Sometimes, the best investments are the “roadies” instead of the “stars”

Investors love to put their money behind long-term macro trends that promise to transform our world. Just a few of these include 5G or the Internet of Things (IoT). And yet, many investors neglect the companies supplying these trends.

Using GAAP accounting, it appears today’s company has struggled to stay relevant, while Uniform Accounting tells a different story.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

News channels like CNBC and Bloomberg are always highlighting the next big markets for investors to be paying attention to. A few years ago, investing in cannabis companies was all the rage. Now, the news cycle is dominated by technology.

Outside of the transformation in spending around the home we call the “At-Home Revolution”, investor money is pouring into new technology trends. These include sectors involved in cloud computing, the move from 4G to 5G, the Internet of Things, and industrial automation, to name just a few.

Companies under these sectors are the “stars” of the investing world, with the spotlight on them. The names related to any one of these trends will see piqued interest, perhaps making them overbought. This is why in these types of exciting industries, we recommend stepping back to look at the “roadies.”

Roadies are the unsung heroes of the music world, setting up the lights and sounds for the stars to perform on. Similarly, the suppliers for these booming industries will be exposed to the same macro tailwinds, but may be cheaper.

There are only a handful of companies who support all of these industries. Broadcom (AVGO) provides the backbone to all of these industries with its semiconductor and technology infrastructure products.

An investor who looks into Broadcom would expect the company to see strong demand from supplying all of these industries. With over 23,000 patents, the company should be able to leverage these intellectual properties (IP) into pricing power and high returns.

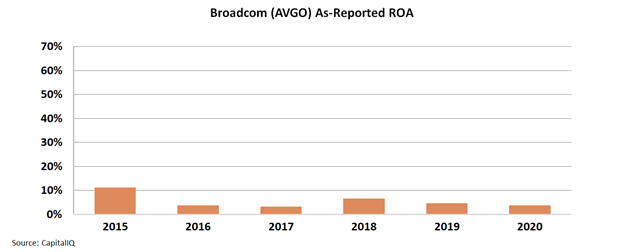

And yet, using GAAP accounting, it would appear Broadcom has been able to do nothing with its IP or marketing positioning.

Over the past six years, as-reported return on assets (ROA) has fallen below 10%, wallowing between corporate averages and cost-of-capital returns today.

However, this picture does not reflect the real earnings power of Broadcom. Distortions in GAAP accounting around goodwill, amortization, and other line items have suppressed the firm’s profitability.

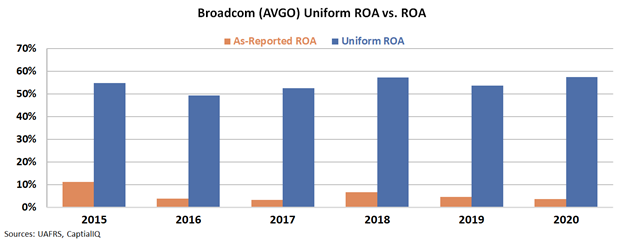

When looking through a Uniform Accounting lens, we can see the true earnings power of the firm.

Rather than returns below corporate averages, Broadcom has seen ROA trending above 50% every year since 2016. Supplying high-demand markets with strong pricing power has made the company a wildly successful “roadie.”

Investors without Uniform Accounting would be scratching their heads wondering why a company with cost-of-capital returns and $24 billion in revenue was worth $200 billion.

In reality, a company with a return of 57% in 2020 is worth a premium. Without using the right numbers, it’s impossible to find the diamonds in the rough before other investors.

By playing the roadie in the background, both investors and GAAP accounting metrics are missing the power of Broadcom.

SUMMARY and Broadcom Inc. Tearsheet

As the Uniform Accounting tearsheet for for Broadcom Inc. (AVGO:USA) highlights, the Uniform P/E trades at 21.2x, which is below the global corporate average of 25.2x, but below its own historical average of 16.6x.

Low P/Es require low EPS growth to sustain them. In the case of Broadcom, the company has recently shown a 7% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Broadcom’s Wall Street analyst-driven forecast is a 6% and 14% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Broadcom’s $450 stock price. These are often referred to as market embedded expectations.

Broadcom is currently being valued as if Uniform earnings would have little to no growth annually over the next three years. What Wall Street analysts expect for Broadcom’s earnings growth is above what the current stock market valuation requires in both 2021 and 2022.

Furthermore, the company’s earning power is 10x the long-run corporate average. However, intrinsic credit risk is 70bps above the risk-free rate and cash flows and cash on hand are below its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a high credit risk.

To conclude, Broadcom’s Uniform earnings growth is below its peer averages but the company is trading in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research