Gold miners weren’t the true winners of the gold rush. This company is using the winners’ playbook for the Internet of Things

With the technological advancements and innovations consistently taking place in the IoT space, the connectivity and strength of products has never been more important.

The power of this company becomes clear when investors understand that being a supplier to the At-Home Revolution IoT space can be compared to a historical example. During the California gold rush, mining the gold itself wasn’t the business where all the money is made.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

When most people think of the Internet of Things (IoT), they immediately think of roombas, Amazon’s Alexa, or a self-driving car.

These physical items with internet connectivity are so recognizable, since they are the front end final products and brands that give the IoT space most recognition.

For example, Amazon (AMZN) owns 70% market share of the U.S. smart speaker market, and there are currently 100 million devices connected to an Amazon Alexa.

Additionally, iRobot (IRBT) estimates that more than 20% of all vacuums in the market today are now robotic, with over 14 million Roombas sold to date.

With all these technological advancements and innovations taking place, competition and new companies within the IoT space is as great as it has ever been.

This means trying to determine which SmartHome provider is going to win, which autonomous vehicle company will win the race, and which smart factory implementor is going to dominate others is a challenging prospect.

Investors should take a page out of the history books to take advantage of the IoT wave. In the California gold rush, everyone wanted to be a gold miner, but few found the precious metal. Meanwhile, the suppliers to the prospectors, such as the pickaxe sellers, were the winners.

To do this correctly in the IoT space, investors need to find the companies that make sensors, radio antennas, power supplies, connectors, and cables, or the equipment that will be crucial for any IoT name.

Unlike Alexa or the Roomba, these products operate in the background of the IoT wave. As a result, investors might expect a company that makes these products to have low returns.

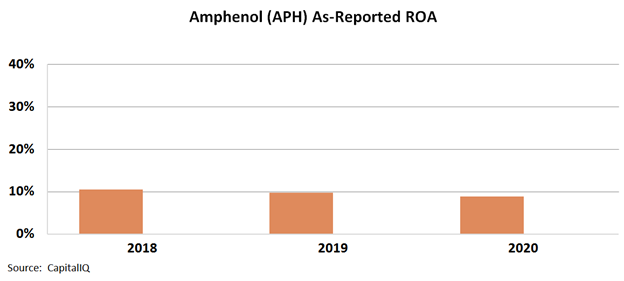

A large producer in the space, Amphenol (APH), appears to fall into this basket. The company’s as-reported metrics have been in a declining trend over the past few years. Specifically, Amphenol’s return on asset (ROA) levels have declined from 11% in 2018 to 9% in 2020.

See for yourself below.

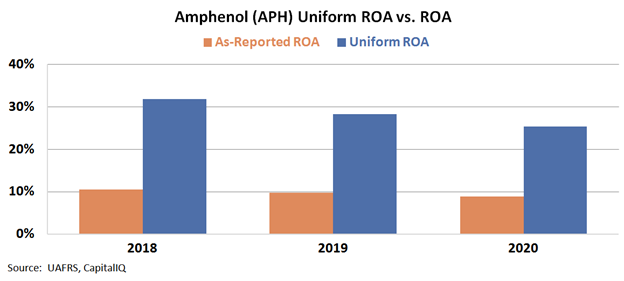

In reality, these low profitability levels are a complete distortion.

The company’s returns are not actually below the U.S. corporate average. In reality, Amphenol is essential and has carved out a vital niche for itself.

With these competitive advantages, the company generates more impressive returns.

Specifically, the company’s current ROA levels are around 25% after making adjustments to poor accounting practices.

The strength of Amphenol becomes more clear when investors understand that being a supplier to the Internet of Things gold miners, selling them their products, is a lucrative business to be in.

SUMMARY and Amphenol Corporation Tearsheet

As the Uniform Accounting tearsheet for Amphenol Corporation (APH:USA) highlights, the Uniform P/E trades at 30.3x, which is above global corporate average valuation levels of 23.7x and its historical average valuations of 26.7x.

High P/Es require high EPS growth to sustain them. In the case of Amphenol, the company has recently shown a 2% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Amphenol’s Wall Street analyst-driven forecast is an EPS growth of 10% in 2021 and 7% in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Amphenol’s $68 stock price. These are often referred to as market embedded expectations.

Amphenol is being valued as if Uniform earnings will be growing 10% annually over the next three years. What Wall Street analysts expect for Amphenol’s earnings growth is near what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is 4x the corporate average and cash flows and cash on hand are nearly 3x its total obligations—including debt maturities and capex maintenance. Together, this signals a low credit risk.

To conclude, Amphenol’s Uniform earnings growth is below peer averages, but well above peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research