Manufacturing is coming home, bringing customers of this semiconductor supplier closer

Companies continue to invest in infrastructure and manufacturing capabilities, as the Supply Chain Super Cycle plays out.

Taiwan Semiconductor Manufacturing Co. (TWSE:2330) (“TSMC”) just announced that they will be offering advanced chips with their new plant in Arizona in 2024, as a result of the push from Apple (AAPL) and the U.S. government.

One group of companies that may be happier than the manufacturers is their suppliers, such as Applied Materials (AMAT).

The company has already increased its profitability in the last decade and is in a great position to benefit from increasing investments in the space.

However, our Embedded Expectations Analysis (“EEA”) framework shows that the market is not pricing in these developments, resulting in the undervaluation of the company.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We have been talking about how the U.S. has underinvested in its infrastructure and manufacturing capacity in the last decade.

Now with the problems with supply chains and infrastructure realized, investments in this space seem inevitable. The Supply Chain Super Cycle is underway.

We have already seen a lot of companies bringing their manufacturing facilities home from cheaper countries where they outsourced production. This will help them optimize their supply chains and decrease lead times.

Currently, we are seeing another example of this in the semiconductors space.

The White House has been stating that the U.S. produces only about 10% of the world’s semiconductor supply and none of the advanced chips. The government wants to revert this.

Following the Biden administration’s efforts and Apple’s (AAPL) push, Taiwan Semiconductor Manufacturing Co. (TWSE:2330) (“TSMC”) announced that they will offer advanced chips when its new $12 billion plant in Arizona opens in 2024.

The company is following the trend after Micron (MU), Intel (INTC), and many others ramped up their investments in the U.S.

While this development might crimp the return on assets (“ROA”) of TSMC, it means great things for suppliers of these chip manufacturers.

One of them is Applied Materials (AMAT). The company provides manufacturing equipment, services, and software to semiconductor-related industries.

It has operations in the U.S., Korea, Taiwan, China, and many other regions where chips are manufactured for the rest of the world.

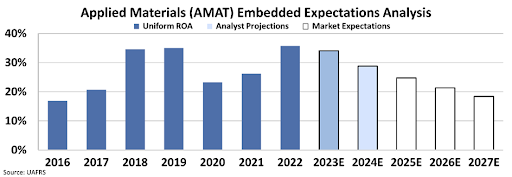

Applied Materials successfully managed to grow its operations and profitability in the last decade. The pandemic and the semiconductor shortage affected the returns a lot. However, it has shown a strong recovery since.

The Uniform ROA of the company dropped from 35% in 2019 to 23% in 2020, which was very close to 2017 levels. With the recovery in the last two years, the company managed to beat the pre-pandemic ROA of 35% slightly.

The company is in a great position to take advantage of the Supply Chain Super Cycle. New manufacturing facilities and increased capacity in the U.S. means booming demand for its products.

The company can use this advantage to grow its operations and boost its profitability.

However, we need to understand what the market thinks about the company to evaluate this as an investment opportunity. If these developments are already priced in by the market, there would be no additional value in investing.

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see what investors expect these companies to do at the current stock price.

Stock valuations are typically determined using a discounted cash flow (“DCF”) model, which makes assumptions about the future and produces the “intrinsic value” of the stock.

We know models with garbage-in assumptions based on distorted GAAP metrics only come out as garbage. Therefore, we use the current stock price with our Embedded Expectations Analysis to determine what returns the market expects.

At around $106, the market expects Applied Materials’ Uniform ROA to fall to 18%, even lower than levels seen in 2017 and during the pandemic.

Analysts are also expecting a drop in profitability, but not as much as the market thinks. They expect Uniform ROA to be 29% in 2024, slightly below the current levels.

Our Embedded Expectations Analysis makes it clear that the market is not pricing in the current developments and thinks the company is not going to benefit much from the Supply Chain Super Cycle.

There might be huge upside potential once we get through this tough downturn.

Uniform accounting and the EEA framework help us realize the mispricing in the market and spot opportunities before anyone else.

SUMMARY and Applied Materials, Inc. Tearsheet

As the Uniform Accounting tearsheet for Applied Materials, Inc. (AMAT:USA) highlights, the Uniform P/E trades at 16.2x, which is below the corporate average of 18.4x but above its historical P/E of 13.3x.

Low P/E require low EPS growth to sustain them. In the case of Applied Materials, the company has recently shown a 62% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Applied Material’s Wall Street analyst-driven forecast is a 5% and 7% EPS shrinkage in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Applied Materials’ $110 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 7% annually over the next three years. What Wall Street analysts expect for Applied Materials’ earnings growth is above what the current stock market valuation requires in 2022 but in line with its requirement in 2023.

Furthermore, the company’s earning power in 2021 is 6x the long-run corporate average. Moreover, cash flows and cash on hand are 3x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 60bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Applied Material’s Uniform earnings growth is in line with its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research