This unlikely company is benefiting from semiconductor shortages, but the market may already know

With the surge in demand for used cars, this replacement car parts business has never been positioned better. The firm is benefiting from significant industry tailwinds, and it still looks cheap on an as-reported basis.

However, when looking through a Uniform Accounting lens, it becomes clear the surge in demand for used cars has not gone unnoticed by investors.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

As more individuals move out of cities and into suburbs, they are beginning to embrace the freedom and availability to leave their homes.

Whether it is to simply get fresh air or even go on a vacation, people have been overwhelmingly looking to buy new and used cars.

Cars have been a more favorable mode of transportation since the onset of the pandemic as public transportation and air travel do not allow for healthy social distancing.

As mentioned, individuals are still wanting to travel and escape quarantine at moments, pushing the demand even higher for cars. Furthermore, with semiconductor shortages impacting cars too, manufacturers are unable to fulfill demand.

It also makes more sense for many first-time car owners to purchase used cars instead of new. Most of the time, used cars are abundant and more affordable than new models.

Car buyers should factor in maintenance when making their decision, because used cars will often require maintenance sooner.

With the surge of used cars back on the roads, we can expect a major uptick in maintenance requests over the coming years.

While this is a complex confluence of market factors, together it means good things are to come for those who sell replacement car parts over the next couple of years.

AutoZone (AZO) is the example beneficiary of this booming used car market. AutoZone operates in the retail and distribution of automotive replacement parts and accessories for cars.

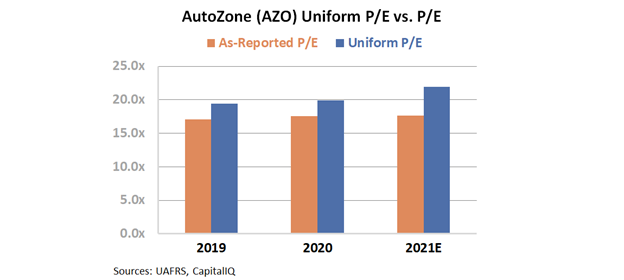

With the surge in used car demand creating various opportunities for AutoZone, the company’s valuations appear to be interesting using as-reported metrics.

In fact, the company is currently trading at a deep discount relative to the market. Specifically, AutoZone is trading at an as-reported 18.0x price to earnings ratio (P/E).

See for yourself below.

In reality, this is not an accurate picture of AutoZone’s valuation.

The company is not trading as cheaply as it seems. The firm is really trading at a 22.0x P/E multiple, right in line with market averages.

When looking through a Uniform Accounting lens, it becomes clear the surge in demand for used cars has not gone unnoticed.

While investors may be dejected that AutoZone’s upside is already priced in, it is more reasonable given the immense tailwinds behind the surge in demand for used cars.

It appears that the market is actually aware of the reality in these trends and in the potential of continued consumer buying habits.

SUMMARY and AutoZone, Inc. Tearsheet

As the Uniform Accounting tearsheet for AutoZone, Inc. (AZO:USA) highlights, the Uniform P/E trades at 21.9x, which is below the global corporate average of 25.2x but above its own historical average of 19.7x.

Moderate P/Es require moderate EPS growth to sustain them. That said, in the case of AutoZone, the company has recently shown a 22% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, AutoZone’s Wall Street analyst-driven forecast is a 4% and 2% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify AutoZone’s $1,419 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 2% per year over the next three years. What Wall Street analysts expect for AutoZone’s earnings growth is above what the current stock market valuation requires in 2021 and in line with its requirement in 2022.

Furthermore, the company’s earning power is 4x the long-run corporate average. Also, intrinsic credit risk is 60bps above the risk-free rate and cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. All in all, this signals a low credit risk.

To conclude, AutoZone Uniform earnings growth is below its peer averages, but the company is trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research