The market has prematurely tossed away this well-established pharma company

Investing in biotech companies is tricky due to the complex nature of the drugs and exclusivity rights. Companies bringing new products to market will often get a set period of time before generic alternatives can replicate the drug and enter the markets.

Today’s firm is dealing with a loss of exclusivity on its breadwinning drug. The market thus has incredibly low expectations for the firm, which may be undervaluing the company.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

We often talk to clients about how there are two main parts needed to understand why Uniform Accounting is important.

The first is understanding just how wrong as-reported metrics are. They give you an incomplete picture of what a company’s actual profitability is.

It also prevents investors from measuring or identifying a firm’s competitive advantage, or to see where earnings trends are going. An investor might see a company with declining returns and assume it has no competitive advantage. In reality the firm may have a sustainable moat and is actually increasing returns.

Additionally, you need to understand how Uniform Accounting helps solve the problems present with as-reported accounting

Biogen (BIIB) can help illustrate the point. Biogen is a multinational biotechnology company based in Cambridge, Massachusetts. The firm specializes in the discovery and development of therapies for neurological diseases.

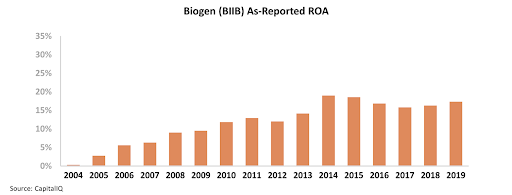

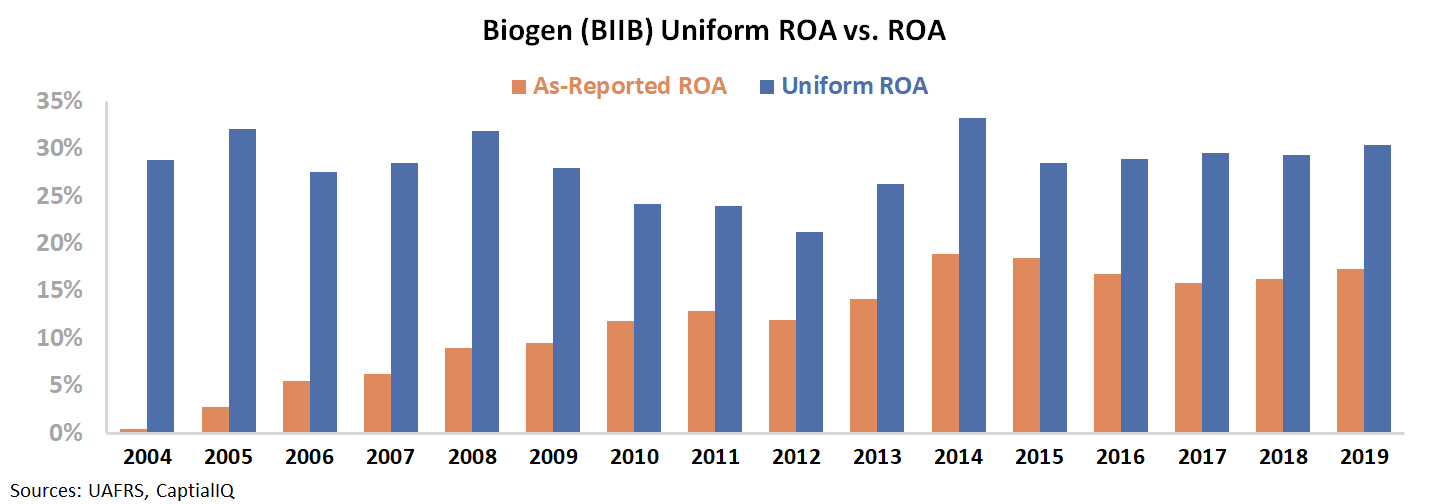

Looking at the firm under the lens of as-reported accounting might lead investors to draw the wrong conclusions. As-reported metrics do get the earnings trend right, showing stable returns the past four years.

However, due to distortions in as-reported accounting, as-reported ROA is understated. The firm appears to have had a 17% ROA in 2019, indicating solid but not groundbreaking returns.

However, once we look at the name under the Uniform Accounting framework, we can see the true extent of returns. Biogen actually had a 30% Uniform ROA in 2019, highlighting the strength of the firm’s economic moat.

Biogen has been able to differentiate itself in the biotech industry with its blockbuster Tecfidera drug used to treat Multiple Sclerosis.

The second component to Uniform Accounting is understanding what the market’s expectations are for the company in the future. Essentially, we’re looking at what Uniform ROA has to be to justify the current valuations for the company.

If an investor believes a company can beat these expectations, the stock is cheap. For Biogen these embedded expectations paint a powerful picture. Biogen has consistently had a Uniform ROA above 20% over the past 15 years thanks to the firm’s innovation and powerful offerings.

Despite this, the market is pricing in returns to fall to just 7%. This is well below any past year in the company’s history.

One of the main reasons for this potential drop is the loss of exclusivity for Biogen’s Tecfidera drug. Tecfidera brings in almost $4 billion in revenue for Biogen and is the firm’s largest money maker. However, courts have paved the way for generic alternatives to enter the market in 2021.

This means a huge potential hit to revenue and returns for Biogen. A silver lining however, is the firm can reduce its costs and reinvest its R&D spend elsewhere.

Without Uniform Accounting investors would miss the strong returns and low expectations of this biotech company. They might see Biogen as a firm with average returns, rather than robust profitability.

The market expects returns to crater for Biogen over the next few years to historic lows due to loss of exclusivity. However, the firm has proven its ability to innovate in the past, and may be undervalued if the firm can beat already low market expectations.

SUMMARY and Biogen Inc. Tearsheet

As the Uniform Accounting tearsheet for Biogen Inc. (BIIB:USA) highlights, the Uniform P/E trades at 10.6x, which is below the global corporate average valuation levels but around its historical average valuations.

Low P/Es require low EPS growth to sustain them. In the case of Biogen, the company has recently shown a 21% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that provide very poor guidance or insight in general. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Biogen’s Wall Street analyst-driven forecast is a 15% EPS shrinkage in 2020 and a 27% EPS shrinkage in 2021.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Biogen’s $249 stock price. These are often referred to as market embedded expectations.

The company can have a 22% Uniform earnings shrinkage each year over the next three years and still justify current stock prices.

What Wall Street analysts expect for Biogen’s earnings growth is below what the current stock market valuation requires in 2020, but above its requirement in 2021.

Furthermore, the company’s earning power is 5x the long-run corporate averages. Additionally, cash flows and cash on hand are 2x its total obligations—including debt maturities, capex maintenance, and dividends. Altogether, these signals a low credit and dividend risk.

To conclude, Biogen’s Uniform earnings growth is slightly above its peer averages, but the company is trading below its peer average valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Researchz