This key supplier is a great way to get sheltered against recession

We might be heading into a recession. Inflation is still a fact, and the Fed is still talking about hiking the rates a couple of more times.

This makes investing in the stock market difficult. Most companies are exposed to recession and interest rate risks and it is difficult to find opportunities. But it is not impossible.

There are well-run cheap companies that are resilient to recessionary and inflationary pressures. One of them is Ardagh Metal Packaging (AMBP). The company provides cans to the biggest beverage players in the industry.

It is a key supplier to a very stable end market. People just do not stop buying beverages, no matter how the economy is. And yet, the market has irrational concerns about its future, making the stock undervalued.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

There is still a possibility of a recession ahead.

Everybody has been talking about it for too long. Inflation is still high, rates are increasing, and the Fed has been giving signals that further rate hikes are coming.

All of this is making refinancing more difficult and debt more costly. That is if the companies can find credit.

Consumers are also getting weaker, facing surging prices and high rates on their credit cards.

This is not the ideal environment for most industries. It also makes investing in the stock market difficult, though not impossible… It is possible to find names resilient to recessionary pressures.

When people think of those stable companies, they think of the consumer staples industry. These companies provide essential products that people have to buy no matter how their financials look like and how expensive the product is.

These dynamics make the businesses incredibly stable.

However, there are a lot of companies in other sectors that can provide the same stability. One example of those is Ardagh Metal Packaging (AMBP).

Even though it is a materials company, its products are as essential as the ones of consumer staples businesses.

It is a pure-play beverage can company dating back to 1932. Its long-term contracts with more than 200 customers across more than 40 countries give it immense stability.

These customers include big beverage players like Coca-Cola, Monster, PepsiCo, Heineken, and more.

The company provides 100% recyclable products, which makes it even more attractive when all companies are trying to be greener and pay attention to their ESG scores.

The beverage industry is exceptionally stable and ever-growing. Being a key supplier to the biggest brands in the area means Ardagh benefits from the same dynamics, allowing it to be as stable as its customers.

And yet, the market seems to have concerns about the future performance of the business.

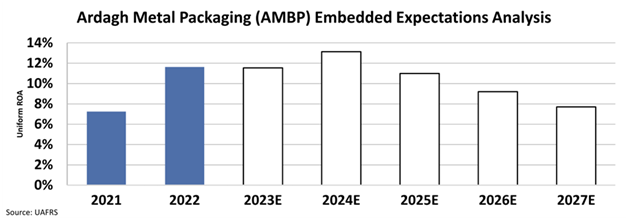

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects that the company is not going to be able to sustain its profitability, and its ROA will fall below 8%.

These concerns might be understandable. It is a consumer-centric business. If sales of these big beverage companies drop, so will Ardagh’s.

When consumers weaken in a recession, they stop spending as much as they were in the good times. They delay big projects and cancel big plans. What they do not do is stop drinking cold beverages on a warm summer day.

Ardagh serves a very stable market that is resilient to recessions. It even has the potential to grow as the beverage industry grows.

Considering these, the market seems over-pessimistic about the future of the business. As Ardagh continues to operate as it has been doing, there might be big upside potential.

SUMMARY and Ardagh Metal Packaging S.A. Tearsheet

As the Uniform Accounting tearsheet for Ardagh Metal Packaging S.A. (AMBP:USA) highlights, the Uniform P/E trades at 18.8x, which is around the corporate average of 18.4x but below its historical P/E of 21.2x.

Average P/Es require average EPS growth to sustain them. In the case of Ardagh, the company has recently shown a 746% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Ardagh’s Wall Street analyst-driven forecast is an 8% EPS growth in 2023 and a 28% EPS Growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Ardagh’s $3.73 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 4% annually over the next three years. What Wall Street analysts expect for Ardagh’s earnings growth is above what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is 2x its long-run corporate average. Moreover, cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends.

All in all, this signals high dividend risk.

Lastly, Ardagh’s Uniform earnings growth is in line with its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research