This oft-forgotten healthcare firm plays a boring yet critical part in today’s healthcare landscape

Logistics are increasingly important in a globalized interconnected world, and the healthcare industry is no different. An ever-growing number of new drugs and treatments can leave a hospital overwhelmed.

However, this massive medical supply company removes the headache and improves efficiency in the U.S. healthcare system.

Additionally, the cleaned up Uniform Accounting metrics highlight a more compelling story than investors might suspect from an initial glance.

Also included below are the company’s Uniform Accounting Performance and Valuation Tearsheet.

Investor Essentials Daily:

Tuesday Tearsheets

Powered by Valens Research

When people think of the healthcare industry, they think of either the doctor they go to, the hospital they have been to, or the medications they take.

Therefore, when people think of healthcare investing, they think of pharma companies or medical device companies, companies that are directly involved at the point of care.

However, all of these businesses rely on one, often overlooked, group of companies to keep the healthcare system functioning. Healthcare distributors, like Cardinal Health (CAH), make sure that hospitals have the right drugs and right equipment to take care of their patients.

For pharmaceuticals alone, there are over 1,300 manufacturers and over 180,000 points of distribution. That doesn’t even include the long list of medical products that a hospital needs for everyday operations.

Imagine if each hospital had to figure out that logistical nightmare on its own. Instead, with Cardinal Health, hospitals do not have to contract with each supplier, and they do not have to hold months’ worth of inventory for every single procedure and service.

Inversely, Cardinal Health makes the supplier’s job easier since the suppliers don’t have to form agreements with every individual hospital and healthcare provider.

Cardinal Health is the connector between healthcare suppliers and healthcare providers and by doing so increases the system’s efficiency. Cardinal Health can do so efficiently because of its massive scale—nearly 90% of U.S. hospitals, 29,000 pharmacies, and 6,200 labs use its services.

This large scale allows the healthcare distributor to negotiate better prices and centralize the supply chain, reducing the total amount of inventory in the healthcare system.

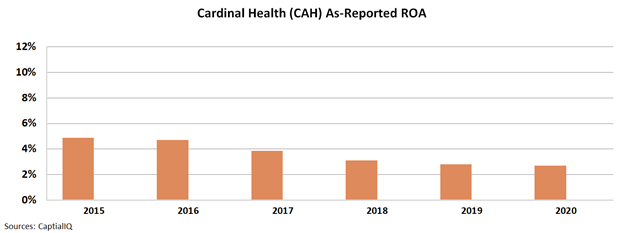

Given Cardinal Health’s importance to the U.S. healthcare system, it’s surprising it only appears to have generated a miserly sub-5% return on assets (ROA). Its as-reported ROA even went as low as 3% in 2020.

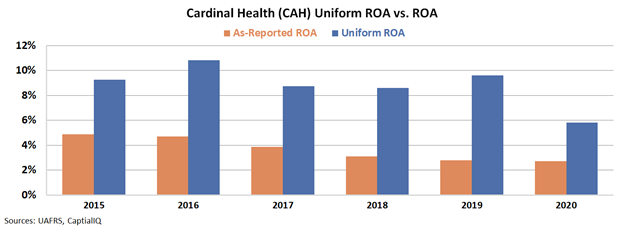

In reality, when we use Uniform Accounting metrics we see that this is not an accurate representation of Cardinal Health’s true profitability.

Once we adjust for these significant distortions, we see that Cardinal Health’s essential services lead to a healthy return.

Uniform ROA remained around 9%-11% levels from 2015 to 2019 and only dropped in 2020 due to the COVID-19 pandemic. In each of these years, Uniform ROA was more than twice what as-reported ROA was.

See for yourself:

Using our Uniform Accounting framework, investors can see how Cardinal Health is a much more profitable business than as-reported numbers would lead you to believe. The firm is central to the American healthcare system and generates a solid return given that importance.

GAAP-based analysis leaves investors with an inaccurate picture and essentially amounts to guesswork as to which companies are vital in their fields.

SUMMARY and Cardinal Health, Inc. Tearsheet

As our Uniform Accounting tearsheet for Cardinal Health, Inc. (CAH:USA) highlights, the Uniform P/E trades at 14.5x, which is below the global corporate average of 23.7x and its own historical P/E of 15.7x.

Low P/Es require low EPS growth to sustain them. In the case of Cardinal Health, the company has recently shown a 41% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Cardinal Health’s Wall Street analyst-driven forecast is a 66% and 22% EPS growth in 2021 and 2022, respectively.

Based on the current stock market valuations, we can use earnings growth valuation metrics to back into the required growth rate to justify Cardinal Health’s $57 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 3% annually over the next three years. What Wall Street analysts expect for Cardinal Health’s earnings growth is above what the current stock market valuation requires in 2021 and 2022.

Furthermore, the company’s earning power is slightly above the long-run corporate average. Also, cash flows and cash on hand are over 2x its total obligations—including debt maturities, capex maintenance, and dividends. Meanwhile, intrinsic credit risk is 90bps above the risk free rate. All in all, this signals a low dividend and credit risk.

To conclude, Cardinal Health’s Uniform earnings growth is in line with its peer averages, and the company is trading around its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research