As-reported metrics distort this military contractor’s true profitability

Rising global tensions result in the market focusing on military contractors supporting defense efforts around the globe.

While most investors focus on major contractors manufacturing advanced weapon systems and other equipment, there is a $180 billion market devoted to logistics and ensuring military bases operate at peak efficiency.

Contractor V2X (VVX) specializes in this department, providing logistical support for 343 U.S. military bases across 45 countries globally.

With growing demand for military spending and a shift towards higher-margin contracts, V2X stands to benefit from current macroeconomic tailwinds.

Thus far, the market has largely doubted this company’s potential due to underwhelming as-reported financials. However, Uniform Accounting highlights investors may be underestimating this stock.

Investor Essentials Daily:

Friday News-based Update

Powered by Valens Research

U.S. military bases are massive institutions; the largest bases in the U.S. can hold well over 100,000 people while overseas bases house up to 40,000 individuals.

These bases aren’t just plots of land for the military to set up equipment and run operations from, they’re small cities with complicated logistics and a never-ending need for maintenance and behind-the-scenes operations.

This is where government contractor V2X (NYSE: VVX) specializes. Unlike most military contractors, V2X doesn’t provide products. The company offers logistic and efficiency solutions, technology integration, engineering services, and training.

V2X’s capabilities can be broken down to four main groups. Aerospace solutions involve maintaining and modifying aircraft, vehicles, and weapon systems to ensure they’re in the best condition possible. Technology solutions provide engineering, system integration, and software services needed for a base’s IT network and cybersecurity functions.

Operations and logistics provide infrastructure operations and support so that bases run as efficiently as possible. Finally, in training solutions, V2X designs and implements training programs designed to ensure personnel at a base equally prepared as the hardware and software V2X maintains.

Today, the company aids all branches of the U.S. military in 343 locations and 45 countries. With global tensions rising around the world, these overseas bases are becoming more important than ever before, emphasizing the importance of a company like V2X.

More conflict has led to more U.S. military spending. In 2005, the Department of Defense (“DOD”) was awarded $402 billion for its annual budget. Twenty years later, our defense budget has more than doubled, with the latest budget providing more than $1 trillion to defense.

In all, this gives V2X a market opportunity valued at $180 billion. Moreover, as this company looks to capitalize on its growing market, the company is also positioning itself for higher profitability going forward.

Historically, the majority of V2X’s contracts were cost-plus agreements. These contracts accounted for 68% of the company’s revenue back in 2020, while fixed contracts accounted for 29%.

While cost-plus contracts offer stable margins, fixed rate agreements present an opportunity for higher returns for V2X. This is why the company has committed to shifting its contract mix in the past five years.

Today cost-plus contracts are still V2X’s most used, however, they only account for 56% of revenue, while firm-fixed deals now make up 41% of all contracts.

Despite the company’s transformation into higher-margin contracts and significant tailwinds driving growth, the market has largely ignored V2X. The company’s stock price is up slightly more than 35% in the past five years, trailing the S&P 500 by 65%.

This may be due to investors misunderstanding this business and how its returns have improved since 2020.

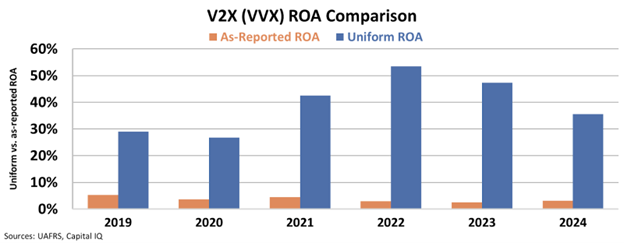

As-reported GAAP metrics present V2X as a below-average company that has declined in recent years.

As-reported return on assets (“ROA”) hovered between 4% and 5% in 2019 and 2020 – around the company’s cost of capital. Since then, as-reported returns declined to just 3% in 2024. At a glance V2X appears to be struggling to generate any profits.

However, using Uniform Accounting, investors have a clearer understanding of this company’s profitability, and how it has evolved over the years.

Uniform Accounting reveals V2X has always been more profitable than the market realizes. Uniform ROA was 27% in 2020, above both the company’s cost of capital and the 12% corporate average return.

Moreover, V2X’s ROA has improved to 36% over the past four years as V2X continued to prioritize higher-margin fixed-rate contracts.

V2X is an essential part of domestic and international U.S. military operations. While the largest defense companies grab headlines for building advanced vehicles and weapons, V2X ensures they’re ready to deploy.

The U.S. is growing its defense budget amid rising global tensions. And all the while, V2X is winning new business. Investors have largely ignored this contractor due to its concerning as-reported financials, however, Uniform Accounting highlights that this company may be one the market is misvaluing.

If V2X can continue performing at levels greater than the market perceives, it could translate into upside for investors.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research