Bill Miller still knows how to pick great stocks

Many investors follow traditional strategies when creating their portfolios. Some “value” investors focus on undervalued companies, while others focus on companies with massive growth trajectories.

Some investors reject the traditional labels, and they simply invest in companies they believe can exceed the market’s embedded expectations. Bill Miller, who gained fame for his performance at Legg Mason, takes the more nuanced approach with his Miller Opportunity Trust Fund.

In addition to examining his current portfolio, we are including a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

Last year, we discussed Bill Miller’s impressive track record as a fund manager. We highlighted the performance of Legg Mason in an article that can be found here.

After generating successful performance in the Legg Mason Value Trust, Bill Miller started his own company. Today, we will highlight Miller Value Partners. More specifically, Miller Opportunity Trust.

While we highlighted Legg Mason back in August, it’s worth seeing how Bill Miller has applied his successful history into a brand new fund.

It takes significant strength to be humble when you are the only institutional investor known to have beaten the S&P 500 15 years consecutively. And yet, that is what makes Bill Miller who he is.

He calls the results of his streak “probably 95% luck.” He also mentions that it was more “an accident of the calendar.” If the reporting year ended on a different month, the streak would have ended long before 15 years.

The reality though is his fund’s success was not because of luck. It was because of a sound strategy based on the root of something great investors understand that the average investor doesn’t.

Miller has said “the first duty of the investor or analyst is to figure out what is embedded in the price, what is discounted…the failure to address that question is the main source of the poor relative results of most money managers.”

Fundamentally, you need to understand what the market is expecting a company to do, also known as “embedded expectations.” Only then can you begin to create an opinion on whether the stock is going to go up or down.

Miller further states “A stock’s performance depends on fundamentals relative to expectations. For big winners, the gap between how a company actually performs and how it’s expected to perform is the widest.”

He has focused on buying companies with future expectations below what he thinks the firms will perform at.

Miller has built his entire investing career on this concept and by rejecting the notions of “value” or “growth” companies. Instead, he has built success searching for mispricing through understanding what the market expects of a firm.

Sometimes “value” stocks are expensive based on their market expectations. On the flip side, “growth” stocks can be cheap compared to embedded expectations.

Most traditional multiples are backward-looking and do not take into account the prospects of a company.

This philosophy led him to be a major early investor in Amazon. He owned close to 6% of shares of the company in 1999, well before it ever broke a profit.

This investment would have been considered ludicrous for a so-called “value investor,” but Miller’s understanding of future expectations and his rejection of typical investing terminology allowed him to see past this.

Miller is also focused on the cash flow of a business, rather than net income and metrics like P/E ratios. Businesses investing capital today to grow the business later will not look good under traditional GAAP accounting.

He produced these incredible returns at Legg Mason Value Trust, where he first joined as an analyst way back in 1981. He ultimately left in 2016 and formed his own company Miller Value Partners.

Today, we will highlight Miller Value Partners and The Miller Opportunity Trust.

This Fund has instilled many of the same strategies and values from Miller’s previous endeavors. Looking over the Opportunity Trust’s current holding in the context of Bill Miller’s historical performance may be instructive.

It is crucial to use Uniform Accounting when analyzing this fund’s current holdings to see what Miller is seeing.

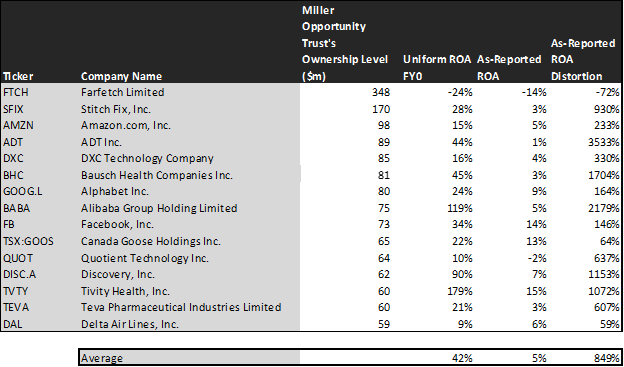

Using only as-reported metrics, it would appear Miller Opportunity Trust is buying sub-par companies with low returns and high market expectations. In reality, these names are significant players with high profitability.

See for yourself below.

Using as-reported accounting, investors would think Miller Opportunity Trust is picking weak companies, unable to generate a high return on assets (ROA).

On an as-reported basis, many of these companies are poor performers with returns below 5%, with the average as-reported ROA right around 5%.

In reality, the average company in the index displays an impressive average Uniform ROA of 42%.

Once we make Uniform Accounting (UAFRS) adjustments to accurately calculate earnings power, we can see the underlying strength of Miller Opportunity Trust’s picks.

When the distortions from as-reported accounting are removed, we can see that ADT, Inc. (ADT) does not have a negligible return of 1%, but a sizable ROA of 44%.

Similarly, Alibaba’s (BABA) ROA is really 119%, not at 5%. While as-reported metrics are portraying the company as a business below cost-of-capital returns, Uniform Accounting shows the company’s truly robust operations.

Tivity Health (TVTY) is another great example of as-reported metrics misrepresenting the company’s profitability. It does not have an 15% ROA, it is actually at 179%.

The list goes on from there, for names ranging from Bausch Health (BHC) and Discovery (DISC.A), to Alphabet (GOOGL) and Teva Pharmaceutical (TEVA).

If investors were to only look at as-reported metrics, they would assume Miller Opportunity Trust has thrown away a sound investment strategy to embrace low-return businesses. On the contrary, the fund is making smart investments to compound returns.

Beating the market isn’t just about buying great companies though. As Miller highlighted, it is about finding companies where market expectations are far too low based on the company’s fundamental potential.

When looking at the fund’s holdings through Uniform Accounting, it is clear it is doing just that.

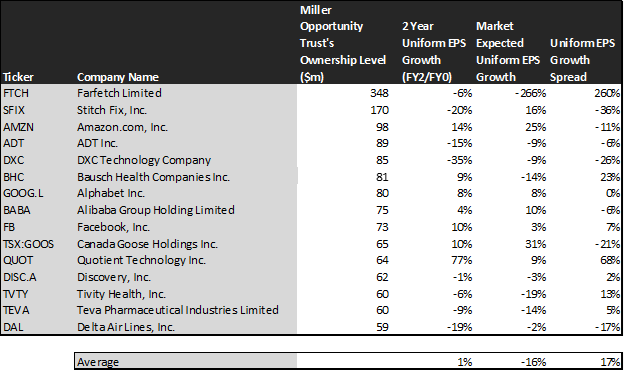

This chart shows three interesting data points:

- The 2-year Uniform EPS growth represents what Uniform earnings growth is forecast to be over the next two years. The EPS number used is the value of when we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market expected Uniform EPS growth is what the market thinks Uniform earnings growth is going to be for the next two years. Here, we show by how much the company needs to grow Uniform earnings in the next 2 years to justify the current stock price of the company. If you’ve been reading our daily analyses and reports for a while, you’ll be familiar with the term embedded expectations. This is the market’s embedded expectations for Uniform earnings growth.

- The Uniform EPS growth spread is the spread between how much the company’s Uniform earnings could grow if the Uniform earnings estimates are right, and what the market expects Uniform earnings growth to be.

The average company in the US is forecast to have 5% annual Uniform Accounting earnings growth over the next 2 years.

The market is pricing these companies for a sharp shrinkage in EPS growth at -16% a year. This huge gap between market expectations and analyst predictions shows how Miller Opportunity Trust looks to pick stocks with EPS growth potential.

One example of a company with high growth potential is Quotient Technology (QUOT). While the market expects Quotient to grow earnings by 9% annually over the next two years, analysts forecast the firm to grow 77% annually over the same period.

Another company with similar dislocations is Bausch Health (BHC). The company is forecast to grow Uniform EPS by 9% a year, and the market is expecting the company’s earnings to shrink 14% annually.

Yet another example is Facebook (FB). The company is cheap, as it is priced for 3% growth in Uniform earnings, but the company is forecast to in fact grow its EPS by 10% in the next two years.

That being said, there are some companies that are forecast to have earnings growth less than market expectations. For these companies, like Stitch Fix (SFIX) and Delta Air Lines (DAL), the market has growth expectations in excess of analysts’ predictions.

Sometimes an investor misses Uniform signals, or the fund might be betting on specific events for the company that make earnings forecasts less relevant.

Many investors spend too much time focusing on labels like “value” or “growth.” Those with a firm grasp of what the market is expecting a company to do can pick companies across the spectrum that will outperform.

By emphasizing companies with lower future expectations, Miller Opportunity Trust has managed to create value for investors with smart picks, as seen with Uniform Accounting.

SUMMARY and Farfetch Limited Tearsheet

As one of Miller Opportunity Trust’s highest individual stock holdings, we’re highlighting Farfetch Limited’s tearsheet today.

As the Uniform Accounting tearsheet for Farfetch Limited (FTCH:USA) highlights, the Uniform P/E trades at -52.4x, which is below the global corporate average of 25.2x and its historical P/E of -23.9x.

Low P/Es require low EPS growth to sustain them. In the case of Farfetch, the company has recently shown a 66% growth in Uniform EPS.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Farfetch’s Wall Street analyst-driven forecast is a 573% UAFRS EPS growth in 2020 and an 87% EPS shrinkage in 2021.

Furthermore, the company’s earning power is below the corporate average. Also, the company’s cash flows and cash on hand are above their total obligations—including debt maturities and capex maintenance. This signals a low credit risk.

To conclude, Farfetch’s Uniform earnings growth is significantly above its peer averages in 2020. However, the company is trading well below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research