This company looks positioned to win the at-home revolution, but Uniform Accounting tells a different story

As the world starts to reopen, there will be winners and losers of what we are calling the at-home revolution. In fact, we even wrote a whole report on the companies we think will win.

This company has been positioning itself to win the “play at home” wave for decades, and at first glance looks like it might be ready to see profitability take off.

However, it doesn’t make our list of best stocks, and Uniform Accounting helps us explain why.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Even as the world starts to reopen, it is happening slowly. People are still spending far more time at home, and particularly for those who don’t know when their office will reopen, that isn’t going to change soon.

We’re calling this massive wave the at-home revolution. In fact, our individual investor arm, Altimetry, released a new report highlighting twelve stocks that are positioned well to benefit from this revolution. If you’re interested you can see more information here.

One of the key themes of this new wave isn’t just working from home though–it is entertaining at home. Playing at home.

Even before the coronavirus pandemic, esports had been a massively growing business. The number of video gamers worldwide has grown from ~1.8 billion in 2014 to over 2.5 billion currently. Esports viewership is projected to grow by 9% annually through 2023, doubling by then relative to 2017 numbers. The global esports market reached over $1 billion in 2019. For context, the revenue of the National Hockey League (NHL) was just $5 billion in 2019.

This is a fast-growing market, and it can be done from home, something the NHL, and other leagues don’t have. As more people are spending time at home, that will only lead to faster growth of this business.

One company that comes up a lot in the conversation of esports is Activision Blizzard (ATVI). Owner of one of the most popular current games, Overwatch, the company is right in the middle of this revolution. Even before that though, Blizzard owned StarCraft, another massive esport game that has been popular for over twenty years.

And it isn’t just going after a gaming niche.

Activision also acquired King Digital in 2016, going after the developer of Candy Crush, the game of choice for “social gaming” and Generation X in particular, with over 2.5 billion downloads to date.

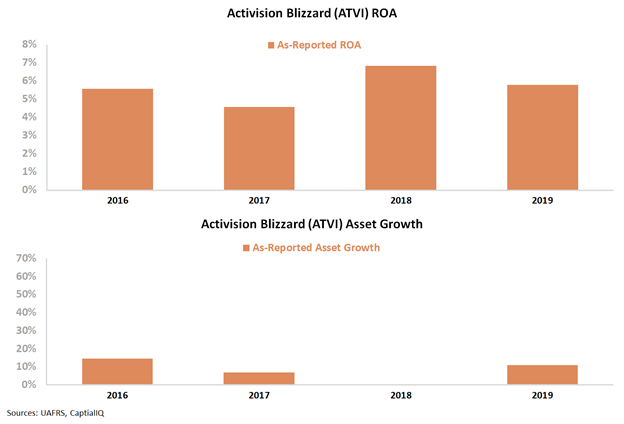

At first glance, the as-reported financials suggest that Activision Blizzard’s acquisition of King Digital wasn’t wise, as it led to Activision being a middling return business. But the company also has been able to maintain its stable return base since, showing at least the business is stable if not slightly improving.

It would appear that the firm has been able to continue to roll up companies in high-demand, building its position in the gaming space, just ahead of this massive wave. Investors may even think that with returns improving slightly in recent years, returns are trending higher, and Activision is about to reap the benefits of its investments.

However, Uniform ROA gives a different picture in two very important ways.

On one hand, the firm already has impressive returns. Since the King acquisition, Uniform ROA isn’t at weak 5%-7% levels, it has been comfortably above 30% each year. On the other hand, while it has been strong, it has also been declining.

This isn’t a company that has ramped investment ahead of good returns, this is a company that is seeing declining profitability as it invests.

Activision is continuing to grow the business, and investors may think this is a solid strategy as more and more are turning to playing at home. The data shows something different, Activision is investing in a lower return business. As long as it continues to do so, returns will continue to fall.

At current levels, the market is pricing in expectations for Activision to see returns grow, possibly because of optimism created by bad as-reported financials.

As it becomes clearer that the firm has actually seen returns compress, that could lead the market to adjust expectations lower.

Activision Blizzard, Inc. Embedded Expectations Analysis – Market expectations are for ROA to improve, and management may be concerned about revenue, margins, and player engagement

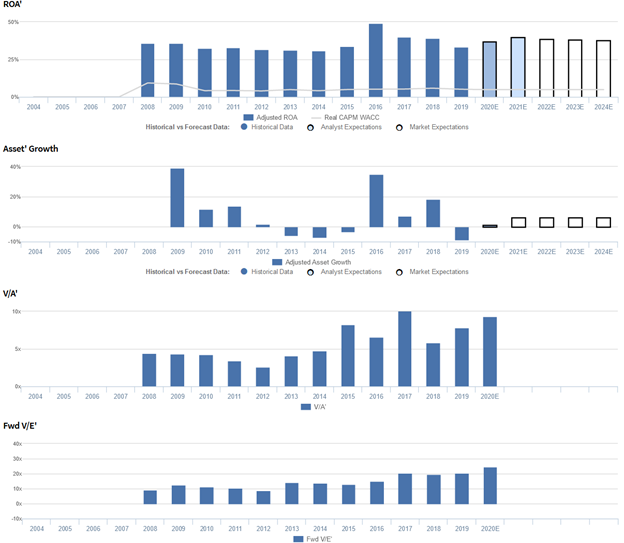

ATVI currently trades above corporate averages relative to Uniform Earnings, with a 24.0x Uniform P/E (Fwd V/E′). At these levels, the market is pricing in expectations for Uniform ROA to improve from 33% in 2019 to 37% in 2024, accompanied by 7% Uniform asset growth going forward.

Meanwhile, analysts have more bullish expectations, projecting Uniform ROA to expand to 40% in 2021, accompanied by 1% Uniform asset growth.

Historically, ATVI has seen robust profitability. From 2008 to 2014, Uniform ROA fell from 36% to 31%, before the firm’s acquisition of King Digital Entertainment spurred Uniform ROA to expand to a peak of 49% in 2016, as they began to expand their footprint into the mobile gaming space. Since then, however, Uniform ROA has compressed to 33% in 2019.

Meanwhile, Uniform asset growth has historically been volatile, positive in seven of the past eleven years, while ranging from -9% to 18%, excluding 39% growth in 2009 and 35% growth in 2016, largely due to their merger with Vivendi Games and acquisition of King Digital, respectively.

Performance Drivers – Sales, Margins, and Turns

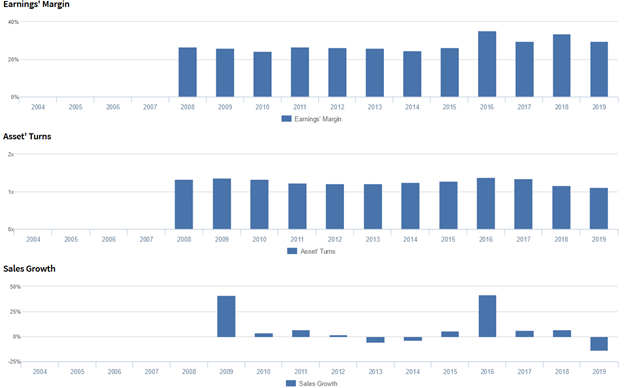

Recent trends in Uniform ROA have been driven by trends in both Uniform earnings margin and Uniform asset turns.

From 2008-2015, Uniform margins remained fairly stable at 24%-27% levels, before expanding to a high of 35% in 2016 and subsequently fading to 30% in 2019.

Similarly, Uniform turns compressed from 1.4x in 2009 to 1.2x levels in 2011-2013, before recovering to 1.4x in 2016 and fading to a low of 1.1x in 2019.

At current valuations, the market is pricing in expectations for Uniform margins to stabilize and a reversal of recent declines in Uniform turns.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2019 earnings call highlights that management is confident they see mobile as a way to attract players that they do not currently reach on PC, console, and others that may have never experienced their franchise before.

However, management may be concerned about their approach towards capital allocation and the sustainability of Call of Duty revenue growth.

In addition, management may lack confidence in their ability to sustain recent operating margin growth in their Blizzard portfolio and whether Hearthstone and Overwatch can drive engagement and player investment.

Furthermore, they may lack confidence in their ability to attract mobile payer engagement, and they may have concerns about the sustainability of revenue in their King portfolio.

Finally, they may also be concerned about the impact of their decision to remove the Season Pass, and they may be exaggerating their enthusiasm about their 2019 financial performance.

UAFRS VS As-Reported

Uniform Accounting metrics also highlight a significantly different fundamental picture for ATVI than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

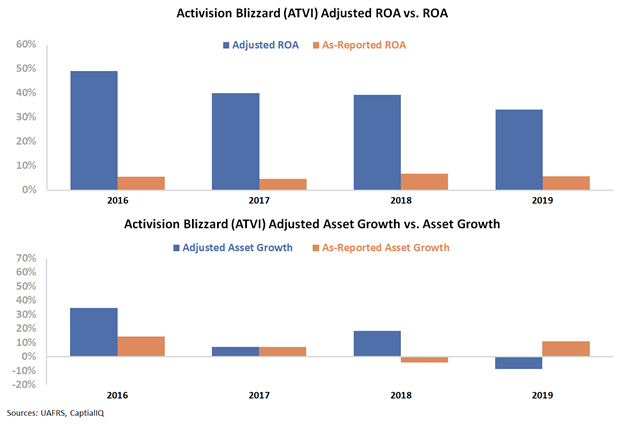

As-reported metrics significantly understate ATVI’s profitability. For example, as-reported ROA for ATVI was 6% in 2019, materially lower than Uniform ROA of 33%, making ATVI appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2016, as-reported ROA has maintained 5%-7% levels through 2019, while Uniform ROA has collapsed from 49% to 33% over the same timeframe, directionally distorting the market’s perception of the firm’s recent profitability trends.

SUMMARY and Activision Blizzard, Inc. Tearsheet

As the Uniform Accounting tearsheet for Activision Blizzard (ATVI) highlights, the Uniform P/E trades at 24.0x, which is above corporate average valuation levels and around its own recent history.

High P/Es require high EPS growth to sustain them. In the case of Activision Blizzard, the company has recently shown a 23% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Activision Blizzard’s Wall Street analyst-driven forecast is a 16% and 9% growth in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Activision Blizzard’s $72 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 4% each year over the next three years to justify current prices. What Wall Street analysts expect for Activision Blizzard’s earnings growth is above what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 6x the corporate average. Also, cash flows and cash on hand are nearly 5x higher than its total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals low credit and dividend risk.

To conclude, Activision Blizzard’s Uniform earnings growth is below peer averages in 2020. However, the company is trading in line with average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research