AvalonBay is priced like the pandemic never existed

Some people are declaring the “At-Home Revolution” to have come and gone. Their evidence? Ballooning valuations for companies that should suffer in the face of it.

Let’s use one example to dispel this myth.

Also below, that company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

At this point in the pandemic, our calls around the “At-Home Revolution” have proven their value to our readers and subscribers through results. We, and other investing publications, have been talking about this theme for the better part of two years.

While the At-Home Revolution has touched every aspect of our lives, it started thanks to a de-emphasis on social gatherings and the emphasis on in-home activities. In general, this has meant an exodus from cities and a flight to the suburbs.

There, people can buy bigger homes with larger backyards to relax in, spacious personal offices to work in, and spare rooms to build home gyms in. Today however, the story has been so played out, pitching a stock idea on it would be bordering on trite.

Throughout the investing universe, just about every stock that was going to be impacted by this trend has already moved massively. We do believe that many could run even farther, as a number of the names on our flagship Conviction Long List were added on the At-Home Revolution theme, and still remain there.

The homeward shift isn’t over. Everything our analyst team is seeing points to it being a lasting shift in how people conceptualize their homes within the context of their lives.

But for At-Home Revolution companies to still be mispriced enough for us to recommend opening a new position, there also need to be other factors and catalysts at play. That’s because most of the pandemic-special tailwinds have already been priced-in.

That is why AvalonBay Communities (AVB) has caught our attention.

Avalon is a real estate investment trust (“REIT”) specializing in apartment buildings located in major American cities. The company boasts the efficacy of its internal research team which helps it identify markets poised for growth.

The buildings it buys then get rebranded as “Avalon communities,” and sold to upmarket renters.

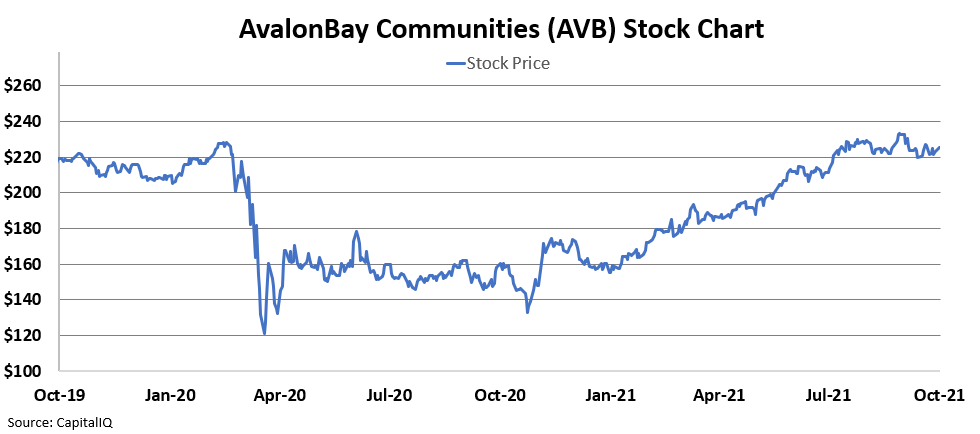

Apartment buildings and city-focused REITs were hit particularly hard during the pandemic. But as you can see below, Avalon’s stock has now returned to pre-pandemic levels. This is particularly puzzling given the waves of lease non-renewals, many of which lagged the pandemic significantly due to their annual renewal schedule.

It appears that the market is betting that AvalonBay owns such high-quality buildings, and has such sticky tenants, that the pandemic pressures should be of no concern.

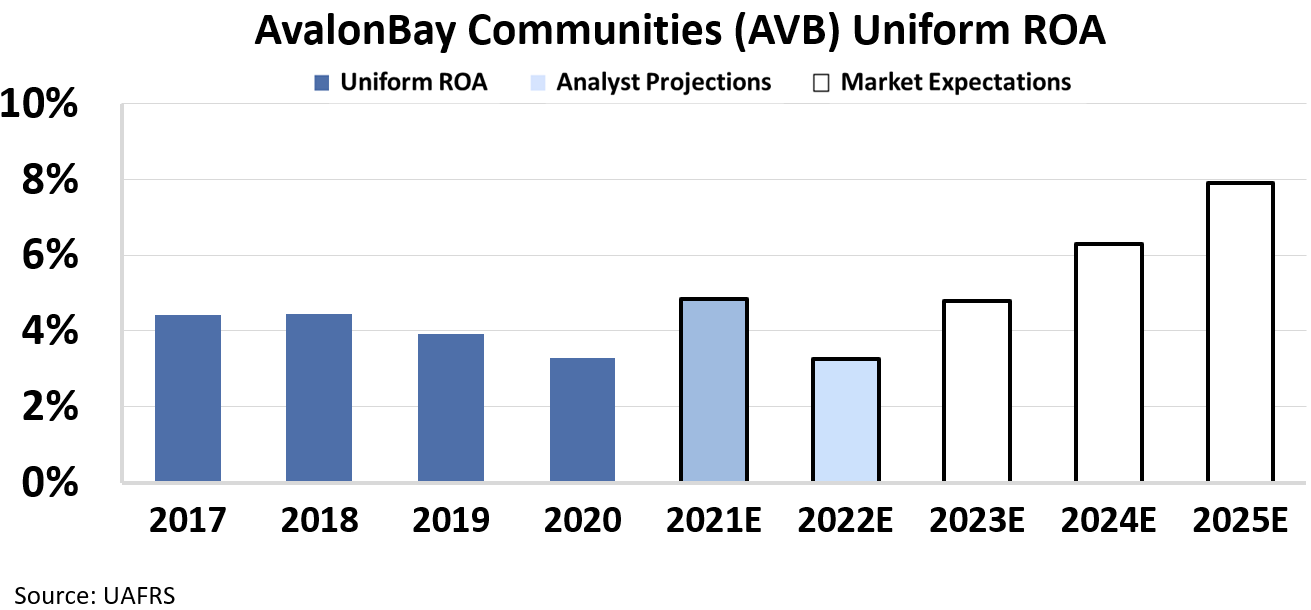

Uniform Accounting metrics show a different story. In reality, return on assets fell significantly from 4.5% in 2018 back to its previous all-time low, 3.3%, in 2020. While management touts their 96% occupancy rate, buildings have been giving large concessions to incentivize renters to move in, putting pressure on the top and bottom line.

Analysts are forecasting ROA to rebound in 2021 to all-time highs, a scenario that seems dubious. Then, analysts are projecting a fall back to 2020 profitability levels for 2022.

The current stock price implies a certain level of future productivity and growth than investors are pricing in. Rather than just saying a stock “looks too high” or “looks too low,” the above framework quantifies the future performance expected at today’s valuation for any stock we cover.

We call this framework the “Embedded Expectations Analysis,” and it is bedrock to our stock picking pipeline.

As the above chart highlighted, Embedded Expectations Analysis for Avalon Bay shows that for the company to be worth its current stock price, it needs its ROA to effectively double from its all-time-highs over the next five years, accompanied by a 7% Uniform asset growth.

The sharp disconnect between the company’s reasonable profitability range and the market-implied profitability sets its stock to come crashing down once those lofty expectations get missed.

While the At-Home Revolution may no longer be a standalone investible thesis, in the absence of other catalysts, it is important to look twice before declaring it is over.

Ballooning valuations for companies that should suffer from this theme is not evidence against its validity.

It is evidence that investors are missing the story.

To learn more about how you can get access to our Embedded Expectations Analysis for over 4,500 companies, along with other detailed Uniform Accounting data, click here.

SUMMARY and AvalonBay Communities, Inc. Tearsheet

As the Uniform Accounting tearsheet for AvalonBay Communities, Inc. (AVB:USA) highlights, the Uniform P/E trades at 50.5x, which is above the global corporate average of 24.3x and its historical P/E of 47.4x.

High P/Es require high EPS growth to sustain them. In the case of AvalonBay, the company has recently shown a 22% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AvalonBay’s Wall Street analyst-driven forecast is a 77% EPS growth in 2021, followed by a 42% EPS decline in 2022.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AvalonBay’s $222 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 25% annually over the next three years. What Wall Street analysts expect for AvalonBay’s earnings growth is above what the current stock market valuation requires in 2021, but below that requirement in 2022.

Furthermore, AvalonBay’s earning power in 2020 is below the long-run corporate average. Moreover, cash flows and cash on hand are below total obligations—including debt maturities and capex maintenance. All in all, this signals a high credit and dividend risk.

Lastly, the company’s Uniform earnings growth is above its peer averages. However, the company is trading below its average peer valuations.

Best Regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research