Supply chain disruptions aren’t going to stop Amazon’s market dominance

The retail shopping experience in America and around the world has changed dramatically over the past 10 years.

Rather than waiting in long shopping mall lines every holiday season, consumers now have the option of ordering almost any type of good imaginable with the click of a mouse, all from the comfort of their own home.

Even in the face of current supply chain challenges, the e-commerce industry is poised to continue growing rapidly as the digital transformation takes hold of everyday economic activity.

Today, we’ll highlight one of the dominant names in the digital retail space—along with many other industries—and describe how as-reported metrics fail to capture its impressive profitability.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

For many Americans, the end of November doesn’t just mean big turkey dinners, getting together with family, and giving thanks—it also means the official arrival of the holiday shopping season.

This year however, those waiting until Black Friday to do their holiday shopping may be waiting a bit too long.

From backlogged ports and skyrocketing shipping container prices to a shortage of truck drivers, the issues that have been clogging global supply chains for over a year now seem poised to disrupt the busiest shopping time of the year.

Despite the concerns, no matter when you start your holiday shopping spree, one company is confident they’ll continue to deliver to consumers.

That company, unsurprisingly, is Amazon.com (“AMZN”)—the $1.8 trillion e-commerce giant that over the past decade has revolutionized the way consumers shop.

Amazon has become an absolutely dominant force in not only the retail industry, with its Amazon.com marketplace, but also in the economy as a whole.

By entering the cloud computing space with Amazon Web Services (“AWS”) in the mid-2010s, Amazon essentially embraced the idea that the total addressable market (“TAM”) for its services is now the entire global economy.

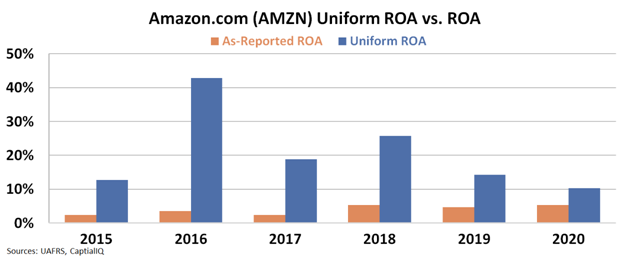

Yet, using as-reported financial metrics, it looks like even during the best of holiday shopping seasons, Amazon’s desire to provide everything to everyone leads it to operate some low-return businesses, pressuring the company’s overall profitability.

In fact, generally accepted accounting-based metrics show a company whose return on assets (“ROA”) has never been above 5% over the past decade. In other words, Amazon looks like a company operating barely above average cost-of-capital levels—which stand at 4.8% in the U.S.

If you don’t believe us, see for yourself below.

In reality, Uniform Accounting metrics highlight that Amazon’s dominant position in some of the key industries of the future makes it a much higher-return business than as-reported metrics suggest.

Rather than a cost-of-capital business, Amazon has generated double-digit Uniform ROA each year over the past 5 years and has consistently grown its assets by around 25%, tremendous growth for a company of its size.

Uniform Accounting removes the illusions of as-reported metrics that Amazon is an average cost-of-capital business.

Providing consumers the ability to order and receive essentially any product imaginable at the click of a button, along with innovative offerings for businesses in areas like cloud computing, makes Amazon a money minting machine.

SUMMARY and Amazon.com, Inc. Tearsheet

As the Uniform Accounting tearsheet for Amazon.com, Inc. (AMZN:USA) highlights, the Uniform P/E trades at 56.7x, which is above the global corporate average of 24.0x and its historical P/E of 43.5x.

High P/Es require high EPS growth to sustain them. In the case of Amazon, the company has recently shown a 5% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Amazon’s Wall Street analyst-driven forecast is for EPS to grow by 13% and 20% EPS in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Amazon’s $3,696 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 33% annually over the next three years. What Wall Street analysts expect for Amazon’s earnings growth is below what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power in 2020 is 2x above the long-run corporate average. Moreover, cash flows and cash on hand are nearly 2x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

Lastly, Amazon’s Uniform earnings growth is in line with peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research