As the backbone for connectivity in the internet of things, this firm’s services have never been more valuable

This firm’s well-positioned business model has benefited from the large macroeconomic tailwinds occurring in the industry it operates in.

Additionally, the firm’s valuable services, which are an essential backbone to the internet of things, have allowed it to generate robust profitability levels.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Last Thursday, we highlighted how Broadcom (AVGO) is well positioned to benefit from the global rollout of 5G.

However, Broadcom is not the only company that has benefited from being well-positioned in the midst of large macroeconomic tailwinds.

Beyond just the trend known as the “internet of things” (IoT), the world is becoming more connected overall.

This connectivity promises huge benefits for users and corporations alike, but signals danger as well. The more we are all connected, the easier it is for a bad actor to find a backdoor into vulnerable data.

One of the largest digital attacks of all time was launched from a weakly defended security camera connected to the internet. From this vulnerability, hackers were able to temporarily take down sites like Spotify, Reddit, and even the U.K. official website.

Furthermore, with so much data consolidated on a few cloud services, the security used to protect the cloud and the world from cyber attacks needs to be top notch. As the world saw with the Equifax (EFX) breach, millions of people had their data leaked with so much information in one place.

As investors might expect, any company that is positioned well to help protect these two components that make up the backbone of connectivity would fetch a premium return.

One of these companies is NetScout Systems (NTCT). NetScout Systems integrates application and network performance management solutions safely.

In other words, NetScout Systems allows for complete functionality in the connection of the IoT.

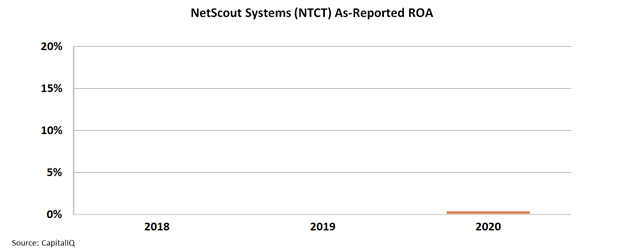

Despite these large secular tailwinds, coupled with the company being essential to the cloud and network security worlds, the firm seems to barely be making any money.

Specifically, on an as-reported basis, the firm’s ROA levels have stagnated below 1% levels.

The as-reported metrics portray the firm as barely able to make a dime.

In reality, this picture of the firm’s earnings power over the last three years is inaccurate. Historically, the firm has been quite profitable. Distortions in GAAP accounting around goodwill, amortization, and other line items have suppressed the firm’s profitability.

When looking through a Uniform Accounting lens, it becomes clear that the firm’s business model is better than it seems.

Specifically, NetScout Systems has been able to generate returns above 7% over the past three years, at 17% levels in 2018.

The distortions between as-reported and Uniform Accounting metrics for NetScout Systems may lead investors to miss the value the firm provides for security in cloud computing and the IoT.

Without Uniform Accounting, investors would never understand that the value NetScout is providing is worth enough to pay for.

SUMMARY and NetScout Systems, Inc. Tearsheet

As the Uniform Accounting tearsheet for NetScout Systems (NTCT:USA) highlights, the Uniform P/E trades at 37.3x, which is above the global corporate average of 25.2x, but around its own historical average of 36.4x.

High P/Es require high EPS growth to sustain them. That said, in the case of NetScout Systems, the company has recently shown a 41% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, NetScout Systems’ Wall Street analyst-driven forecast is a 25% EPS decline in 2021 followed by a 63% EPS growth in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify NetScout Systems’ $29 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 15% per year over the next three years. What Wall Street analysts expect for NetScout Systems’ earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power is around the long-run corporate average. Also, intrinsic credit risk is 260bps above the risk-free rate and cash flows and cash on hand are slightly above its total obligations—including debt maturities and capex maintenance. All in all, this signals a moderate credit risk.

To conclude, NetScout Systems’ Uniform earnings growth is in line with its peer averages while the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research