Amid solid earnings and strong data center revenues, this semiconductor firm saw its stock crater by nearly 20% after its latest earnings call

Capital expenditures for data centers are expected to surge to $7 trillion by 2030.

Given this massive rise in spending, semiconductor companies, especially those that design high-performance chips for data centers and AI-related applications are well-positioned to benefit from this windfall.

Marvell Technology (MRVL) is an example of a company that has played a pivotal role in the build-out of data centers by providing hyperscalers such as Amazon, Microsoft, Alphabet, and Meta with high-performance chips.

Despite demonstrating its ability to meet demand for high-performance chips, the company’s share price cratered by nearly 20% since its earnings call on August 28, after it narrowly missed revenue expectations and failed to impress investors with its second quarter results.

While this reaction from the market may seem overblown, Uniform accounting shows why investors reacted this way.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

Data centers are the backbone powering today’s artificial intelligence (“AI”) boom.

Without these massive facilities, the AI tools that almost every company and individual depends on wouldn’t be able to function. These physical infrastructures are responsible for housing thousands of servers that perform the millions of complex computations needed to make AI tools run.

As a result, tech giants such as Microsoft (MSFT), Meta (META), Amazon (AMZN), and Alphabet (GOOG), are in the midst of out-building and outspending each other in a bid to become the leader in today’s AI arms race.

With all this spending by the big players and other firms looking to capitalize on the AI boom, it’s forecasted that capital expenditure on data centers will balloon to as much as $7 trillion by 2030.

Given this surge in spending, semiconductor companies, especially those that specialize in designing chips for data centers and AI-related applications, are well-positioned to take advantage of this windfall.

Marvell Technology (MRVL) is an example of a company that has played a pivotal role in the build-out of data centers by providing clients with high-performance chips.

This semiconductor firm designs and provides chips for a variety of applications, ranging from chips used in cell towers to network chips used in smartphones, automobiles, and home and enterprise Wi-Fi networks.

Despite this wide range of applications for its chips, Marvell is commonly associated with its development and creation of application specific integrated circuit (“ASIC”) chips which are used in data centers.

ASIC chips are highly sought after because these can be customized to perform specific processes without sacrificing performance and power efficiency. Even though these chips function differently from the graphics processing units designed by Nvidia (NVDA), ASICs play an important part in AI-related workloads.

By supplying its power-efficient and customized ASIC chips to hyperscalers such as Amazon, Microsoft, and Alphabet, Marvell has carved a place for itself in the AI chips market despite being considered as a close second to Broadcom (AVGO).

And with capital expenditures expected to reach trillions in the next few years, investors have high hopes for Marvell despite its standing as the number two in its industry.

However, the company has failed to live up to these expectations.

During its earnings call for the second quarter of fiscal 2026, Marvell reported a revenue of $2 billion, up 58% year over year, driven by a 69% surge in its data center segment. However, this narrowly missed consensus estimates of $2.01 billion.

Its data center segment was the company’s largest end market as it contributed 74% of revenue. The remaining 26% of revenue came from segments such as enterprise networking, carrier infrastructure, consumer, and automotive.

While encouraging on the surface, Marvell’s second quarter revenue fell short of analyst estimates by $10 million, resulting in its stock price falling nearly 20% since reporting earnings in late August.

While a $10 million miss for a company that generated $2 billion in revenue seems like a marginal miss, it can result in significant reactions when investors place sky-high expectations on a company.

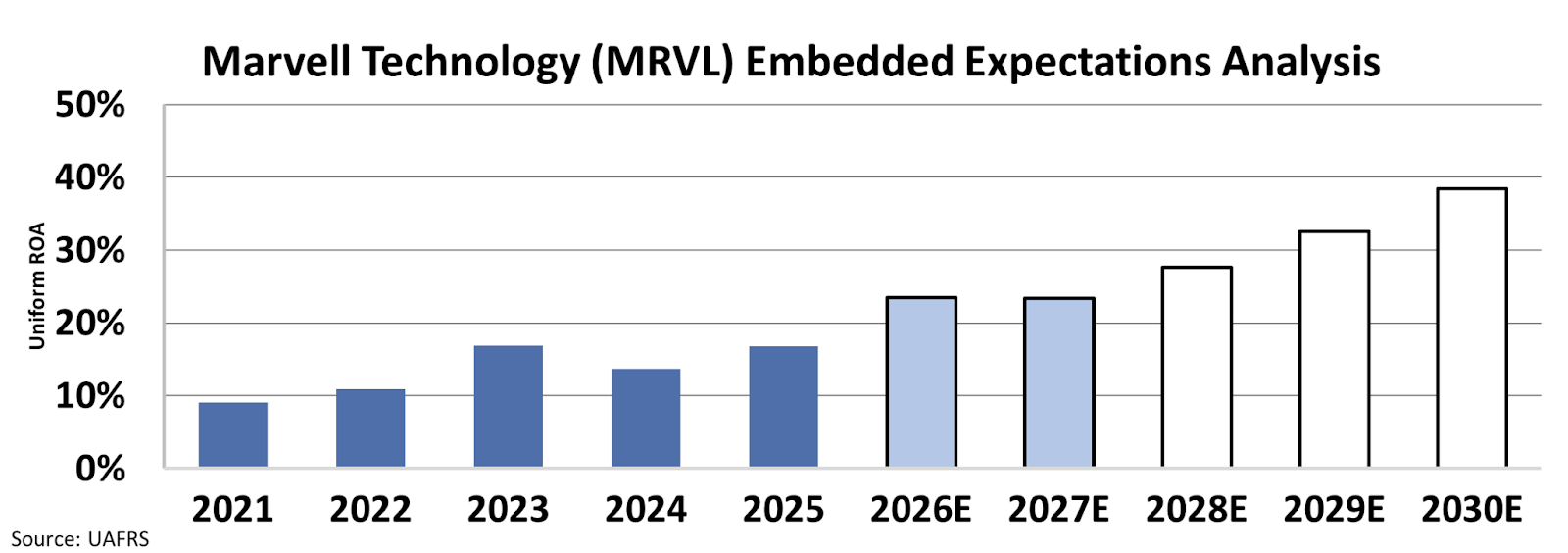

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

Since 2021, Marvell’s Uniform return on assets (“ROA”) has steadily climbed from 9% to 17%. Wall Street analysts expect returns to level out around 23% levels in the next two years, however the wider market believes Marvell will continue its ascent, with ROA expected to reach 38% by 2030.

While the company has shown it can capitalize on the booming demand for high-performance chips, investors’ current expectations are far from modest.

As a result, the market will demand nothing less than perfect execution from Marvell. If it fails to meet expectations—just like it did during its most recent quarter—investors will punish it accordingly.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research