Moody’s reputation got burned by the housing collapse in the late 2000s, it is still penalizing the industry because of it

Credit agencies were largely criticized following the Great Recession for their inability to accurately portray the credit risk of mortgage-backed securities until after the market collapse.

This firm shows that, as a byproduct of its damaged reputation in the space, Moody’s may still be overly hesitant about the housing industry. Instead of paying attention to economic reality, it is giving this company a highly-speculative rating, despite investment-grade fundamentals.

Below, we show how Uniform Accounting restates financials for a clearer credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Jim Chanos, president and founder of Kykinos Associates, a famed investment advisory focused on short-selling, once stated:

“If the rating agencies will downgrade only when we can all see the losses, then why do we need the rating agencies?“

Chanos’s question reflects one of growing sentiments among investors following the Great Recession. Ratings agencies lag economic reality.

Prior to the recession, rating agencies, such as Moody’s and S&P, would consistently give mortgage-backed securities AAA-ratings. AAA represents the highest rating possible.

These investments were supposed to be extremely safe, with little to no risk. As a result, many investors and institutions readily bought into these assets.

The rest is history. The housing bubble burst and investors soon learned that these mortgage-backed securities were full of subprime, and often recklessly distributed, underlying assets.

As default rates skyrocketed, the value of these securities plummeted, and the market suffered tremendously.

However, although the recession started at the end of December 2007, the ratings agencies didn’t downgrade a bulk of these securities until early to mid-2008, well after the market had known of their faults.

In all, over $1.5 trillion worth of mortgage-backed securities were downgraded. By the end of the recession, an estimated 73% of Moody’s 2006 AAA-rated CDOs (collateralized debt obligations) had been downgraded to junk status.

A driving force behind the credit rating agencies’ failure lies in their reliance on bad data. First, the agencies over-rely on historical data, which by nature, will trail economic reality. Second, the agencies often use as-reported metrics, which further distort the firms’ ability to gain accurate insights.

For any creditor, the core question for credit risk lies in a company’s ability to pay off its debts. If a company can pay off its debts with no issues, then it should be an investment grade.

For instance, Builders FirstSource (BLDR), a manufacturer and supplier of building materials for homebuilders, is a company that seems to be able to do so.

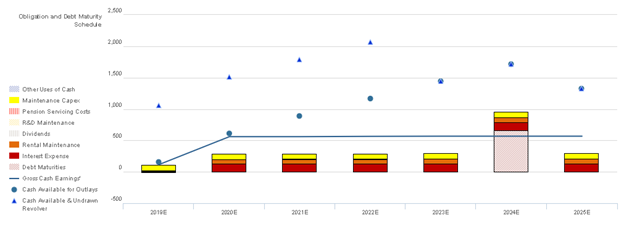

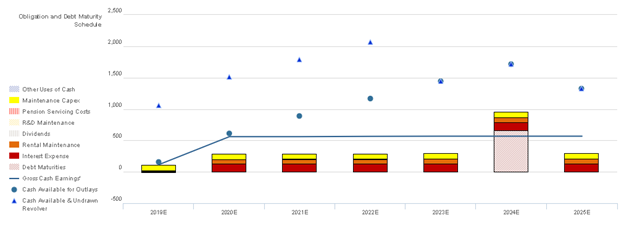

As evident in the chart below, Builders has cash flows and an expected cash build that should comfortably cover all obligations, including debt maturities going forward.

In addition, with no material debt headwall until 2024, the firm has plenty of room to adjust if its cash flows start to falter in out years.

As such, it should be a no-brainer that Builders could pay off its debts, which is why we rate the firm as an investment-grade (IG4) name.

However, Moody’s rating tells a different story. With its highly-speculative B1 rating, Moody’s implies that Builders is an imminent default risk, grouping it in a universe where nearly a fifth of firms default within 5 years.

Although Builders did have negative ROAs in the middle of a once-in-a-generation housing crisis, it has since recovered valiantly to near-peak levels in recent years.

This again shows how Moody’s and credit agencies are missing the mark on accurately portraying credit risk. Moody’s is hesitant to upgrade a firm that is in an industry which has burned it before, and has largely damaged its reputation. Instead it is completely ignoring the company’s fundamentals.

Using Uniform Accounting we can see why investors are not pricing the firm’s bonds as high risk assets, with yields that are more in-line with Valens’ IG4 rating. Markets do not seem to have the same misguided reservations about past history as credit agencies.

When investors pay more attention to economic reality as opposed to Moody’s distorted as-reported accounting analysis, they get a better understanding of where credit risk is heading.

Ratings Improvement Likely as BLDR’s Robust Cash Flows and Sizeable Cash Build Continue to be Overlooked

Credit markets are accurately stating credit risk with a cash bond YTW of 3.894%, relative to an Intrinsic YTW of 4.054% and an Intrinsic CDS of 243bps.

However, Moody’s is materially overstating Builders’ fundamental credit risk with its highly speculative, high-yield B1 rating, five notches lower than Valens’ IG4 (Baa2) rating.

Fundamental analysis highlights that Builders’ cash flows would materially exceed operating obligations in each year going forward. Moreover, the firm’s combined cash flows and expected cash build should be sufficient to service all obligations through 2025, including a material $661mn debt headwall in 2024.

This is vital, as the firm’s neutral 55% recovery rate and modest market capitalization may make it difficult to access credit markets to refinance on favorable terms.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for credit holders.

Builders’ management compensation structure should drive them to focus on growth, margins, and asset efficiency, which should lead to Uniform ROA expansion and higher cash flows available for servicing obligations.

Also, management is not well-compensated in a change-in-control, indicating they are unlikely to pursue a sale or accept a buyout of the firm, decreasing event risk for creditors.

That said, most management members are not material owners of Builders equity relative to their average annual compensation, indicating they may not be aligned with shareholders for long-term value creation.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (11/1) highlights that management is confident they have a competitive position within the market.

However, they may lack confidence in their ability to improve their profitability through implementing pricing tools, and they may be concerned about the demand for their higher margin products.

Furthermore, they may lack confidence in their ability to source accretive M&A opportunities and improve their market share.

Finally, they may lack confidence in their ability to sustain net income improvements and meet their capex spend guidance.

Given BLDR’s robust cash flows and sizable expected cash build, Moody’s is materially overstating credit risk. As such, a ratings improvement is likely going forward.

SUMMARY and Builders FirstSource, Inc. Tearsheet

As the Uniform Accounting tearsheet for Builders FirstSource, Inc. (BLDR) highlights, the company trades at a 17.4x Uniform P/E, which is below global corporate average valuation levels but is in line with its own history.

Low P/E’s only require low—or even negative—EPS growth to sustain them. That said, in the case of Builders, the company has recently shown a robust 314% Uniform EPS growth, significantly above what is required.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Builders’ Wall Street analyst-driven EPS growth forecast flipped from negative to positive.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $27 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for Builders, the company would have to have Uniform earnings shrink by 6% or less each year over the next three years.

Wall Street analysts’ expectations for Builders’ earnings growth are below what the current stock market valuation requires in 2019, but far above the requirement in 2020.

In addition to Builders’ low valuations, its Uniform P/E and Uniform EPS growth are both below peer averages.

Meanwhile, the company’s earnings power is 2x corporate averages, signaling very low risk to its dividend or operations.

To summarize, Builders is expected to see below average Uniform earnings growth in 2019, which is not expected to continue in 2020. Furthermore, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research