This company will help build the digital backbone of America

The Bipartisan Infrastructure Bill allocates $1.2 trillion to infrastructure projects, including a significant investment in broadband infrastructure to address the digital divide, especially in underserved and rural areas.

This investment is expected to boost demand for connectivity products, benefitting companies like Belden (BDC), a leading provider of connectivity solutions.

Belden’s diverse product portfolio positions it well to capitalize on this increased demand.

Despite these tailwinds, market skepticism remains, influenced by doubts about the sustainability of the demand generated by the bill.

Also below, is the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

The Bipartisan Infrastructure Bill passed in 2021, allocates a whopping $1.2 trillion in infrastructure projects.

The bill is expected to fund a wide range of projects, including transportation, water systems, and energy infrastructure.

Furthermore, a significant portion of this budget is expected to be allocated towards ensuring that every American has access to reliable high-speed internet.

This investment in broadband infrastructure is critical, as it will help bridge the digital divide and ensure that all Americans have access to the opportunities and resources that come with reliable internet access.

The funding will be used to expand broadband infrastructure in underserved and rural areas, as well as to improve existing infrastructure in urban areas.

As a result of this investment, there is to be a significant increase in demand for products such as cabling, routers, switches, and gateways. These products are essential for building and maintaining high-speed internet infrastructure, and Belden (BDC) is well-positioned to benefit from this increased demand.

Belden is a leading provider of connectivity and networking solutions for industrial automation, enterprise, and broadcast markets. The company offers a wide range of products for network infrastructure and connectivity across various applications.

With a product portfolio that encompasses everything from cabling and connectivity systems to routers and optical fiber cables, Belden’s offerings are crucial to the build-out of internet infrastructure.

The company’s products are known for their reliability, durability, and high performance. Furthermore, these products are also designed to be easy to install and maintain, which makes them an attractive option for customers looking to upgrade their existing infrastructure.

Belden’s products are essential components of the broadband infrastructure that will be built to expand access to high-speed internet. As demand for these products increases, Belden is likely to see a surge in sales and profits.

We can already see the effects of the infrastructure bill in play…

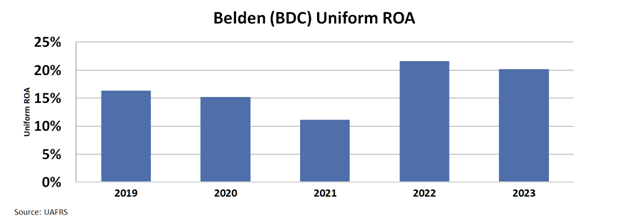

While struggling during the pandemic, Belden managed to recover its Uniform return of assets (“ROA”) in 2022 with 22%.

After the bill passed, the company has seen increased sales and profitability in 2022 and 2023.

As the bill’s provisions begin to materialize, Belden will continue to capitalize on the ensuing opportunities. The company’s robust portfolio of connectivity solutions and its established presence in the market place it at the forefront of what promises to be a period of growth and expansion in the broadband infrastructure.

Despite these promising tailwinds, there seems to be a cloud of pessimism hanging over the company in the market.

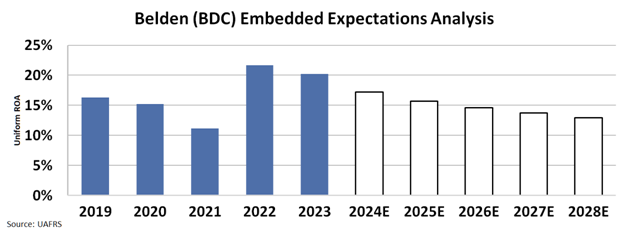

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s ROA to fall to 13%, similar to the pandemic levels.

The market’s pessimistic view is caused by the demand coming from the bill not being sustainable…

As governments and private entities alike gear up to upgrade and expand the nation’s internet infrastructure, Belden’s products and solutions are likely to see continuous demand.

For Belden, this period represents a unique opportunity for growth and expansion. As the company ramps up production to meet the anticipated demand, it will also be contributing to a national effort to enhance connectivity and technological accessibility.

Thanks to this continued high demand, the stock has a big upside potential.

SUMMARY and Belden Inc. Tearsheet

As the Uniform Accounting tearsheet Belden Inc (BDC:USA) highlights, the Uniform P/E trades at 15.3x, which is below its global corporate average of 22.4x and its historical P/E of 13.0x.

Low P/Es require low EPS growth to sustain them. In the case of Belden, the company has recently shown a 26% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Belden’s Wall Street analyst-driven forecast is a 8% and 10% EPS shrinkage in 2023 and 2024, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Belden’s $84.97 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to shrink 8% annually over the next three years. What Wall Street analysts expect for Belden’s earnings growth is in line with what the current stock market valuation requires in 2023 but above its 2024 requirement.

Furthermore, the company’s earning power is 3x its long-run corporate average. Moreover, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Also, the company’s intrinsic credit risk is 200bps above the risk-free rate.

All in all, this signals low dividend risk.

Lastly, Belden’s Uniform earnings growth is above its peer averages but in line with its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research