The DOJ saw something in this massive merger many might have missed, and put its foot down

Today, we are talking about a merger that would have transformed an industry that millions of Americans are reliant on.

However, the DOJ put its foot down and the deal fell through. Uniform Accounting may help us understand why the company-to-be would have been a threatening monopoly.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Despite once being a hot-button issue, much of the country has come together in agreeing that competition is indeed being blunted by colossal oligopolies.

Many of these behemoth companies didn’t organically grow into their shoes, but acquired their way up using a variety of strategies.

For example, big fish like Facebook (FB) are constantly on the hunt to acquire tiny, forward-thinking startups like Instagram that could one day become a thorn in their side. Alternatively, massive horizontal mergers, like T-Mobile (TMUS) and Sprint in 2020, were another lucrative way to grow.

We just witnessed one such horizontal merger get spectacularly derailed by the Department of Justice (DOJ).

The corporate insurance brokerage business is dominated by three big fish: Marsh and McLennan (MMC), Aon (AON), and Willis Towers Watson (WLTW). Had the DOJ not stepped in, the pool would have shrunk to just two, following an in-process merger by Aon and Willis Towers Watson. The new company would have surpassed Marsh and McLennan to become the undisputed elephant in the room.

Part of why the DOJ felt it was necessary to block the merger is these brokers serve an important role in the lives of millions of Americans.

For most Americans working at large companies, chances are that their health insurance, retirement, or benefits plan was either brokered by or sold by Marsh McLennan, Aon, or WIllis Towers Watson. The DOJ claimed that the new company would have had the market dominance to significantly raise prices or lower the quality of their products, without worrying too much about what the competition is doing.

Aon, in fact, didn’t even wait for the regulators to officially bring the hammer down. The merger was voluntarily called off less than a month after the DOJ’s antitrust suit was filed.

The company vehemently disagrees with the DOJ’s calculus about how the merger would impact competition and innovation. But, it also says it wasn’t willing to wait for the scheduled court date, deep into next year, to resume the process. The time and money lost wouldn’t be worth it. As it turns out, Aon and Willis are both focused on operational efficiency.

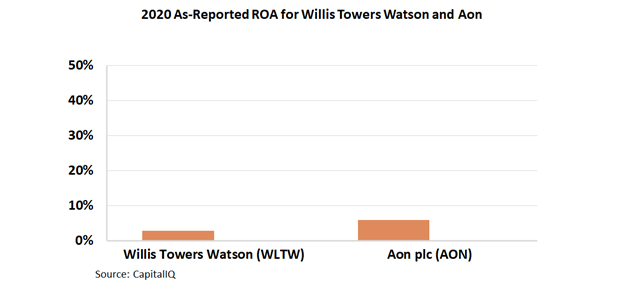

To many, this may come as a surprise. These corporations aren’t usually thought to be bastions of efficiency. This, however, may be a fault of how companies report their finances.

If you looked at Aon and Willis Towers Watson’s as-reported ROAs, you’d find them to be slow, unproductive businesses, barely capable of delivering more value than the cost-of-capital.

If this is the picture that regulators saw and believed, they might have let the merger go on under the assumption that two mismanaged companies aren’t taking enough of a profit to threaten pricing power.

However, due to a slew of deficiencies inherent to the American rules for financial reporting, the real picture is rather different.

Both companies have impressively strong Uniform ROA well above the corporate average. This is because well-managed companies can use their scale to boost profitability.

Over the past decade, Aon has doubled its Uniform ROA to over 40%, and Willis has held Uniform ROA steady at 20%-35% levels.

Take a look at how their 2020 performance actually looks, once you remove the accounting noise:

If these companies were to combine, they would integrate the operational efficiencies they’ve each learned over the years. Willis would certainly stand to benefit from the deal, as Aon’s management team works their magic on the new firm.

Marsh McLennan, which also boasts 40% Uniform ROA, would then become the underdog, with only one adversary to compete with rather than two. This opens the door to oligopolistic price-setting, and further increases the barrier that new firms face in the insurance brokerage business.

The DOJ, which has a devoted team of forensic accountants and analysts who have spent hundreds of hours analyzing the potential impact of the deal, clearly recognized that the new combined business would have not just been too large, but also a lean and mean economic powerhouse.

With the tools we’ve built at Valens Research, you could see the same thing in a matter of minutes.

SUMMARY and Aon, Inc. Tearsheet

As the Uniform Accounting tearsheet for Aon plc (AON:USA) highlights, the Uniform P/E trades at 22.2x, which is around the global corporate average of 23.7x but above Aon plc’s historical P/E of 19.9x.

Moderate P/Es require moderate EPS growth to sustain them. That said, in the case of Aon plc, the company has recently shown a 23% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Aon plc’s Wall Street analyst-driven forecast is an 8% and 7% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Aon plc’s $260 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 1% annually over the next three years. What Wall Street analysts expect for Aon plc’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power in 2021 is 7x the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

To conclude, Aon plc’s Uniform earnings growth is in line with its peer averages, while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research