Analysts are looking at all the wrong signals to understand inflation

News organizations and pundits are rife with speculation about the risks of inflation. Last week, markets took a tumble as the Fed talked about raising rates partly to curb excess inflation.

However, inflation itself has a huge impact on stock market valuations. As investments are savings for the future, if currency values plummet then investments will be worth less, driving down prices. While many investors are fearing this outcome, money managers shouldn’t jump to conclusions.

Today, we are going to look at the risk of prolonged inflation, and how you should invest around this risk going into 2022.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Going shopping has never been this expensive.

You may have come across headlines in the past year highlighting how inflation has been a bigger concern than it has at any time in recent history.

While we have seen the market rebound faster than any of us expected, the inflation rate has skyrocketed right alongside it.

These discussions about inflation have centered around increases seen in categories like used cars, oil, and rent.

However, a big category has often been left out of the conversation.

Due to a confluence of bottlenecks, food prices were up 40% year over year in May 2021. Supply chain disruptions from the “farm” to the “plate” have meant prices have spiked.

Perishable foods such as fruits and vegetables need rapid transportation to grocery stores, which means refrigerated transportation costs are soaring.

Shortages in truck drivers mean grocery store distribution networks are paying higher fees to get any food across land routes. Meanwhile, huge rate hikes in dry bulk ships for items such as grains or sugar that travel across the ocean has meant many inputs are undergoing price hikes.

The result has been that a lot less has arrived at its destination on schedule.

Another factor that has challenged the food industry even before the coronavirus pandemic was the 2018 swine flu outbreak in China.

The outbreak forced China, a vital global supplier, to cull half its pig herd. It took more than two years to rebuild stocks to replace the lost pigs. This has created even more shortages as the pig population is still recovering.

Some experts worry that signs of an outbreak with a new coronavirus variant in 2022 could destabilize the food and livestock industry with more disruptions.

There don’t appear to be any easy solutions to remedy these problems in the food industry. Unfortunately, none of it looks likely to resolve in the near term. High prices are here to stay.

However, high prices today don’t mean high prices tomorrow. It is important to note that there is another side to the story.

Even as prices stay high, particularly in perishables like food, it is important to note that many of these prices have started to stabilize. Items such as orange juice, sugar, soybeans, and corn, just to name a few, are seeing prices level off.

While prices remain elevated, if prices stick where they are, inflation itself is tapering.

Annualizing these spikes becomes important as we look at the potential of stabilization in the markets.

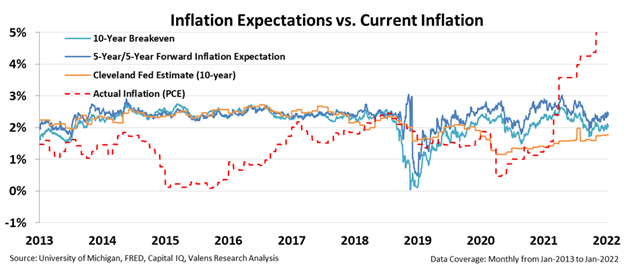

In the chart below, The dotted red line is actual inflation, or personal consumption expenditure, which tracks prices themselves. This has spiked as food prices have climbed the past year.

However, the light and dark blue lines represent the 10-year inflation expectations, which remain flat and have even trended down over the past year. As supply chains ease, prices will flatten and come back down to normal levels, not continue to climb.

News outlets use our understanding of inflation, or protracted price increases thanks to monetary policy, to talk about the current, short-term phenomenon happening in the current overheated economy.

While inflation numbers have risen significantly in the past year, these rates will taper off and should fall in the long term.

Thanks to pandemic shutdowns declining and large corporate investments in supply chain infrastructure, companies will begin to lower prices as they seek to undercut the competition. That is why inflation expectations in the long term remain low.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research