Coal is back, and Alliance Resource Partners is ready to supply it

The Russian invasion has caused a shift in macroeconomic dynamics around the world. We have talked before about how this could benefit the U.S. natural gas companies. Now there might be another winner.

European countries looking to reduce their energy dependency on Russia are now turning back to coal. This move increases the interest in coal production companies such as Alliance Resource Partners (ARLP).

Despite global efforts to stop burning coal over the last decade, the company now has a huge opportunity to become the energy supplier of Europe. To see just how much Alliance is set to profit, we can turn to Uniform Accounting.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Due to the Russian invasion of Ukraine, the world has seen the prices of food, energy, and rare metals rise due to supply chain issues caused by the war.

The prices of crude oil and wheat rose by 37% and 65% respectively in the two weeks following the beginning of the invasion. While grain is starting to normalize, energy prices have been more stubborn.

We have been highlighting over the past few months how the U.S. natural gas companies are poised to pick up the slack in European energy without Russian exports.

These companies are not the only winners though. U.S. coal companies have a huge opportunity waiting for them in the short term.

Countries like Germany are looking for ways to reduce their energy dependency on Russia, as Germany is looking to stand tall with its NATO allies and can no longer rely on steady shipments from Moscow. As Germany’s Economy Ministry explained, one way of doing this is turning back to coal.

A big winner of this recent news is Alliance Resource Partners (ARLP). The company is a diversified natural resource extractor focusing on coal production and oil and gas mineral interests.

92% of the company’s revenue was generated from its coal operations in 2021, while the rest came from mineral and royalty interests.

Being on the wrong side of the transformation to greener sources of energy, Alliance Resource Partners has been seeing profitability collapse over the last decade.

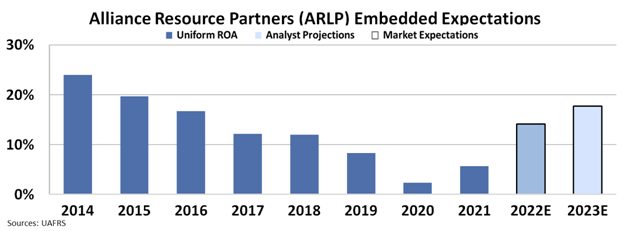

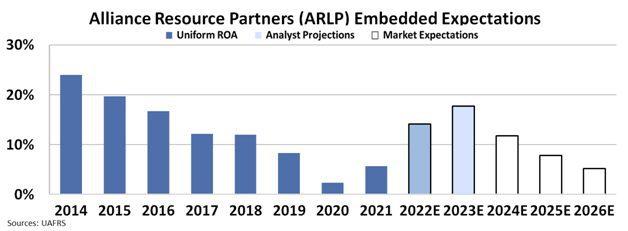

The Uniform return on assets (“ROA”) dropped from 24% in 2014 to just 2% in 2020, before jumping to 6% in 2021 as energy demand spiked following lockdowns ending.

Analysts think that the recent jump is just a tiny preview of things to come. They expect the company to see returns hit 18% by 2023 due to rising coal consumption.

These expectations certainly make the investors excited. However, investing without knowing what the market thinks would be acting blindly.

By utilizing our Embedded Expectations Analysis (“EEA”) framework, we can see how investors expect a company to perform at the current stock price.

At valuations around $20 per share, the market is still pricing Alliance Resource Partners for the inevitable crash in coal that will happen as it is dying. The expectations are for the company’s ROA to fall below 5% levels going forward.

If current disruptions in the global energy market continue and Europe acts on its word to walk away from Russian natural gas, the market is missing out on a major opportunity.

Investors would not be able to see this mispricing and act upon it without the Uniform Accounting and our EEA framework.

SUMMARY and Alliance Resource Partners, L.P. Tearsheet

As the Uniform Accounting tearsheet for Alliance Resource Partners, L.P. (ARLP:USA) highlights, the Uniform P/E trades at 7.0x, which is below the global corporate average of 19.7x and its own historical P/E of 16.9x.

Low P/Es require low EPS growth to sustain them. In the case of Alliance Resource Partners, the company has recently shown a 555% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Alliance Resource Partners’ Wall Street analyst-driven forecast is a 236% and 17% EPS growth in 2022 and 2023, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Alliance Resource Partners’ $20 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink by 1% annually over the next three years. What Wall Street analysts expect for Alliance Resource Partners’ earnings growth is above what the current stock market valuation requires through 2023.

Furthermore, the company’s earning power in 2021 is in line with the long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals low dividend and credit risk.

Lastly, Alliance Resource Partners’ Uniform earnings growth is above its peer averages, but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research