This beverage company can hold up during downturns

Beverages hold up well in downturns because people still need affordable daily staples, often trading down and drinking more at home.

Keurig Dr Pepper’s (KDP) diverse portfolio drove 5% revenue growth and 14% profit growth last quarter, led by a strong refreshment-drinks business even as coffee appliance volumes dipped.

Its investment in Ghost gives it higher-margin energy and functional drinks that can boost overall profitability as coffee costs ease in late 2025.

Trading at below corporate averages, Keurig Dr Pepper looks set for mid-single-digit revenue growth and margin improvement once input‐cost headwinds fade.

Investor Essentials Daily:

Tuesday News-based Update

Powered by Valens Research

During economic downturns, the beverage industry often serves as a safe harbor due to the consistent nature of its products.

Unlike luxury goods or travel, beverages are staples. While people’s financial situations may change, their need for refreshment and daily rituals remains, providing a stable floor for demand.

What does shift, however, is consumer behavior. In a weaker economy, customers don’t necessarily stop buying drinks but they change their habits.

Many will trade down from premium products to more affordable brands. They also tend to drink more at home, as it is significantly cheaper than buying drinks at a bar or restaurant. This predictability allows larger, established beverage companies to thrive in downturns.

By focusing on at-home consumption, value-oriented pricing, and leveraging strong brand loyalty, they can navigate economic turbulence more effectively than businesses in other, more discretionary sectors.

Keurig Dr Pepper (KDP) effectively manages a broad collection of beverage brands, ranging from its Keurig single-serve coffee systems to its popular Dr Pepper soft drinks, catering to a wide array of consumer tastes.

The company’s mix gives it steady cash flow even when one segment slows. In the latest quarter, Keurig Dr Pepper posted 5% revenue growth and expanded net profit by 14%, driven largely by an 11% jump in its refreshment beverages business.

Energy drinks and carbonated soft drinks carried the quarter, while coffee appliance and pod volumes dipped amid inventory adjustments and higher prices taken to offset green-bean inflation.

Furthermore, Keurig Dr Pepper is pushing into higher-margin categories. Its early 2025 investment in a majority stake in Ghost gives the company a foothold in fast-growing energy and functional drinks.

Ghost’s lifestyle and energy brand blends easily with the company’s distribution network, adding products that carry healthier or performance-oriented positioning.

Because those drinks command better margins than coffee and soda, their growth could lift overall profitability, concealing any lingering coffee weakness.

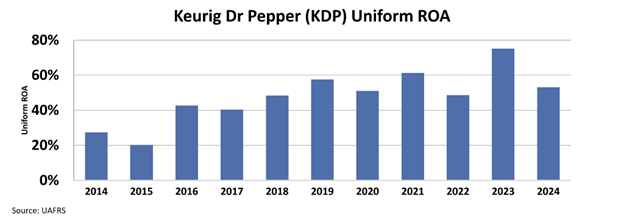

These factors and the steady nature of its business enabled the company to achieve 53% Uniform return on assets ”ROA” and 30% asset growth last year.

Despite demonstrating strong performance, Keurig Dr Pepper’s stock trades at below corporate average with a 19x Uniform P/E ratio.

This valuation suggests the market is concerned with the impact of rising input costs, especially new U.S. coffee tariffs and short-term swings in commodity prices.

We can see what the market thinks through our Embedded Expectations Analysis (“EEA”) framework.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform ROA to decline to around 46% from 53% last year.

In reality, management has already raised prices to protect margins, and coffee futures have started to retreat as Brazil’s harvest ramps up.

If coffee costs ease as expected by late 2025, promotions and steady pricing could help that segment recover.

Furthermore, Keurig Dr Pepper trades below its non-alcoholic beverage peers. At 19x forward P/E versus a 22x peer average, the stock still carries a 2.8% dividend yield, compared with peers closer to 1.5%.

However, risks remain. New coffee tariffs create supply-chain uncertainty, and any further cost shocks would test the company’s pricing power. Currency swings and a tough U.S. retail environment could also temper international growth.

Still, management’s history of cost control, its diversified portfolio, and its track record of steady dividend growth give the company a buffer against shocks.

At today’s levels, Keurig Dr Pepper looks positioned for mid-single-digit revenue gains and ongoing margin improvement.

That outlook, combined with its 2.8% yield, suggests investors who look past near-term cost noise can earn a solid return.

As coffee prices normalize and functional beverages take off, the market should give Keurig Dr Pepper credit with a higher multiple, unlocking upside for shareholders.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research