For some time, ESG has looked like a fad, Uniform Accounting shows this ESG-focused cloud computer business is anything but

Socially responsible investing or ESG investing has increased in relevance in recent years, and recent events around the world point towards an even greater shift towards ESG investing themes.

Today’s company has an ESG focus and a cloud computing background, which should make it a compelling company, but its low as-reported returns imply it’s just another ESG fad company without the fundamentals to warrant premium valuations.

Uniform Accounting shows why that conclusion may be incorrect, and this may be an example of the new thinking around ESG, that being socially responsible and profitable are not mutually exclusive.

Also below, Uniform Accounting Embedded Expectations Analysis and the Uniform Accounting Performance and Valuation Tearsheet for the company.

Investor Essentials Daily:

Thursday Tearsheets

Powered by Valens Research

Socially responsible investing, or ESG (environmental, social, governance) focused investing is built around the idea that corporations should not solely be focused on profits, but also on social and environmental good.

As the world has become more aware of environmental, social, and governance-related issues, companies are being forced to consider how they achieve those tenets. It is possible companies that are focused on these issues can generate wealth more sustainably. Even if that were not the case, at the very least, the public would be less likely to view these companies negatively

Investors are also taking notice of these factors.

Recent Morningstar data shows that sustainable funds reached a record-high net inflow of $10.5 billion in the first quarter of 2020, even as the general market plunged. Investors are recognizing that good governance can reduce headline risk for the firms in which they invest. In a market recently driven by headlines, that is a positive.

Additionally, in research done at the University of Hamburg, it was found that nearly all studies showed ESG had a non-negative relationship with corporate financial performance. A majority highlighted a positive relationship between the two. Even looking beyond the headline benefits, there would appear to be actual, tangible value in companies focused on ESG.

Unfortunately, it can sometimes be difficult to find investments that combine high-quality fundamentals, intriguing valuations, and a healthy focus on ESG. The iShares U.S. ESG ETF has performed roughly in line with the S&P since inception. The global equivalent has underperformed. This data at least doesn’t appear to show alpha exists in ESG.

At first glance, Blackbaud, Inc. (BLKB) looks like it could be just another one of those strong ESG, weak fundamental companies.

The firm is focused on bringing cloud computing technology to firms focused on the “social good.” Examples include bringing financial management tools to faith communities and for K-12 programs, and marketing and engagement tools to arts and cultural organizations.

Cloud computing and ESG make for quite the combination of in-vogue buzzwords currently. Unfortunately, as-reported financials make the firm look nearly uninvestable.

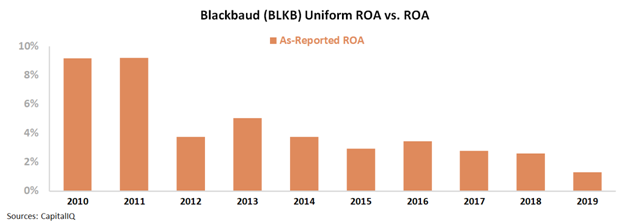

For context, as-reported ROA has fallen massively recently, from already modest levels.

Meanwhile, as-reported P/E levels are at 29x currently, well above corporate averages of around 20x-22x. At first glance, this appears to be just another company with a good story but poor fundamentals.

Fortunately, the as-reported financials are wrong.

Once the appropriate adjustments under UAFRS are made, it becomes clear this is a much better business than investors might realize. This isn’t a barely-profitable business with sky-high valuations.

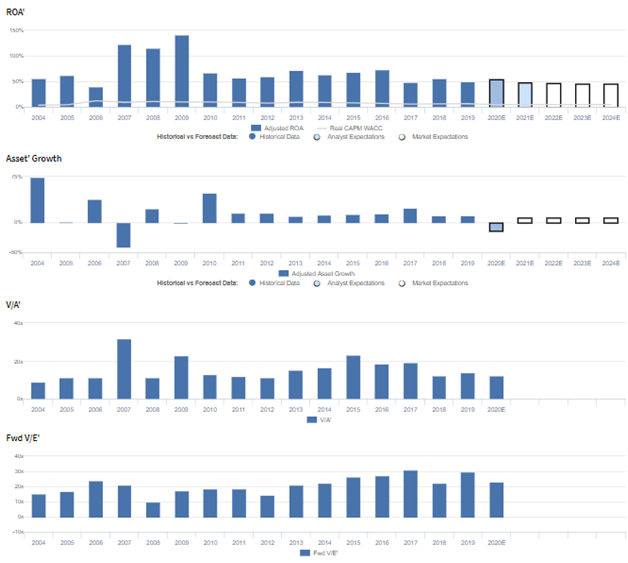

In fact, Uniform ROA has been comfortably over 45% over the last decade, highlighting the strength of this business model:

Even though the firm has seen Uniform ROA come down slightly recently, this has largely been a factor of continued, massive investment in the business, not fundamental weakness in earnings. This is a strong business that is compounding those returns to create value for shareholders.

More interestingly, Blackbaud shares are trading at a 24x Uniform P/E, suggesting the name isn’t overly expensive, either. At this valuation, investors are getting a company with major ESG and cloud-computing-based tailwinds, with near best-in-class profitability at market averages.

It is worth noting the recent earnings call highlights some potential concerns from management that point to near-term volatility for the name, but for investors focused on investing for the future, as those investing in ESG are, this ought to not completely turn them off to the name.

Blackbaud, Inc. Embedded Expectations Analysis – Market expectations are for slight Uniform ROA declines, and management may be concerned about costs, their positioning, and data centers

BLKB currently trades near corporate averages relative to Uniform earnings, with a 24.1x Uniform P/E (Fwd V/E’). At these levels, the market is pricing in expectations for Uniform ROA to remain at 49% levels through 2024, accompanied by 8% Uniform asset growth going forward.

Analysts have similar expectations, projecting Uniform ROA to decline slightly to 48% by 2021, though accompanied by 14% Uniform asset shrinkage.

Historically, as a cloud computing provider, BLKB has seen robust, but volatile profitability. After fading from 56% in 2004 to 40% in 2006, Uniform ROA jumped to 115%-141% levels in 2007-2009 before collapsing to 57% in 2011. Thereafter, Uniform ROA expanded to 73% by 2016 before compressing to 49% in 2019.

Meanwhile, due to its asset light balance sheet, Uniform asset growth has also been robust, but volatile, positive in fourteen of the past sixteen years, while ranging from -41% to 48%, excluding 74% growth in 2004, driven by the firm’s IPO.

Performance Drivers – Sales, Margins, and Turns

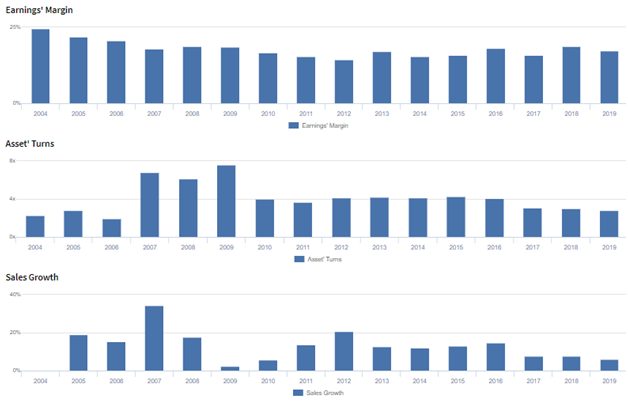

Trends in Uniform ROA have been largely driven by volatility in Uniform asset turns, coupled with general declines in Uniform earnings margin.

Uniform asset turns jumped from 2.0x-2.8x levels in 2004-2006 to 6.2x-7.6x levels in 2007-2009 before collapsing to 3.7x-4.2x levels through 2016 and compressing further to 2.8x in 2019.

Meanwhile, Uniform earnings margins declined from 25% in 2004 to 14% in 2012 before recovering to 19% by 2018 and fading to 17% in 2019.

At current valuations, markets are pricing in expectations for both Uniform earnings margins and Uniform asset turns to stabilize near current levels.

Earnings Call Forensics

Valens’ qualitative analysis of the firm’s Q4 2019 earnings call highlights that management generated an excitement marker when saying they have introduced a large number of new features using their SKY engineering platform, and they are confident that much of their structural transition is now behind them.

However, they are also confident they will have tough growth comparisons as they are on the backside of their transition from legacy to next-gen products. In addition, management may be concerned about the impact of consistent restructuring costs, headcount increases, and their education partnership with Microsoft.

Moreover, they may be exaggerating their future restructuring cost savings, the strength of their long-term positioning, and the reach of the Your Cause platform. Finally, they may be concerned about the progress of their migration from colo data centers to third party cloud data centers, and they may lack confidence in their ability to balance profitability and growth.

UAFRS VS As-Reported

Uniform accounting metrics also highlight a significantly different fundamental picture for BLKB than as-reported metrics reflect.

As-reported metrics can lead investors to view a company to be dramatically stronger or weaker than real operating fundamentals highlight. Understanding where these distortions occur can help explain why market expectations for the company may be divergent.

As-reported metrics significantly understate BLKB’s profitability. For example, as-reported ROA for BLKB was just 1% in 2019, substantially lower than Uniform ROA of 49%, making BLKB appear to be a much weaker business than real economic metrics highlight.

Moreover, since 2014, as-reported ROA has not exceeded 4%, while Uniform ROA has not fallen below 48% over the same timeframe, distorting the market’s perception of BLKB’s historical profitability ceiling.

SUMMARY and Blackbaud, Inc. Tearsheet

As the Uniform Accounting tearsheet for Blackbaud (BLKB) highlights, the Uniform P/E trades at 24.1x, which is above corporate average valuation levels and below its own recent history.

Average P/Es require average EPS growth to sustain them. In the case of Blackbaud, the company has recently shown a 6% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Blackbaud’s Wall Street analyst-driven forecast is a 6% and 9% shrinkage in 2020 and 2021, respectively.

Based on current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Blackbaud’s $60 stock price. These are often referred to as market embedded expectations.

The company needs to have Uniform earnings grow by 7% each year over the next three years to justify current prices. What Wall Street analysts expect for Blackbaud’s earnings growth is below what the current stock market valuation requires in 2020 and 2021.

Furthermore, the company’s earning power is 8x the corporate average. However, cash flows are below their total obligations—including debt maturities, capex maintenance, and dividends. Together, this signals moderate risk for their dividend.

To conclude, Blackbaud’s Uniform earnings growth is below peer averages in 2020. In addition, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research