Calls for a recession appear premature

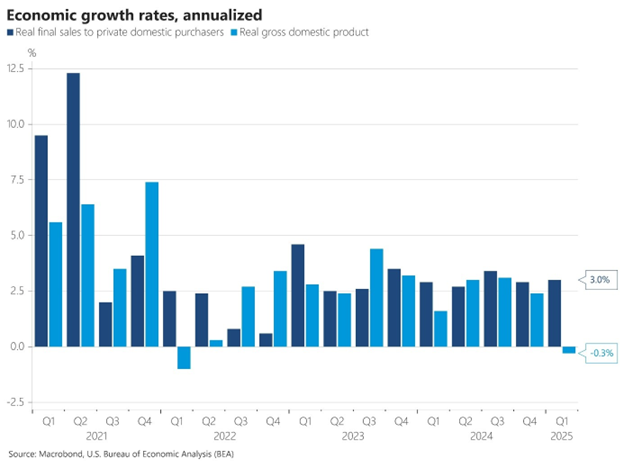

First quarter GDP fell 0.3%, but that drop was driven almost entirely by a 41% surge in imports ahead of tariff fears and a 5.1% cut in federal spending.

When you strip out trade and government noise, real final sales to private domestic purchasers rose 3%, with business investment up nearly 22% and consumer spending up 2%.

In other words, the core economy, households buying and companies investing, remains on solid footing, making recession calls premature.

Investor Essentials Daily:

The Monday Macro Report

Powered by Valens Research

Last week, the U.S. economy shrank for the first time in three years. In the first quarter of 2025, real GDP fell by 0.3%.

Markets didn’t take it well. The S&P 500 dropped more than 2% within the first hour last Wednesday. Investors assumed the long-feared recession had finally arrived.

GDP is calculated using a formula that factors in multiple components beyond production or spending. And one input distorted the entire reading.

Imports rose 41.3% in Q1. It was the biggest spike in five years. Companies scrambled to front-load shipments ahead of expected tariffs under the Trump administration.

Imports subtract from GDP because they reflect dollars flowing out of the domestic economy. When businesses import more goods, that drags down GDP.

Exports barely moved at just 2% growth. Because of how GDP is calculated, that imbalance alone knocked nearly five percentage points off the headline GDP number.

When we focus on core domestic activity, the picture is far more stable.

Real final sales to private domestic purchasers, which removes the noise of inventories, trade, and government outlays, rose 3.0%.

Take a look…

That’s a solid number. And it’s consistent with how the economy has performed over the past several years.

Private investment surged nearly 22%, driven by business equipment investments. Consumer spending increased by a modest 2%. These are the indicators of real economic momentum.

The government component, by contrast, declined. Federal spending fell at a 5.1% annualized pace.

That was the other major drag on the GDP total. This reflected early-term spending cuts from the new administration.

GDP is often treated as a temperature check on growth. But this reading was skewed by temporary behaviors tied to policy.

The first quarter is rarely a great one. It comes right after the holiday season, and fiscal years tend to start out slow.

That said, when you remove the tariff noise, this year’s first quarter was overwhelmingly fine.

The underlying engine of the economy, consumers and businesses, hasn’t stalled.

Companies are still investing, households are still spending, and there’s no sign that credit markets or liquidity conditions are under stress.

Policy changes and trade friction can create noise in quarterly data. But investors who focus only on top-line GDP are likely to miss the signal.

Recession calls seem premature for now.

This quarter’s decline was driven by trade distortions and government policy shifts. Private-sector fundamentals don’t seem to be coming apart just yet.

The smartest investors will look through it and stay focused on what actually drives growth and they’ll treat these kinds of selloffs as buying opportunities.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research