This water management company is helping the oil and gas industry thrive from undergrounds

The U.S. oil and gas industry is still strong. With increasing demand from Europe, American oil and gas manufacturers are getting ready for a decade of high exports.

While the industry is competitive, there are those that help the industry thrive while having less competition.

Aris Water Solutions (ARIS) is one of them. It owns pipelines in the Permian Basin that help transfer the water to and from the fracking sites. Oil and gas companies have to use these if they don’t want to bring water each time with tanks.

Aris saw its returns skyrocket over the last few years and is likely to continue having high returns as the U.S. oil and gas industry remains strong.

Yet, the market fails to see the story, causing undervaluation.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The U.S. oil and gas industry is still up and running.

After the Russian invasion of Ukraine, Europe started looking for different sources to get energy from.

We have been talking about the big chance the U.S. has with its massive reserves and how this situation will start another Shale Renaissance.

This has really come true. U.S. LNG exports to Europe surged from 3 billion cubic feet per day in 2021 to more than 7 billion cubic feet per day in 2022. This is more than a 120% increase.

In the meantime, oil and gas companies in the U.S. thrived. Not only did they sell higher volumes, but they also sold them for higher prices as energy became more expensive.

Being by far the largest producer of natural gas in the world and sitting on insanely big shale gas reserves, it is likely that U.S. exports to Europe continue strong as long as they don’t start buying from Russia.

As this happens, American companies will continue to realize high demand and generate high returns.

Like most others, oil and gas is a competitive industry. Companies compete for new resources, securing contracts and customers. It might be difficult to pick a winner in this case.

Although, sometimes it is possible to find winners such as Aris Water Solutions (ARIS).

The company allows the oil and gas companies to work efficiently. Water is an essential input and output of fracking operations. Aris brings water for fracking and handles used water with its pipelines and facilities around the Permian Basin.

It is essentially a utilities company for oil and gas companies. The alternative for them is to use tanks to bring and get rid of water, which is more expensive and difficult operationally.

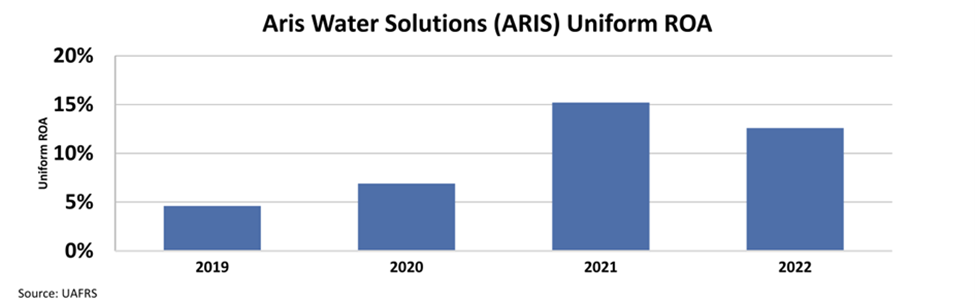

Thanks to Aris’ focus on recycling and reselling water, and increasing water volumes, the company’s cost per barrel produced went down significantly.

Combined with increasing prices, its return on assets (“ROA”) skyrocketed from under 5% in 2019 to 15% in 2021 and was still above 12% in 2022.

The company provides an essential service to an industry that is poised to remain strong, especially with the demand from Europe.

And yet, the market does not think Aris is going to be able to sustain high profitability.

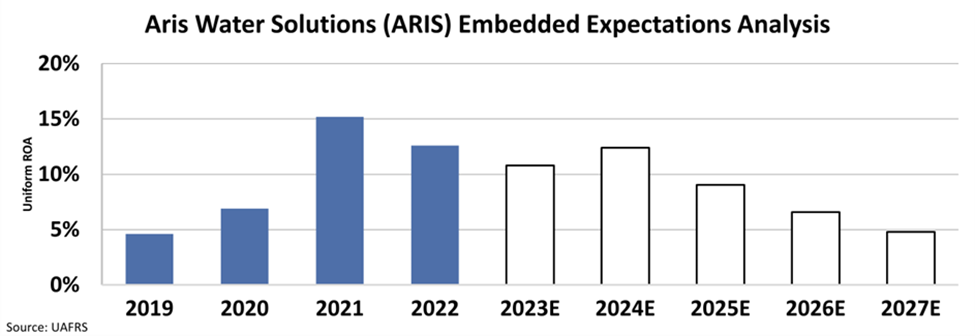

We can see this through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to collapse back to 2019 levels below 5%.

Aris has proven it can reach high returns when the oil and gas industry is strong. It has strategic pipelines in one of the biggest basins in the country, making its services irreplaceable.

Additionally, its focus on recycling water and reselling made its cost per barrel fall significantly, affecting profitability positively.

Considering these, the market’s expectations of falling ROA seem pessimistic. In a more realistic scenario, Aris is likely to have higher returns for a longer time.

This pessimism causes mispricing that opportunistic investors can benefit from.

SUMMARY and Aris Water Solutions, Inc. Tearsheet

As the Uniform Accounting tearsheet for Aris Water Solutions, Inc. (ARIS:USA) highlights, the Uniform P/E trades at 13.4x, which is below the corporate average of 18.4x but above its historical P/E of 11.4x.

High P/Es require high EPS growth to sustain them. In the case of Aris, the company has recently shown a 23% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Aris’ Wall Street analyst-driven forecast is a 20% EPS shrinkage in 2023 and a 41% EPS growth in 2024.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Aris’ $10.23 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 3% annually over the next three years. What Wall Street analysts expect for Aris’ earnings growth is below what the current stock market valuation requires in 2023 but above its 2024 requirement.

Furthermore, the company’s earning power is 2x its long-run corporate average. Moreover, cash flows and cash on hand are 1x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company has no risk to their dividend.

All in all, this signals low dividend risk.

Lastly, ARIS’ Uniform earnings growth is immaterial with its peer averages but above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research