This internet giant may finally be slowing down after a decade of high growth

The pandemic has changed the way we live. We got stuck in our homes and had to change the way we shop, work, and communicate.

This has also changed the corporate landscape. Some companies saw a massive boost in demand, while others failed.

One of the biggest beneficiaries was Amazon (AMZN). It saw a surge in demand for both its retail and web services businesses.

However, it hasn’t been going well since. People are not sitting at home shopping as much as during the pandemic, and the SaaS boom is winding down.

The market sees these tailwinds weakening and thinks Amazon’s growth will slow down.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The pandemic changed a lot of dynamics affecting various businesses.

We call this the At Home Revolution. People got stuck in their homes, changed their shopping behaviors, and found new ways of working and socializing.

At the same time, governments all around the world implemented limitations on public spaces, sometimes requiring masks to be worn or Covid tests to be taken.

These changes had contrary impacts on different sets of companies.

Some improved their margins and saw increasing demand for their products and services, while some others went bankrupt.

One of the big beneficiaries was Amazon.com (AMZN), and it has seen growth in two different ways.

The first was the strong demand for e-commerce. As people couldn’t go outside to buy, they ordered everything online.

As the biggest player in the space, the company saw sales increase immensely all over the world.

The second was the explosion in technology services. Companies accelerated digital transformation processes and new remote work and collaboration tools were developed.

This was a massive boost in demand for Amazon Web Services (“AWS”).

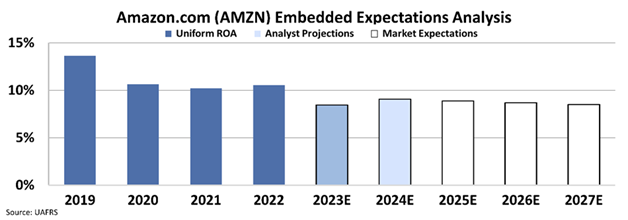

Even though Amazon had massive growth during and after the pandemic, we do not see that transform to higher profitability.

The company’s return on assets (“ROA”) has been stable at around 10% after 2020.

Since then, both these tailwinds have started to reverse…

People are not only sitting at home shopping from Amazon anymore. Additionally, people started to wake up to how much we have overinvested in software as a service (“SaaS”) solutions over the past 3 years, and really the past 15 years.

This is bad news for Amazon and means the company might face falling demand for both its offerings.

However, it is important to understand what the market thinks before using this story to make an investment decision.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At around $106 per share, the market is expecting the company’s ROA to stay flat at just below 10% going forward.

This is combined with slowing growth that had already slowed down in 2022 to continue to slow down to 12%, from consistently above 20%-30% growth historically.

This might look cheap for a company like Amazon. The market is saying that the king of e-commerce and web services will not be able to grow or improve profitability as much as it has before.

Considering the new norm of the At Home Revolution and SaaS booms winding down, it might be the right way to look at the company.

Investors need to be cautious investing in big names with an amazing history such as Amazon and should take into account the new market dynamics.

SUMMARY and Amazon.com, Inc. Tearsheet

As the Uniform Accounting tearsheet for Amazon.com, Inc. (AMZN:USA) highlights, the Uniform P/E trades at 29.5x, which is above the corporate average of 18.4x but below its historical P/E of 35.6x.

High P/Es require high EPS growth to sustain them. In the case of Amazon.com, the company has recently shown a 22% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Amazon’s Wall Street analyst-driven forecast is an 11% EPS shrinkage in 2023 and a 16% EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Amazon’s $106 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 7% annually over the next three years. What Wall Street analysts expect for Amazon’s earnings growth is below what the current stock market valuation requires in 2023 but above its 2024 requirement.

Furthermore, the company’s earning power is 2x its long-run corporate average. Moreover, cash flows and cash on hand are 1.8x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 30bps above the risk-free rate.

All in all, this signals low credit risk with no dividends.

Lastly, Amazon’s Uniform earnings growth is above its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research