Despite what appears to be stiff competition, this firm secretly dominates the water heater market

In this market, investors are under the impression competitors are forced to fight tooth and nail for customers. Today’s firm has been able to dominate the space.

By viewing the incorrect data, investors are blinded to this giant’s true power selling some of the best water heaters on the market.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

A large part of the At-Home Revolution surge has been propelled by individuals investing capital into their existing homes and new homes soon after the purchase.

Most of the conversation around these investments focuses on replicating something from the outside world.

Instead of going to the movies, people are investing in home theater systems. Rather than working from the office, workers have invested in work-from-home setups.

While this is a huge component of the At-Home revolution, there’s also huge demand for upgrading existing systems in the home.

Just one example of this type of feature is a home water management system. As individuals are spending more time in their homes, they want to make sure they are getting safe, clean water at any temperature.

Some companies that homeowners turn to for the best quality solutions for home improvement include names like American Water Heaters, Lochinvar, Reliance, GSW, and many more.

Another favorite brand in the ecosystem is A.O. Smith. A.O. Smith’s products include residential and commercial gas and electric water heaters and boilers.

All together in the water heater and boiler side of the industry, these brands control over 40% of the market for both residential and commercial offerings.

On the surface, the water management market sounds competitive. There’s no clear brand monopoly.

That is, until you realize all of these brands are owned by the same firm, A.O. Smith Corporation (AOS).

A.O. Smith is another example of a firm that benefits from the illusion of choice given to customers. This is a market advantage we have discussed before at Valens.

When buying these products for homes, customers believe they have many different options at different prices and features across the industry. In reality, customers are really buying all their products from A.O. Smith.

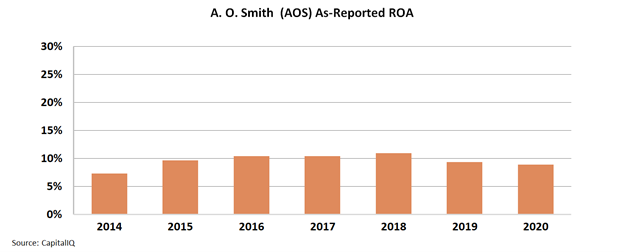

Using as-reported accounting, it’s difficult to say if this massive market share is of any benefit for the firm.

Specifically, as-reported return of asset (ROA) figures highlight A.O. Smith has not been able to sustain returns north of 10% over the past seven years.

By looking at as-reported metrics, investors might conclude that this stock generates returns lower than the corporate average.

See for yourself below.

In reality, this is not an accurate picture of A.O. Smith’s performance. The firm’s dominant market share in both the residential and commercial segments has allowed it to earn above average returns for its services.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business model is better than it seems.

Since 2014, the company’s returns have never dipped below 20%.

Considering the tailwinds for the company’s end market, these returns are unlikely to fade anytime soon, contrary to the as-reported metrics.

Without Uniform Accounting, investors would be unsure of the true power A.O. Smith has unlocked from the “illusion of choice” within the heater and boiler segment of the At-Home Revolution trend.

SUMMARY and A. O. Smith Corporation Tearsheet

As the Uniform Accounting tearsheet for A. O. Smith Corporation (AOS:USA) highlights, its Uniform P/E trades at 20.6x, which is below the global corporate average of 25.2x, but around its own historical average of 20.5x.

Low P/Es require low EPS growth to sustain them. That said, in the case of A. O. Smith, the company has recently shown a 15% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, A. O. Smith’s Wall Street analyst-driven forecast is a 10% and 7% EPS growth in 2020 and 2021, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify A. O. Smith’s $54 stock price. These are often referred to as market embedded expectations.

A. O. Smith is currently being valued as if Uniform earnings were to grow 2% annually over the next three years. What Wall Street analysts expect for A. O. Smith’s earnings growth is above what the current stock market valuation requires through 2022.

Furthermore, the company’s earning power is 4x the long-run corporate average. Also, intrinsic credit risk is 40bps above the risk-free rate and cash flows and cash on hand are more than twice its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low dividend and credit risk.

To conclude, A. O. Smith’s Uniform earnings growth is in line with peer averages, but the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research