This defense company’s inventions fly under investors’ radar

The world is becoming a scarier place with geopolitical conflicts erupting in various regions.

To address these challenges, the United States recognizes the need to modernize its defense posture. Congress has approved increasing defense budgets, and the Biden administration is seeking over $830 billion for defense in 2024.

AeroVironment (AVAV), a company with a history of developing unmanned solutions, is strategically positioned to benefit from this shift.

If geopolitical tensions continue to drive defense spending, AeroVironment could see significant opportunities for growth and market leadership. However, the market underestimates their potential and contributions.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The number of geopolitical conflicts has surged worldwide in the last two years. In the face of an increasingly scarier world, policymakers in Washington recognize the need to transform America’s defense posture for the 21st century.

This requires significant modernization of U.S. forces. The Pentagon has made innovation in fields like autonomous systems, AI, hypersonics, and space-based capabilities top priorities as these emerging domains will shape future great power competition.

To support this defense renaissance, Congress has approved steadily increasing budgets, with negotiations underway to further boost spending on national security. The Biden administration is requesting over $830 billion for defense in 2024 (a 2% increase over 2023), a sign of the renewed commitment to American military primacy.

While giants of the industry will capture much of this funding, smaller innovators stand to benefit enormously from the Pentagon’s strategic focus on transformative technologies.

AeroVironment (AVAV) has positioned itself at the very forefront of these trends reshaping defense through its history of developing cutting-edge unmanned solutions.

For over 40 years, the company has supported American forces with intelligence-gathering drones like the Raven and Wasp, establishing itself as the pioneer in small unmanned aircraft system (“UAS”) technology. Its experience in this segment has provided valuable lessons that have since guided expansion into new domains.

Recognizing autonomous systems as increasingly vital to 21st-century warfare, AeroVironment has made strategic moves to capture more of the rising investment.

Through acquisitions of Tomahawk Robotics, Nauticus Robotics, and Arcturus UAV since 2021, it has integrated industry-leading capabilities in AI-enabled autonomy, advanced navigation, and connectivity between unmanned platforms.

These additions are directly aligned with the Pentagon’s priorities, allowing networked teams of drones and robots to multiply the effectiveness of troops on the ground and at sea.

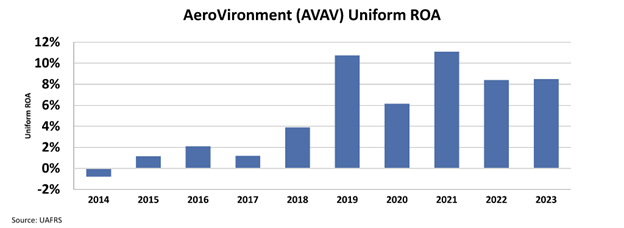

Also, these developments massively boosted the profitability and recovered business. The company’s Uniform return on assets (“ROA”) jumped from -1% in 2014 to nearly 9% in 2023.

Take a look…

With its expanded technological portfolio and reputation as one of the most experienced innovators in unmanned vehicles, AeroVironment is uniquely positioned to support the military modernization underway.

As greater budgets flow to autonomous solutions, the company is well-equipped to provide the transformative capabilities demanded by combatant commands.

While AeroVironment stands to capture outsized gains, the market is just expecting a slight increase in the company’s profitability.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to rise just around 12%, a far cry from the company’s true potential…

The market is severely underappreciating the company’s position in the coming years for defense investments.

If current geopolitical tensions continue driving increased defense spending focused on innovation, smaller companies at the forefront like AeroVironment stand to gain immense opportunities.

AeroVironment’s pioneering role in autonomous systems perfectly aligns with the strategic direction of both the Pentagon and the defense industry.

SUMMARY and AeroVironment, Inc. Tearsheet

As the Uniform Accounting tearsheet highlights, the Uniform P/E trades at 24.5x, which is above its global corporate average of 18.4x, but below its historical P/E of 27.8x.

High P/Es require high EPS growth to sustain them. In the case of AeroVironment, the company has recently shown an 11% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AeroVironment’s Wall Street analyst-driven forecast is a 60% and 7% EPS growth in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AeroVironment’s $135.56 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 14% annually over the next three years. What Wall Street analysts expect for AeroVironment’s earnings growth is in line with what the current stock market valuation requires through 2024.

Furthermore, the company’s earning power is 1x its long-run corporate average. Moreover, cash flows and cash on hand are 1.9x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 160bps above the risk-free rate.

All in all, this signals average credit risk.

Lastly, AeroVironment’s Uniform earnings growth is in line with its peer averages and its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research