If Buffett isn’t worried, you shouldn’t be either

Studies have shown that credit rating downgrades lead to a significant market reaction.

Usually, this is company-specific. However, Fitch has investors intrigued with its newest downgrade on the entire United States.

Recently, Fitch has downgraded U.S. credit from the top AAA grade to AA+. In light of such negative news, one investor saw no real concern for this change, Warren Buffett.

Buffett, CEO of Berkshire Hathaway, most recently came out and said, “There are some things people shouldn’t worry about. This is one.”

It’s clear that Buffett sees no issue with the standing of U.S. debt. With that being said, let’s take a look at Berkshire Hathaway’s top holdings and see if his market views are reflected in his current portfolio.

In addition to examining the portfolio, we include a deeper look into the fund’s largest current holding, providing you with the current Uniform Accounting Performance and Valuation Tearsheet for that company.

Also below is a detailed Uniform Accounting tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

The economy is not clear-cut.

However, if there is one person to look at in times of uncertainty, Warren Buffett would be a solid choice.

When everyone turned their backs on banks during the financial crisis, Buffett acted against the broader market and hammered money in Goldman Sachs (GS) and Bank of America (BAC).

What may have seemed like a radical move back then, actually proved to be an extremely profitable play, in which Buffett earned about $15 billion from the total investment.

This is just one instance where Buffett bet against the herd, it’s been seen several times throughout his career.

Therefore, Buffett’s fairly successful track record brings validity when he says that the U.S. debt downgrade from Fitch is nothing to worry about.

Though downgrades are not uncommon, U.S. debt hasn’t been downgraded by a major credit rating agency since 2011. That 2011 downgrade had a tremendous market impact, including the S&P 500 dropping 6% within days of the news.

Part of the surprise of this credit rating change is the U.S. treasuries are regarded as one of the safest assets in the world, in part because the U.S. has never defaulted or missed a payment on its debt.

Warren Buffett put his money where his mouth is. He bought $10 billion worth of U.S. treasuries every week for several weeks straight.

In all, it appears Buffett has used this recent Fitch rating as a buying opportunity more than anything else.

Amid this historic downgrade, let’s look into Berkshire Hathaway’s top holdings and see if Buffett’s market expertise and stance play a role in how his portfolio is positioned today.

Economic productivity is massively misunderstood on Wall Street. This is reflected by the 130+ distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, as well as flawed acquisition accounting.

It’s no surprise that once many of these distortions are accounted for, it becomes apparent which companies are in real robust profitability and which may not be as strong of an investment.

See for yourself below.

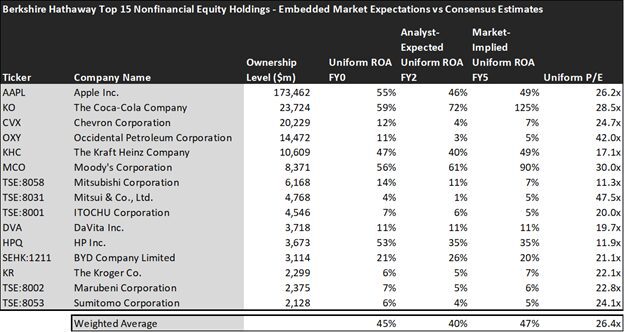

Looking at as-reported accounting numbers, investors would see that Berkshire Hathaway invests in some high-quality companies.

On an as-reported basis, many of the companies in the fund are above-average performers. The average as-reported ROA for the top 15 holdings of the fund is 16%, which is higher than the 12% U.S. corporate average.

However, once we make Uniform Accounting adjustments to accurately calculate the earning power, we can see that the average return in Berkshire Hathaway’s top 15 holdings is tremendously more profitable than what as-reported metrics show, which is coming in at 45%.

As the distortions from as-reported accounting are removed, we can see that HP (HPQ) isn’t a 9% return business. Its Uniform ROA is 53%.

Meanwhile, Moody’s Corporation (MCO) also looks like a 9% return business, but this financial services company powers a 56% Uniform ROA.

That being said, to find companies that can deliver alpha beyond the market, just finding companies where as-reported metrics misrepresent a company’s real profitability is insufficient.

To really generate alpha, any investor also needs to identify where the market is significantly undervaluing the company’s potential.

These dislocations demonstrate that most of these firms are in a different financial position than GAAP may make their books appear. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The average Uniform ROA among Berkshire Hathaway’s top 15 holdings is actually 45%, which is much better than the corporate average in the United States.

- The analyst-expected Uniform ROA represents what ROA is forecasted to do over the next two years. To get the ROA value, we take consensus Wall Street estimates and convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here are 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, the average Uniform P/E across the investing universe is roughly 20x.

Embedded Expectations Analysis of Berkshire Hathaway paints a clear picture. Over the next few years, Wall Street analysts expect the companies in the fund to drop in levels of profitability. Meanwhile, the market has expectations for these companies to surpass their current performance.

Analysts forecast the portfolio holdings on average to see Uniform ROA slightly decrease to 40% over the next two years. At current valuations, the market’s expectations are notably higher than analysts and it expects a 47% Uniform ROA for the companies in the portfolio.

For instance, Kraft Heinz (KHC) returned 47% this year. Analysts anticipate its returns slightly decrease to about 40%. Comparably, the market thinks the company’s profitability will increase its current levels therefore pricing its Uniform ROA at 49%.

Similarly, Mitsui (TSE:8031) has a Uniform ROA of 4%. Analysts expect its returns to see a decline to around 1%, but the market is slightly more optimistic about the company and pricing its returns to be around 5%.

Since Buffett took over Berkshire Hathaway in 1965, the company has recorded a compounded annual gain of 19.8%, or nearly double the S&P 500’s 9.9% compound annual gain. He has beaten the market 39 out of 58 years.

Buffett’s market expertise is undeniable when looking at his returns throughout his career. He doesn’t always follow consensus views and his recent disregard for Fitch’s rating is indicative of this principle.

Along with investing predominantly in US-based companies, Buffett shows his belief in the country’s financial strength by adding safer assets like U.S. treasuries to his portfolio.

Additionally, the state of Berkshire Hathaway’s portfolio and anticipated market returns show that Buffett may continue to beat the market with the high-quality companies he has in the portfolio.

While many of the holdings are already significantly outperforming the U.S. corporate average, the market still expects these companies to expand profitability even further.

This situation may limit upside potential for investors as the market is already pricing in possible improvements for these businesses over the next five years.

However, there is always news coming out about the market and if you are ever unsure of where it’s headed, taking a look at what Buffett has to say could be an important source.

This just goes to show the importance of valuation in the investing process. Finding a company with strong profitability and growth is only half of the process. The other, just as important part, is attaching reasonable valuations to the companies and understanding which have upside which has not been fully priced into their current prices.

To see a list of companies that have great performance and stability also at attractive valuations, the Valens Conviction Long Idea List is the place to look. The conviction list is powered by the Valens database, which offers access to full Uniform Accounting metrics for thousands of companies.

Click here to get access.

Read on to see a detailed tearsheet of one of Berkshire Hathaway’s largest holdings.

SUMMARY and The Coca-Cola Company Tearsheet

As one of Berkshire Hathaway’s largest individual stock holdings, we’re highlighting The Coca-Cola Company (KO:USA) tearsheet today.

As the Uniform Accounting tearsheet for The Coca-Cola Company highlights, its Uniform P/E trades at 28.5x, which is above the global corporate average of 18.4x, but below its historical average of 30.2x.

High P/Es require high EPS growth to sustain them. In the case of The Coca-Cola Company, the company has recently shown 5% Uniform EPS growth.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, The Coca-Cola Company’s Wall Street analyst-driven forecast is for EPS to grow by 12% and 10% in 2023 and 2024, respectively.

Furthermore, the company’s return on assets was 59% in 2022, which is 10x the long-run corporate averages. Also, cash flows and cash on hand consistently exceed its total obligations—including debt maturities and CAPEX maintenance. These signal low dividend risk and low credit risk.

Lastly, The Coca-Cola Company’s Uniform earnings growth is in line with peer averages, and in line with peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research