Six years ago, Uniform Accounting was consistently finding undervalued credits, this company is an example of markets growing more reasonably valued

When Valens started looking at bond-specific trades, rather than just credit for equity analysis, we found far more cheap bonds than expensive. However, the tides have turned and more often we are finding a more balanced mix of credit longs and shorts.

This company is the perfect example of a company that doesn’t look as positive, where fundamentals haven’t kept up with bond prices.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

After focusing mostly on equity ideas in Valens’ earlier years, in 2014, we began focusing on credit in earnest.

Prior to this, we had always spent time in our research looking at the credit profile of stocks we liked (or didn’t). Any good investor will say you need to understand the whole business to make informed decisions, and that includes understanding a company’s credit outlook.

However, we hadn’t spent the time to identify investable bonds from that research.

In what would eventually be the first step towards developing our Uniform Accounting Database, our team looked at model after model, cleaning up the accounting to find mispriced credit ideas.

Much like that report, most of the bonds we identified as mispriced were too cheap. If we said 50 companies had bonds that were trading at incorrect prices, chances were 45 of them would be undervalued.

This lined up pretty consistently with what our macro analysis was saying as well. Back then, we were looking at a lot of the macro signals we still look at today, and signals that are good for equity are generally good for credit because those signals are good for the whole business.

Credit was increasingly available for refinancing and investment, reducing risk of default.

Credit was increasingly cheap, so those companies that did refinance could do so at lower and lower prices.

Sentiment wasn’t stretched, as investors were still somewhat wary even several years after the Great Recession. We hadn’t reached “irrational exuberance” in equity markets or bond markets.

All of these supported our finding that corporate bonds, on average, were cheap. This gave us opportunities like the oil and gas bond basket.

With those recommendations we were able to help investors get equity-like returns in the bond markets, something that doesn’t happen often.

However, recently, this has started to shift. Instead of seeing only cheap bonds, we’ve started to see a better balance. Now there are still cheap bonds, but we’ve also come across a number where the market may be too bullish.

This also aligns well with our macro analysis that we’ve shared lately. As we’ve gotten later in the cycle, credit standards have continued to loosen. Credit pricing is cheap (in some places, cheaper than it has ever been), and investors have driven bond prices higher chasing yield.

In some cases, fundamentals for these companies have kept up, but in others, fundamentals haven’t. That is where we find bonds that are too expensive. American Axle & Manufacturing Holdings (AXL), is one of those companies.

The firm is expected to see a step down in profitability in the near-term, and although it should be able to service obligations for the next few years, it does raise the company’s risk profile.

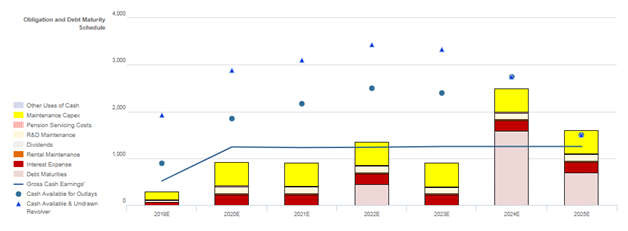

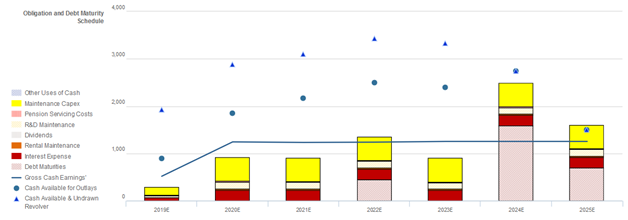

The chart above highlights the firm’s cash flows relative to obligations through 2025. Although it should have sufficient liquidity to service obligations until 2025, cash balances have declined, and the firm isn’t operating with a material buffer should things turn negative.

Additionally, after issuing several billion dollars of debt to acquire Metaldyne in 2017, American Axle’s recovery rate on unsecured debt fell significantly. At these levels, the firm may struggle to access credit markets to refinance obligations if it needs to do so.

These issues don’t point to a company facing imminent bankruptcy, but they do suggest a slightly risky name. This is particularly true for a sub-$1bn market capitalization name that does not have a material equity base to fall back on to raise capital.

As a result, current yields appear too tight and bond downside for the name might be warranted.

Credit Markets Continue to Understate AXL’s Consistent Material Debt Maturities; Wider Spreads Warranted

CDS markets are materially understating AXL’s credit risk, with a CDS of 279bps relative to an Intrinsic CDS of 437bps, while cash bond markets are understating credit risk with a cash bond YTW of 4.912% relative to an Intrinsic YTW of 6.112%.

However, Moody’s is overstating AXL’s fundamental credit risk, with their B1 rating four notches lower than Valens’ XO (Baa3) rating.

Fundamental analysis highlights that AXL’s cash flows should exceed operating obligations in each year going forward. However, the firm’s combined cash flows and expected cash build would fall short of servicing all obligations including debt maturities in 2025, as they face material debt headwalls of $1.6bn in 2024 and $700mn in 2025.

Despite this, the firm’s capex flexibility should allow them to service obligations, which is important, as the firm’s lackluster 40% recovery rate and limited market capitalization may inhibit their ability to access credit markets to refinance.

Incentives Dictate Behavior™ analysis highlights AXL’s compensation framework holds positive signals for credit holders, as it focuses management on all three value drivers: growth, margins, and asset turnover.

This should facilitate Uniform return on assets expansion and lead to increased cash flows available for servicing debt obligations.

Additionally, management members are not well compensated in a change-in-control, implying they are not incentivized to pursue a sale or accept a buyout of the firm, limiting event risk for creditors.

However, management members are not material holders of the firm’s equity relative to their annual compensation, indicating that they may not be well-aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (11/1) highlights that management may be concerned about continued EPS headwinds, the strength of their value proposition, and the throughput of their supply chain.

Material debt headwalls and a limited market capitalization suggest that credit markets are understating AXL’s underlying credit risk, while their operational sustainability and capex flexibility indicate that Moody’s is overstating their fundamental credit risk.

As such, a widening of credit spreads and a ratings improvement are both likely going forward.

SUMMARY and American Axle & Manufacturing Holdings, Inc. Tearsheet

As the Uniform Accounting tearsheet for American Axle & Manufacturing Holdings, Inc. (AXL) highlights the company’s Uniform P/E trades at 11.3x, which is below global corporate average valuation levels and its historical averages.

Low P/E’s require low—or even negative—EPS growth to sustain them. In the case of American Axle, the company has recently seen its Uniform EPS to decline by 67%, which may be a signal that below-average valuations are justified.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, American Axle’s Wall Street analyst-driven EPS growth forecast goes from a 52% in 2020 before inflecting negatively to -17% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $5 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for American Axle, the company would have to have Uniform earnings shrink by 7% each year over the next three years.

Considering a weak year this year, Wall Street analysts’ expectations for American Axle’s earnings growth are far below what the current stock market valuation requires.

American Axle’s Uniform P/E and Uniform EPS growth are both below peer averages.

Meanwhile, the company’s earnings power 1x corporate averages. Furthermore, total obligations, including debt maturities, maintenance capex, and dividends, are above total cash flows, signaling a high risk to its dividend or operations.

To summarize, American Axle is an above average profitability company with significantly low earnings growth potential and muted embedded expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research