Analysts are looking to crack open “fedspeak” to model inflation

Investors and the financial media are trying to decipher how long Federal Reserve Chairman Jerome Powell and the rest of the Federal Open Market Committee will tolerate higher inflation.

Money managers and analysts want to know when the Fed will use its most powerful tool – interest rates. By raising interest rates, the Fed can rein in elevated prices that producers and consumers are facing.

Today, we will use one of our more esoteric tools in our toolbox to figure out exactly what the Fed thinks of the current inflationary environment.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

The debate around inflation rates is the hot-button topic of 2021. Some call for the Fed to raise interest rates sooner to ensure higher prices don’t become embedded into people’s minds. Even the idea of inflation, if held by enough people, can start an inflationary spiral. It’s what we saw in the U.S. during the Great Inflation of the 1970s.

Others are concerned the economy might get stuck in a period of stagflation, a situation where there is both high inflation and high unemployment, accompanied by slow growth. This presents challenges for policymakers because they may have to choose policies to deal with inflation (like raising interest rates) that only exacerbate growth issues and vice versa.

Stagflation worries stem from the potential that current supply chain issues become more longer-lasting than expected. This could lead corporate management teams to refrain from investing, leading to continued price pressures.

Here at Valens, we have a more sophisticated way of gaining insights into the vague world of “Fedspeak,” a term meant to describe the central bank’s intentional ambiguity.

Thanks to our Earnings Call Forensics (“ECF”) analysis, we can obtain a window into what Powell – and corporate management teams – are thinking.

Recently, we had the team review previous Fed meetings, and some signals from their July press conference were revealing. Powell was particularly confident that pricing surges in energy, lumber, and other inputs look transient.

On top of that, Powell was confident he doesn’t believe the current inflationary issues are likely to last longer than 12 months or that consumers will start to expect higher inflation going forward.

Like what we’ve been telling our readers, the Fed chairman was also confident that a supply shock drives price pressures. It’s not the sort of wage-price spiral dynamic that should be a concern for the economy and investors.

Insight into what Powell and other Fed officials are thinking about inflation is important. That’s because inflation rates are central to understanding what valuations are warranted in the market.

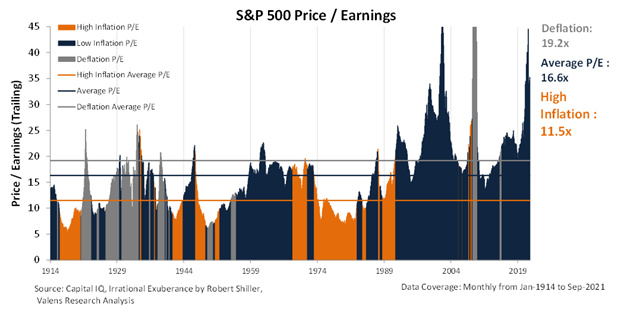

When inflation is higher, it generally means lower price-to-earnings (P/E) ratios for the market. Real returns are being eaten away by the rising cost of goods and services.

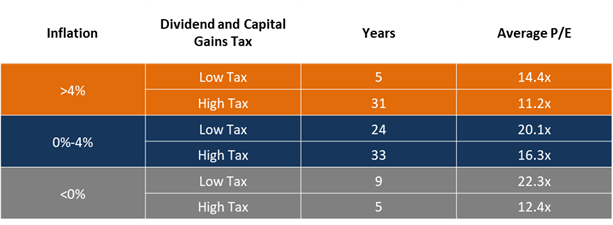

When inflation is above 4% for a sustained period, even in a low tax environment like the one we’re currently in now, market prices suffer. In this environment, investors are looking at a 14.4 times average P/E rather than 20.1 times when inflation is between 0% and 4%.

See the historical data for yourself below…

For a more tangible representation of how low P/E levels can impact your portfolio, take a look at the chart below. The orange represents times with high inflation over the past 100 years, when market valuations were pushed lower.

With Powell’s recent signals, we can have confidence that we’re not about to enter either an inflationary spiral or stagflation in the near term… that would lead to lower market valuations and slower earnings growth.

When current price pressures abate, the healthy credit environment and strength of corporate profitability in the U.S. can continue to support market valuations at the higher end of historical averages.

As we keep telling readers, given the current inflation dynamics, investors should allow the market noise to clear and continue to take advantage of opportunities to buy the dip.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research