As-reported numbers are underestimating the upside potential of this AI enabler

Data centers serve as the backbone of the AI boom, housing thousands of servers that process vast amounts of data needed to train and run AI models.

Data centers require reliable access to electricity, advanced chips, and cooling systems. However, those aren’t the only equipment needed to run data centers smoothly.

Server racks found in data centers often operate in clusters, and in order to run smoothly, they need to be able to transfer terabytes of data efficiently. As a result, demand has grown for optical networking solutions.

And this surging demand has benefitted Ciena Corporation (CIEN), a leading provider of optical networking solutions.

Investor Essentials Daily:

Thursday News-based Update

Powered by Valens Research

Data centers serve as the backbone of today’s AI boom.

They house thousands of servers that process the vast amounts of data needed to train, develop, and run AI models smoothly.

Since these structures run millions of AI-related tasks each day, they need reliable access to electricity, fleets of advanced chips, and efficient cooling systems. However, those aren’t the only things data centers need to run smoothly.

Data centers house thousands of server racks that need to be connected to each other in order to function and communicate efficiently as clusters. And while copper has been the mainstay of data center connectivity, operators have shifted to optical networking solutions due to the massive scale and speed requirements needed in AI-related workloads.

Major hyperscalers like Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN), and Meta (META) are forecasted to collectively spend $600 billion on AI infrastructure this year, positioning Ciena Corporation (CIEN), a leading provider of optical networking solutions, to benefit from this spending.

Founded in 1992, the company specializes in providing network solutions for telecommunication and cloud computing firms. Its clients include the likes of AT&T (T), Microsoft, Google, Meta, and others.

Ciena has long been a leader in network solutions for leading tech firms across metro, regional, and long-haul networks. However, in recent years the company has solidified itself as a key pillar of the AI buildout.

Today, cyclical telecom providers account for less than half of the company’s revenue, with direct cloud providers like AI hyperscalers becoming a larger share of Ciena’s business.

Back in 2021, these customers accounted for just 22% of revenue. However as the AI revolution has gained steam, direct cloud producers have grown to make up 38% of sales in 2025.

Ciena has capitalized on the AI movement, and has been rewarded as a result. In just the past year the company’s stock has soared more than 350%. Following this ascension, some investors may be hard-pressed to say this company may still be undervalued.

However, Uniform accounting reveals this may be the case.

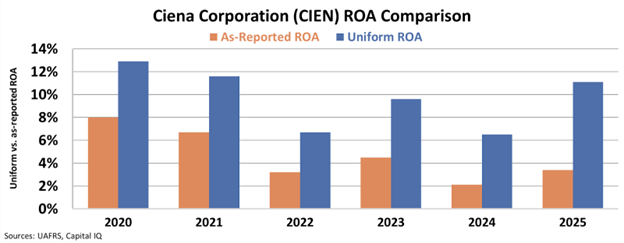

According to GAAP-accounting, Ciena’s as-reported return on assets (“ROA”) peaked at 8% in 2020. Returns collapsed to 3% in 2022 amid a weak semiconductor market and reduced investment following a strong cycle coming out of the pandemic.

Since then, the company’s as-reported returns have remained at 3% levels, suggesting that while the company is embracing new market tailwinds, they have not resulted in improved profitability. However, Uniform accounting offers a differing perspective. After delivering returns above 10% each year from 2019 to 2021, Ciena’s Uniform ROA fell in 2022 amid a cycle downturn, but fell only to 7%, which still exceeded the company’s cost of capital.

Today the company’s profitability has returned to 10%-plus levels as growing demand for AI products and a shift towards AI-related end markets has boosted returns.

Investors understand that Ciena is benefitting from increased optical networking spending as companies race to build out the foundation for AI models.

However, the market is still failing to recognize how these tailwinds have had a material impact on the company’s profitability. After booking a record $5 billion backlog in 2025, Ciena’s returns are primed to continue climbing.

As long as investors continue to misunderstand Ciena’s true profitability, additional upside may yet be warranted.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research