Bond investors are almost never more bullish than equity investors, but they are for this company. UAFRS shows it is setting them up for a big loss

Everyone knows about retail’s demise and how painful the last few years have been for brick and mortar stores.

Below, we talk about why one name in the space has been particularly punished by the stock market but how bond investors appear to not be aware the other shoe is about to drop.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

Three years ago, we wrote an article on Seeking Alpha, highlighting that the whole Retail industry looked overvalued.

At the time, there were early signs of profitability issues in that segment of the market, but our analysis showed a number of companies still trading at premium valuations. It’s possible the market hadn’t quite caught on.

Since then…

…the industry has barely moved, while the whole S&P is reaching new highs almost every day. In the last three years, the S&P is up 50%+, while the XRT has only risen 3% over the same time frame.

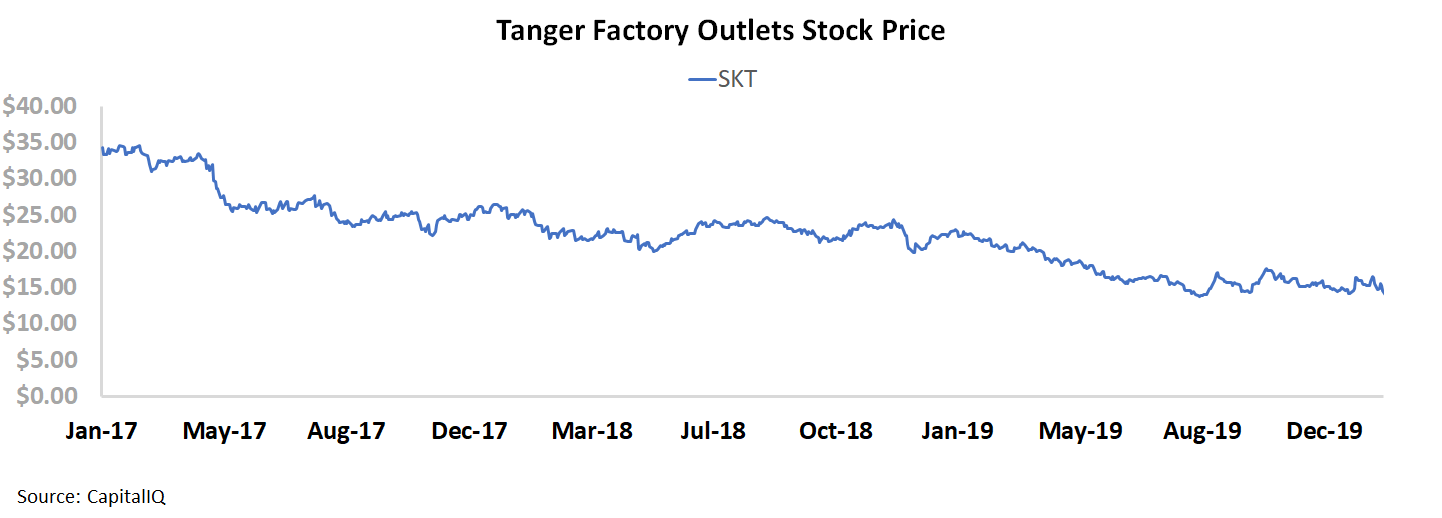

One of those retail names that significantly underperformed the market was Tanger Factory Outlets. In fact, it’s down 60% since that article:

This is a name that has faced more pressure than even most of its peers in retail. That is because it isn’t just a traditional retail company.

We’ve talked before about buying companies that “sell the picks and shovels.” During the gold rush, the people that made the most money sold tools, they weren’t the ones prospecting.

Companies that supply competitive and growing markets can often do very well, even if their customers don’t.

The problem is when people stop buying picks and shovels, as we talked about when writing about Schlumberger in January.

Tanger is a company that owns the outlets that premium retail companies lease to have a brick and mortar presence. When those companies competed for space, Tanger won.

Unfortunately, Amazon and e-commerce have entered the picture, and people no longer feel the need to travel to Tanger’s outlets. Now Tanger’s customers are competing for less space and an online presence instead.

As a REIT, Tanger owns 39 shopping center locations across the US and Canada. These shopping centers have tenants like Nike, lululemon, and Adidas, which have all done very well in recent years.

They also have tenants like Coach, Under Armor, and Gap, which have done less well. The thing all those companies have in common is that they’re trying to compete digitally now. They don’t care as much about floor space.

That’s why Tanger’s stock has gotten crushed, and it may be justified. Also, after falling 60%, the company currently has a 10% dividend yield. Yields like this aren’t usually sustainable and equity investors are betting that dividend cuts are coming, which could lead to further downside.

But it doesn’t appear anyone has told the bondholders.

During this massive slide, Tanger bonds are actually up. The chart below shows the company’s 2023 bond price over the last three years:

This isn’t some high-yielding bond, either. At current prices, the yield is around 3%, or less than ⅓ of the current dividend yield.

Equity investors are pounding the table calling for a dividend cut at these levels. They have significant concerns about Tanger’s cash flows, while bond investors couldn’t care less.

Those bond investors are probably wrong.

Our analysis highlights that equity markets are right to be concerned. When looking at the cash flows projected for Tanger compared to its obligations over the next few years, the picture isn’t a good one.

Even if the company cuts its dividend, several debt headwalls and significant interest expense will pressure Tanger’s declining cash flows. And the act of cutting the dividend would be just as bad a signalling issue for the credit as it would be for the equity.

It’s hard to envision a scenario where bond markets and equity markets are both right. Looking at the firm’s outlook, even if they don’t go bankrupt, it’s apparent this may be a rare situation where bond investors may be overly optimistic, not the equity.

Poor cash flows and material debt headwalls indicate that credit markets and ratings agencies are understating credit risk

Fundamental analysis highlights that SKT’s cash flows would fall short of operating obligations in each year going forward.

Furthermore, the combination of the firm’s cash flows and cash on hand would fall short of servicing all obligations, including debt maturities, in each year going forward.

Although the firm can significantly reduce capex spend to free up liquidity in the near-term, SKT will likely have to refinance in order to cover material $247mn and $595mn debt headwalls in 2023 and 2024, respectively.

Incentives Dictate Behavior™ analysis highlights positive signals for creditors.

SKT’s compensation metrics should focus management on all three value drivers: asset efficiency, margins, and top-line growth, leading to Uniform ROA expansion and increased cash flows available to service obligations.

Meanwhile, the consolidated debt to adjusted total asset ratio should discourage management from overleveraging their balance sheet.

In addition, most management members are material owners of SKT equity, relative to their average annual compensation, indicating that they are well-aligned with shareholders for long-term value creation. `

Moreover, other than General Counsel Perry and COO McDonough, most management members have low change-in-control compensation, implying they are unlikely to accept a buyout or pursue a sale of the company, reducing event risk.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (10/31) highlights that management may be concerned about their value proposition for consumers, and they may lack confidence in the effectiveness of their leasing strategy.

Furthermore, they may be exaggerating the low cost of occupancy of outlets for retailers, and they may lack confidence in their ability to expand their digital outreach effectively.

Finally, they may lack confidence in their ability to efficiently invest in their assets, and they may be concerned about the value of their recent share buyback program.

Poor cash flows and material debt headwalls indicate that credit markets and Moody’s are understating SKT’s fundamental credit risk. As such, a widening of credit spreads and a ratings downgrade are likely going forward.

SUMMARY and Tanger Factory Outlets Tearsheet

As the Uniform Accounting tearsheet for Tanger Factory Outlet Centers, Inc. (SKT) highlights, the company’s Uniform P/E trades at 21x, which is around global average valuation levels and previous period valuations.

Low P/E’s require low, and even negative, EPS growth to sustain them. In the case of SKT, the company has recently seen its Uniform EPS decline, which may be a signal that below-average valuations are justified.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, SKT’s Wall Street analyst-driven EPS growth forecast flipped from positive to negative.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $15 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for SKT, the company would have to have Uniform earnings shrink by 2% each year over the next three years.

Despite a weak year this year, Wall Street analysts’ expectations for SKT’s earnings growth are above what the current stock market valuation requires.

In addition to SKT’s valuations being low, its Uniform P/E is significantly lower than peer averages, while its Uniform EPS growth is fairly above peer averages.

Meanwhile, the company’s earnings power is slightly above the corporate averages, signaling a high risk to its dividend or operations.

To summarize, Tanger Factory Outlet Centers, Inc. is an average-earning company with a high earnings growth potential and muted embedded expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research