This beer maker can reap the benefits of tariffs

Trump’s tariff announcement significantly shook markets, causing major indices to drop sharply due to fears of reduced corporate profits.

Amid recession concerns, Molson Coors (TAP) is gaining attention as a defensive investment, benefiting from its mostly domestic production and potential tariff-driven advantages against imported beer competitors.

After successfully managing down high debt levels from a 2016 acquisition, Molson Coors now has a healthier balance sheet, yet market skepticism persists, expecting lower returns.

Despite challenges from shifting consumer tastes and stagnant margins, the market might be underestimating the company’s opportunity to capture additional market share from tariffs on imports.

Investor Essentials Daily:

Thursday News-based Update

Powered by Valens Research

When President Trump unveiled his extensive tariff plan, markets responded with immediate concern.

The S&P 500 fell by 4.8%, the Dow Jones Industrial Average dropped by 4%, and the Nasdaq plummeted by 6% in a single trading day.

Investors moved quickly to shed stocks with international exposure as they feared potential damage to corporate profits across industries.

As recession fears grip the market, stable companies are stepping into the spotlight as defensive plays, with Molson Coors (TAP) emerging as a particularly compelling opportunity.

The company, which owns well-known brands including Coors, Miller, Blue Moon, and others, has positioned itself primarily as a domestic producer with over two-thirds of its sales generated in the United States.

With potential tariffs looming that could increase prices on imported beer brands, Molson Coors may be uniquely positioned to capitalize on a market shift.

As a primarily U.S.-based producer brewing the majority of its products domestically, the company could see an opportunity to build market share as imported competitors face higher costs that must be passed on to consumers.

Currently, Molson Coors holds approximately 24% of the U.S. beer market, positioning it as the second-largest beer company in the country behind Anheuser-Busch.

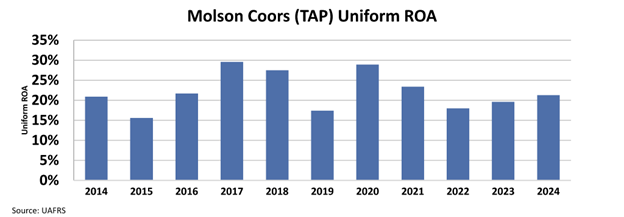

Over the years, the company has consistently achieved solid returns, maintaining around a 20% Uniform return on assets ”ROA”.

An essential part of the company’s recent story is the significant debt management initiative undertaken following its $12 billion acquisition of SABMiller’s assets in 2016.

This acquisition greatly expanded Molson Coors’ portfolio but came at the cost of a substantial debt increase of around $9.2 billion, pushing leverage ratios to concerning levels at the time.

Over the past several years, management has strategically reduced this debt burden. This has lowered the company’s debt-to-EBITDA ratio from an alarming high of nearly 5x in 2016 down to a more manageable level of about 2.1x today.

This reduction in debt should ideally provide Molson Coors with increased flexibility, allowing more cash to be returned to shareholders through dividends and share buybacks.

Despite these positive developments, the market still has concerns about the company.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform ROA to decline to 13% from 21% last year.

Molson Coors’ margin growth has been relatively stagnant in recent years, impacted by high input costs and limited ability to pass those costs onto consumers without hurting sales volumes.

Consumer preferences have increasingly shifted towards lower-priced or non-alcoholic beverages, limiting the company’s ability to raise prices significantly.

This challenge, combined with ongoing declines in beer consumption per capita, paints a cautious outlook for revenue growth.

Yet, the potential tailwind provided by tariffs offers a genuine opportunity.

If imported beer prices rise notably, the company could leverage its domestic presence to gain market share.

This scenario is something the broader market appears to be overlooking.

Molson Coors’ successful deleveraging efforts have strengthened the balance sheet, and the potential tariff advantage could drive market share gains, offering substantial upside.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research