Bloomberg says insider selling may be a worrying sign, our mosaic tells a different story

Executives know their companies better than anyone. That is why insider selling and buying can be such important indicators.

Today, we will look at recent trends in insider investing and what that means for investors.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

All data points are important; however, as we discussed two weeks ago, it is necessary to look at data points as a mosaic. While looking at one datapoint has the ability to give insights into the macroeconomic picture, an investor cannot be confident until multiple data points reaffirm the same theory.

A great example of this in action is management intent.

Investors love looking at insider buying and selling. Recently, a Bloomberg article highlighted how executives of companies in the S&P 500 have been unloading shares.

This is a marked change from the beginning of the pandemic. In mid-March, insider buying hit a nine-year high as stock prices were crashing. While investors everywhere became worried about the coronavirus pandemic, executives who knew their companies’ performance and knew the world wasn’t ending voted with their wallets. They used the opportunity to buy more of their company’s stock at cheap valuations.

Now that the S&P 500 is up 50% from its trough, those executives appear to be locking in their profits.

The recent shift in insider trading trends could worry investors. However, it is only a single metric, so it must be looked at in context.

The reason for shift may be because of the stock market appreciation in recent months. Management members tend to subscribe more to value investing than growth investing.

When prices dip and they don’t have reason to be concerned about their business operations, they buy. As stock prices rise in a short period of time, valuations rise as well, some management teams may sell.

Now that valuations do not look as attractive as six months ago, management members may be deciding to unload some shares.

However, just because management teams are selling shares does not mean they think their company’s stock is overvalued or will freefall.

There are countless reasons why management teams sell stock. The first is for liquidity. While stocks have value, they cannot be used to purchase anything.

Some executives may be interested in buying a new house, following the trends of the At-Home Revolution to move out of the city. Others may need to put their kids through college now that the academic season has started again or diversify out of their company.

Another reason is uncertainty in the short-term. With the elections coming up and questions over the coronavirus and a stimulus package abound, executives may just be concerned about the following months.

That all assumes the data from Bloomberg is right. Because the reality is even if insider selling rises, if some insiders are also actively buying too, then selling alone isn’t a warning sign. That says in aggregate management teams aren’t getting concerned.

And that is exactly what the bigger picture says right now. When looking at the buy/sell ratio of US corporate management teams, it’s not at low levels at all. In fact, outside of big market sell-offs like December 2018 or in particular like in March this year, insider buying to selling is currently at average levels.

Contrary to the Bloomberg article, management teams aren’t running for the hills.

Looking at buying versus selling is relevant because there are countless explanations why an executive may sell out of their company. However, there is only one reason they will buy on the open market, as opposed to from share grants; they think the stock will go up. To figure out exactly why executives may be buying or selling, we can use our Earnings Call Forensics (ECF) technology.

As we highlighted a couple of months ago when discussing the Federal Reserve, our technology can help us get unique insight into human sentiment. Alongside anchoring market trends, the ECF allows us to gain a clearer picture of management outlook.

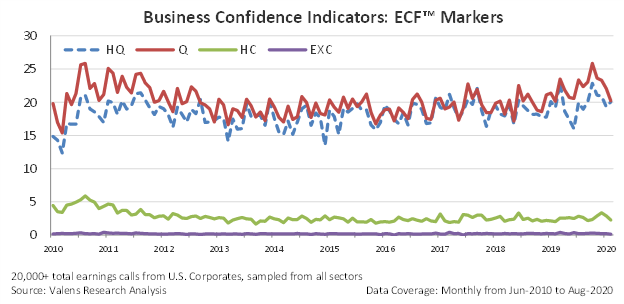

Our ECF data shows us when management members are “highly questionable”, “questionable”, “highly confident”, and “excited”.

Highly questionable markers signal management may be holding back on communicating what they’re really thinking about a subject. Highly confident markers signal management has conviction in what they are talking about. Excitement markers, which are exceedingly rare, highlight literal giddiness from management on a subject.

As the graph below shows, highly questionable and questionable markers have decreased in recent months. After significant uncertainty grew in the few months up to March and April 2020, in May management teams started showing less uncertainty and concern about the visibility in their outlook for businesses.

Unsurprisingly as that happened, initially, management teams also got more confident about opportunities for investment, as seen by the rise in highly confident markers. Subsequently, however, even as management teams remain less concerned about surprises, they also are getting less confident about investing in growth.

So even for those insiders who are selling, if they are not selling for personal reasons, it appears in aggregate the reason is less because they are worried about their companies’ outlook, and more because they are less bullish about growth.

Understanding management sentiment is essential when trying to map out the future of a business. After all, these are the people driving a company’s stock through their strategies and execution. Their optimism or pessimism about their company and plan can provide us clues as to how a company may perform in the future which is essential to an investors’ mosaic.

While Bloomberg may be concerned about insider selling, in the context of both buying and selling, and where management sentiment is heading, we see there’s much less cause for concern about this being a sign that the market is about to roll over.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research