Uniform Accounting unveils the surge in demand for automation in the semiconductor space, powering Brooks Automation

If the world has learned anything over the course of the pandemic, it is that semiconductor chips are at the heart of almost every modern technology, from Apple iPhones to Ford pickup trucks.

The current chip shortage partly stems from the fact that semiconductor fabrication plants are among the most complex operations in all of manufacturing, meaning the process of building more capacity to meet demand takes large amounts of time and money.

Yet, as the world needs an ever increasing supply of chips, more capacity will be built, and for one provider of the automation solutions factories rely on, as-reported metrics fail to see just how strong demand truly is.

Also below, the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

There is a lot of buzz in the media and investors about the coming revolutions in automation and the Internet of Things (“IoT”), and how they will forever change manufacturing processes around the world.

At the heart of these transitions are semiconductor chips, an essential component to the electronic devices that enable smart machines and automated processes to function in the first place.

What many often glance over or fail to appreciate is that the same semiconductor “fabs”—the plants where integrated circuits are manufactured—are themselves massive adopters of automation technology.

The factories where semiconductor chips are produced are among the most advanced, complex buildings in the world, as each chip requires the utmost level of accuracy and precision.

If a single wafer, the thin slice of silicon material used as the base of semiconductor chips, is contaminated, the whole manufacturing process is called into question. This means fabs are cleaner than a surgical room, and require workers to wear Hazmat-type suits that look like they are taken straight from an infectious disease lab.

By using industrial robots and other automation technologies, semiconductor fab giants like Taiwan Semiconductor Manufacturing (TSM) can become leaner and cleaner, leading to higher volumes and greater quality chips.

To do this innovative manufacturing, there’s one company that many in the semiconductor industry turn to: Brooks Automation (BRKS).

Brooks Automation helps semiconductor fabrication plant operators automate their processes, such as the cleaning and inspection of precious wafers, which speeds up the overall manufacturing timeline and requires less workers.

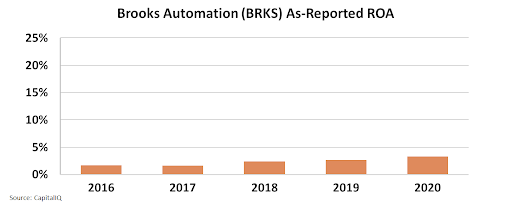

While the company supports a booming industry that is reliant on its technology to keep scaling, particularly now in the midst of an acute chip shortage, Brooks Automation’s weak as-reported return on assets (“ROA”) suggests the market is significantly underpricing its technological power.

Yet, taking a deeper look with Uniform Accounting, it is clear the company’s true ROA has been comfortably above 10% since the semiconductor demand spike, highlighting that the strength of demand for its automation solutions in this newest boom is much greater than as-reported metrics reflect.

See for yourself below…as-reported metrics dramatically fail to capture the scale of the company’s profitability ramp up starting in 2018.

Brooks Automation supplies an innovative suite of products and services that are essential to one of the global economy’s most booming and critical industries. Nevertheless, as-reported metrics portray a story of a company with below cost of capital returns that are only slowing pushing higher.

As economies and even militaries become ever more dependent on semiconductor chips to function, the importance and focus placed on companies like Brooks Automation will only accelerate, with returns likely to follow.

SUMMARY and Brooks Automation, Inc. Tearsheet

As the Uniform Accounting tearsheet for Brooks Automation, Inc. (BRKS:USA) highlights, the Uniform P/E trades at 38.6x, which is above the global corporate average of 24.3x and its historical P/E of 27.6x.

High P/Es require high EPS growth to sustain them. In the case of Brooks Automation, the company has recently shown a 164% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Brooks Automation’s Wall Street analyst-driven forecast is a 10% and 25% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Brooks Automation’s $93 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow 24% annually over the next three years. What Wall Street analysts expect for Brooks Automation’s earnings growth is below what the current stock market valuation requires in 2021, but above that requirement in 2022.

Furthermore, the company’s earning power in 2020 is 3x the long-run corporate average. Moreover, cash flows and cash on hand are more than 2x its total obligations—including debt maturities, capex maintenance, and dividends. All in all, this signals a low credit and dividend risk.

Lastly, Brooks Automation’s Uniform earnings growth is around peer averages, while the company is trading below its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research