As-reported metrics make Equifax look far less profitable than reality

As data becomes more and more essential to the world, the firms that hold it will become more powerful. Consumer credit rating companies are some of those companies that have a ton of data that everyone wants access to.

Today, we are going to take a closer look at Equifax Inc. (EFX), one of the leading consumer credit rating companies, through a Uniform Accounting lens to get a better idea to see how it’s performing in this age of data.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Data is what makes the modern economy go round. It’s essential to power so much of what we do. For a civilization built on leverage and debt to power further opportunities, underwriting data is gold.

One group of companies that has been at the heart of understanding the value and power of data is the consumer credit rating companies, including TransUnion (TRU), Experian (EXPN), and Equifax.

These firms understand that if they can paint a broader picture of our lives, they can better understand underwriting. Everyone will want that data, which should help them see strong profitability.

By tracking the credit history of borrowers, these companies can generate reports and credit scores that help determine credit risk. The reports are typically then sold to lenders as a risk profile of consumers looking to take out loans.

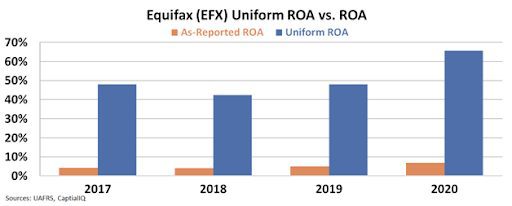

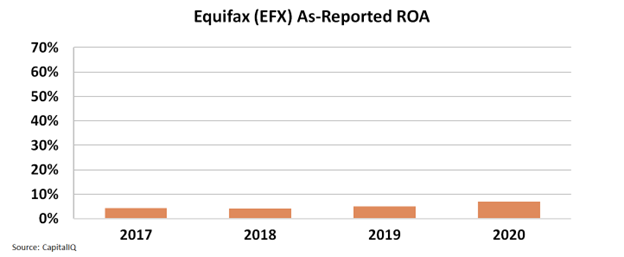

However, as-reported metrics show that desire to acquire all that data hasn’t really benefited Equifax.

Its return on assets (“ROA”) appear to have consistently been weak, sitting below 10% since 2008. But in 2017, Equifax suffered a major data breach, putting the personal information of close to half the US population at risk.

As-reported metrics make it seem Equifax is just starting to now recover from that data breach. As-reported return on assets (“ROA”) fell from 7% in 2017 to 4% levels in 2018-2019, before recovering back to 7% in 2021.

While Equifax’s profitability has seen improvement, this low level is disappointing, given the power of the data it holds.

While Equifax’s profitability has seen improvement, this low level is disappointing, given the power of the data it holds.

However, if we look at Uniform metrics, we can see that Equifax has actually been massively profitable this whole time.

While Uniform metrics show us Equifax did still take a hit following the data breach, dropping from 66% in 2017 to 42% in 2019, it never actually fell to below cost-of-capital levels. Since then, its ROA has returned to 66% levels in 2021, showing us customers still see the value in all the data the firm holds.