Uniform Accounting reveals how much the U.S. government is willing to pay for cyber defense

The threat of cyber attacks has spiked in recent years. While it’s overall a threat and a concern, it does create demand for increased cybersecurity infrastructure. Today’s firm is part of that movement.

Looking at as-reported numbers might make investors think digital security is a thankless, profitless job. Digging deeper, we can see the firm has stronger profitability than the market thinks.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

Ever since President Trump assumed office, there has been a fierce political debate regarding the efficacy of his policies and strategies.

One hot topic has been President Trump and Senate majority leader McConnell’s efforts to confirm more than 200 judges across the country. Trump’s tax cuts, his response to the coronavirus pandemic, and policies regarding immigration have also caused debate.

Despite all the disagreement, there is one issue both sides appear to agree on: President Trump took on a more confrontational stance with China in his trade war. Although the method may have been controversial, both sides of the aisle are worried about the threat China poses.

The Biden administration is unlikely to significantly reverse its pursuit of a new economic ‘Cold War’ with China. Biden’s choice for Secretary of State, Antony Blinken, outright called China a competitor. The situation appears to be much like the U.S.’s relationship with the former USSR. The battlefield includes not just geopolitics, but one of the fastest-growing issues facing America: cyberwarfare.

This issue has become more prominent in recent years. In just the past five years, China has sought to gain access to U.S. infrastructure and intellectual property and Russia has attempted to destabilize the election process.

One of the companies working on the front lines of this cyberwarfare is Booz Allen Hamilton (BAH). Booz Allen is a management and information technology (IT) consulting firm.

Over 95% of Booz Allen’s revenue comes from the US government and 66% of its staff holds some type of security clearance. The firm won over $4 billion in US Federal obligations in 2020 alone. The company provides IT cybersecurity services to many different branches of the federal government, including the Department of Defense.

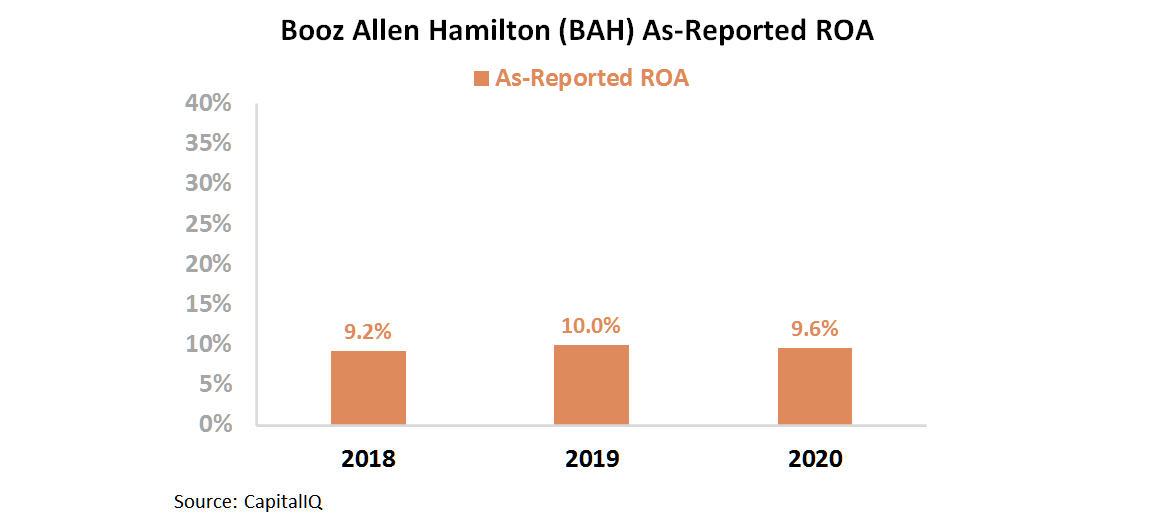

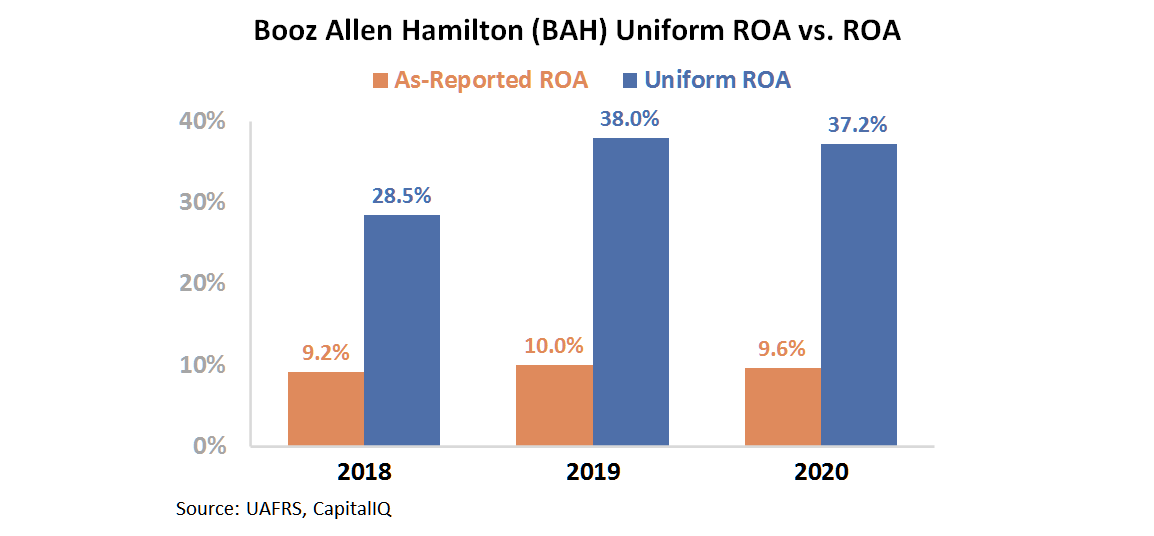

Booz Allen Hamilton plays a vital role in trying to keep the country’s secrets safe from enemies abroad. With such an important role, one might assume the government pays top dollar to ensure success. However, Booz Allen has had a stagnant, average-at-best as-reported ROA in recent years. Between 2018 and 2020, it ranged between 9% and 10%, slightly below corporate averages.

This is not an accurate depiction of the firm’s profitability. GAAP’s treatment of interest expense, among other distortions, is suppressing the firm’s earnings.

By using Uniform Accounting, we can see how the economics actually work for Booz Allen Hamilton’s contracts. The firm has been able to improve its win rate on both recompetes and new business in recent years, allowing it to expand its profitability.

Despite as-reported metrics implying Booz Allen Hamilton has stagnant profitability, Uniform Accounting highlights that Uniform ROA has improved from 29% in 2018 to 37% in 2020.

Uniform Accounting is able to show how successful Booz Allen Hamilton has been. It operates in one of the most important sectors for national security. As such, the government pays the firm considerably for its services.

Cyber threats are an unfortunate constant in the world of modern technology and politics. As such, it’s likely Booz Allen Hamilton will be able to sustain its momentum going forward.

SUMMARY and Booz Allen Hamilton Holding Corporation Tearsheet

As the Uniform Accounting tearsheet for Booz Allen Hamilton Holding Corporation (BAH:USA) highlights, the Uniform P/E trades at 19.6x, which is below the global corporate average valuation levels but above its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Booz Allen Hamilton, the company has recently shown a 21% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Booz Allen Hamilton’s Wall Street analyst-driven forecast is a 1% EPS shrinkage in 2020 and an 11% EPS growth in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Booz Allen Hamilton’s $88 stock price. These are often referred to as market embedded expectations.

The company can have a minimal Uniform earnings growth each year over the next three years and still justify current stock prices. What Wall Street analysts expect for Booz Allen Hamilton’s earnings growth is below what the current stock market valuation requires in 2020, but above this requirement in 2021.

Furthermore, the company’s earning power is 6x the long-run corporate averages. Additionally, cash flows and cash on hand are well above its total obligations—including debt maturities, capex maintenance, and dividends. Altogether, these signals a low credit and dividend risk.

To conclude, Booz Allen Hamilton’s Uniform earnings growth is slightly below its peer averages, but the company is trading above its peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research