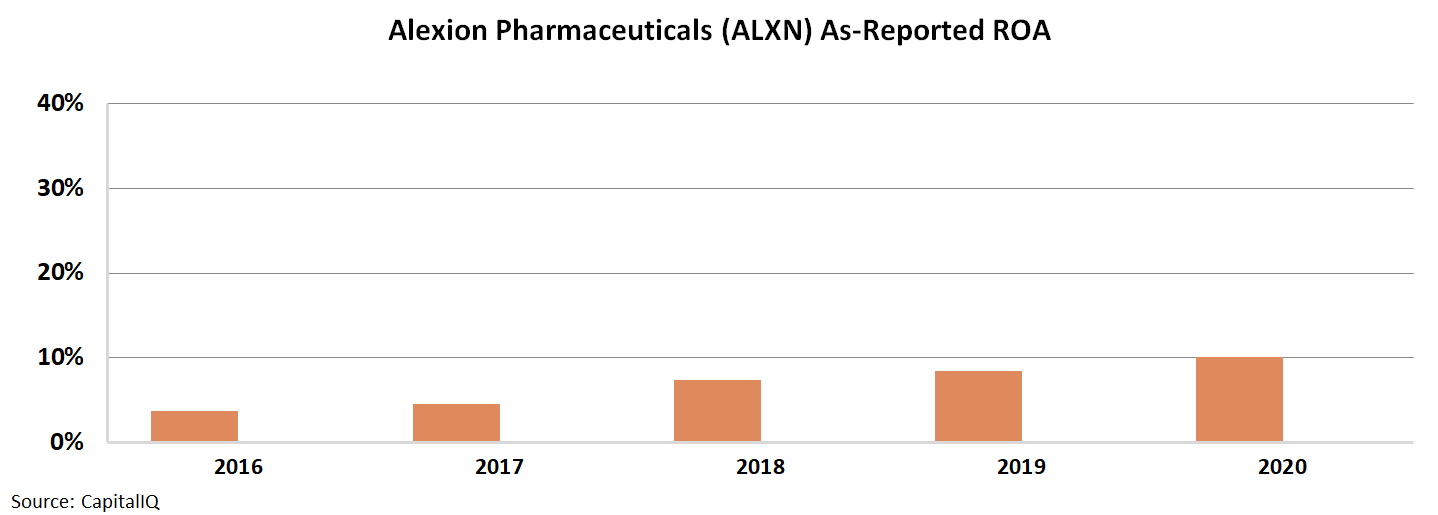

Based on as-reported results, it appears ALXN has languished over the past 5 years with weak returns and meager asset growth, supporting the market’s low valuation of the company.

Yet, when applying a Uniform Accounting lens, it becomes clear the business consistently generated high returns while not receiving any credit from the market—until now.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

AstraZeneca PLC (AZN) has garnered quite a bit of media attention over the past few months, and most of it has been pretty ugly.

Headlines surrounding possible connections between its COVID-19 vaccine and deaths related to blood-clotting seem to be circulating on a daily basis, negatively impacting the firm’s global image.

Yet, for investors, the COVID-19 vaccine is likely a transient issue. A long-term relevant issue may be whether or not the company’s recent blockbuster acquisition of Alexion Pharmaceuticals (ALXN) will be worth its $40 billion price tag.

Pending final regulatory approvals, the deal looks set to close in Q3, and may provide AstraZeneca with a high return business that may also help to diversify its revenue streams.

Unlike its acquirer, which is largely focused on major diseases in areas such as oncology, cardiovascular, and respiratory, Alexion is a niche business focused on treating rare diseases.

Rare diseases only affect a relatively small portion of the global population, and the drugs to treat them are costly to discover. As a result, they can cost patients hundreds of thousands of dollars a year.

For example, Alexion’s best-selling drug Soliris runs at over $400,000 per patient for a single year of treatment.

Despite charging hundreds of thousands of dollars for each drug, Alexion appears to generate low returns on an as-reported basis.

For example, over the past five years, Alexion has had as-reported return on assets (ROA) below 10%.

See for yourself below…

However, this is not an accurate account of Alexion’s performance over the past 5 years.

After accounting for distortions, one can observe that the company has actually been generating strong Uniform ROA levels in the 26%-39% range.

These significant discrepancies suggest that AstraZeneca acquired a high-return business at a great price, especially considering Alexion’s returns have been improving recently.

Moreover, the Uniform metrics suggest that understanding actual business performance versus relying on as-reported metrics can make a meaningful difference in determining a company’s prospects.

SUMMARY and Alexion Pharmaceuticals, Inc. Tearsheet

As the Uniform Accounting tearsheet for Alexion Pharmaceuticals, Inc. (ALXN:USA) highlights, the Uniform P/E trades at 12.3x, which is below the global corporate average of 23.7x, but above its own historical P/E of 9.5x.

Low P/Es require low EPS growth to sustain them. In the case of Alexion, the company has recently shown a 26% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Alexion’s Wall Street analyst-driven forecast is an 11% EPS shrinkage in 2021, followed by a 7% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Alexion’s $186 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 12% annually over the next three years. What Wall Street analysts expect for Alexion’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 7x the long-run corporate average. Also, cash flows and cash on hand are around 4x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

To conclude, Alexion’s Uniform earnings growth is in line with its peer averages. Therefore, as is warranted, the company is also trading around average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research