Moody’s is saying this homebuilder is a bigger credit risk than they were in 2007, but UAFRS says otherwise

Moody’s says this homebuilder is a bigger risk now than they were in 2007. As-reported financials seem to support this conclusion, even after the firm has taken steps to improve its performance. However, both as-reported figures and Moody’s conclusions are wrong.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

One of the biggest catalysts of the Great Recession was housing.

In the several years leading up to the crash, demand for housing was augmented by seemingly cheap mortgages, and homebuilders raced to meet that demand. These companies built up development after development, buying acres and acres of land.

Then it all came crashing down.

In October 2007, right around when the whole market peaked, reports were already circulating about the number of vacant homes in the US. CNN Money reported over two million homes for sale were vacant that month.

Even in great housing markets, the number of vacant homes for sale had risen by over 50% in just a few years. Not only was demand slowly starting to decline, but the market had been flooded with new homes no one wanted to, or possibly could, buy.

Beazer Homes USA, Inc. (BZH) was one of these companies that had overinvested. In 2006, Beazer’s inventory had ballooned from $1.7 billion just a few years earlier, to $3.5 billion. By 2007, that inventory had moderated slightly, but still sat at $2.8 billion, higher than any year prior to 2005.

When the proverbial fat lady sang, Beazer Homes was left holding much less valuable assets. In fact, over the next three years, the firm wrote down over $1.2 billion in assets, nearly half of the balance sheet.

The firm survived, barely. Credit default swaps, a signal of corporate health, jumped north of 2,000bps in 2008, a signal of a company facing bankruptcy.

Coming out the other side, they have been better about managing inventory. In fact, inventories are still at just $1.6 billion, not close to approaching those levels seen in 2006 and 2007.

However, the company is still anemic.

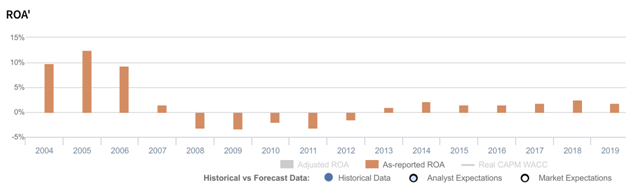

The firm has an ROA of just 2.5%. Since finally recovering to positive levels, as-reported ROA has failed to even approach pre-recession levels.

EBITDA is just $74 million, or almost 90% lower than it was in 2006. Additionally, the firm has $1.2 billion in debt outstanding, nearly as much as they had prior to the Great Recession. All signs would point to a bad business that is in a worse position than they were in 2007.

But those signs are wrong.

After making the required adjustments under UAFRS, it becomes clear that the firm has rebounded nicely. ROA is actually in double-digit territory, as it was pre-recession:

And adjusted EBITDA is up to $171 million, still shy of $550 million-plus peaks in 2006, but not off 90%.

Most importantly though, this name isn’t an imminent bankruptcy risk.

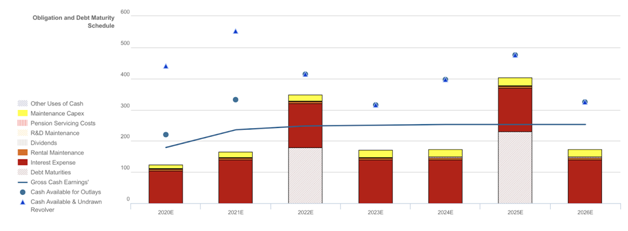

It is true that the firm has a good deal of debt on the balance sheet, but they have managed it well. Looking at adjusted cash flows relative to adjusted obligations, it’s clear Beazer Homes should have limited issues in servicing their upcoming debt headwalls:

Most of the firm’s debt doesn’t even come due in the next seven years.

Moody’s isn’t looking at the right signals, and as a result, is calling Beazer Homes a B3 credit, or junk. They are saying the company is a bigger risk now than they were in 2007 (when they had a Ba2 rating).

Instead, with the right signals, it is clear the firm should be approaching investment grade. In fact, Valens has the firm rated as an IG4, or seven notches higher.

BZH’s Credit Risk Remains Overstated as Cash Bond Markets Continue to Overlook Robust Recovery Rate

Cash bond markets are grossly overstating BZH’s credit risk with a YTW of 13.790% relative to an Intrinsic YTW of 8.280%, while CDS markets are materially overstating credit risk with a CDS of 954bps relative to an Intrinsic CDS of 776bps.

Meanwhile, Moody’s is materially overstating BZH’s fundamental credit risk, with its highly speculative B3 credit rating seven notches lower than Valens’ IG4 (Baa2) rating.

Fundamental analysis highlights that BZH’s cash flows alone would exceed operating obligations in each year going forward.

Additionally, their combined cash flows and expected cash build should meet all obligations including debt maturities going forward, including in 2022 and 2025, when the firm faces material $180 million and $230 million debt headwalls, respectively.

Furthermore, their robust 84% recovery rate should enable access to credit markets to refinance, if necessary. However, BZH’s small market capitalization may inhibit their ability to do so at favorable rates.

Incentives Dictate Behavior™ analysis highlights positive signals for creditors. Management’s compensation framework focuses them on all three value drivers, as well as debt reduction, which should lead to Uniform ROA expansion and increased cash flows available for servicing debt obligations.

Furthermore, management members are material holders of BZH equity relative to their average annual compensation, indicating they are likely well-aligned with shareholders for long-term value creation.

Additionally, management members have low change-in-control compensation, indicating they are not highly incentivized to seek a buyout or sale of the firm, decreasing potential event risk.

Earnings Call Forensics™ of the firm’s Q1 2020 earnings call (1/30) highlights that management generated an excitement marker when saying gross margin was up 10bps, driven by ongoing efforts to simplify product offerings.

In addition, they are confident their strategy targets double-digit ROA by growing EBITDA faster than revenue on a less leveraged balance sheet.

However, management may lack confidence in their ability to pay off $50 million of debt this year and hit their goal of bringing total debt below $1 billion.

Moreover, they may be concerned about their community count cadence, and they may lack confidence in their ability to sustain increases in gross margin and continue to reduce incentives.

Operational sustainability, expected cash build, and a robust recovery rate indicate that credit markets and Moody’s are overstating credit risk.

As such, both a ratings improvement and a tightening of credit market spreads are likely going forward.

SUMMARY and Beazer Homes USA, Inc. Tearsheet

As the Uniform Accounting tearsheet for Beazer Homes USA, Inc. highlights, the company trades at a 5.6x Uniform P/E, which is below global corporate average valuation levels but around historical average valuations.

Low P/E’s only require low—or even negative—EPS growth to sustain them. That said, in the case of Beazer Homes, the company has recently shown -36% Uniform EPS shrinkage.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Beazer Homes’ Wall Street analyst-driven forecast a growth of 51% in 2020 but a decline of 33% in 2021.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $7 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for Beazer Homes, the company would need to have Uniform earnings shrink by 24% or less each year over the next three years.

Wall Street analysts’ expectations for Beazer Homes’ earnings growth are far above what the current stock market valuation requires in 2020 and 2021.

In addition, Beazer Homes’ Uniform earnings growth is the highest among peers and the company is trading below peer valuations.

Also, the company’s earnings power is 2x corporate averages, signaling very low risk to its dividend or operations.

To summarize, Beazer Homes USA, Inc. is expected to see significant Uniform earnings growth in 2020, which is expected to continue in 2021. Furthermore, the company is trading below average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research