Investors think this company’s fleet of assets means its debt is safe, but historical analysis and Credit Cash Flow Prime analysis say differently

Investors were caught off guard when MLPs—one of the most stable investment classes—struggled during the Great Recession. Banks were lending on the wrong metrics, and it had disastrous results.

Today, we’re highlighting another company investors are pricing as nearly risk-free, and showing you why that isn’t the case.

Below, we show how Uniform Accounting restates financials for a clear credit profile.

We also provide the equity tearsheet showing Uniform Accounting-based Performance and Valuation analysis of the company.

Investor Essentials Daily:

Wednesday Credit Insights

Powered by Valens Research

We often talk about how every recession throughout history began with a credit crunch.

A combination of overly-ambitious borrowers and lax lending standards end up putting many borrowers in a situation where they can’t refinance, which sends ripples through the economy.

After so many recessions, you’d think one of the parties—either banks or borrowers—would have figured out how to prevent such a thing from happening again.

This is easier said than done, especially with perfect hindsight but far weaker foresight.

There’s a great example from the Great Recession where banks, corporations, and investors all thought they were safe. An industry known for its stability was brought to a near halt because they were focusing on the wrong metrics.

Master Limited Partnerships, or MLPs, are among the most stable public investments. Much like a REIT, an MLP generates income from a stable set of assets, often assets like oil pipelines and storage.

They also have to pay the majority of their earnings as tax-advantaged distributions, which makes MLPs a good dividend investment assuming prices stay stable.

Despite how “safe” and stable the MLP business tends to be, the industry was crushed during the Great Recession.

You see, banks chose to lend to MLPs based on the value of their assets, not their ability to service debt maturities via their cash flows. MLPs have long-term assets, so they should ideally take on long-term debt.

Unfortunately, banks offered much lower rates for short-term debt, which many MLPs chose to take the banks up on to finance their businesses. This decision was fine as long as cash flows remained steady, but it became disastrous once those cash flows dried up.

Entering 2008, many MLPs had debt coming due that they could not pay off. Additionally, the energy industry took a big hit during the recession, which slashed cash flows for the MLP industry.

When the companies approached the banks to refinance their debt as they always had, they were turned away and allowed to fall into distress.

While the MLP industry is a great example, there are many other industries reliant on constantly refinancing their debt, and investors are not being compensated for the added risk.

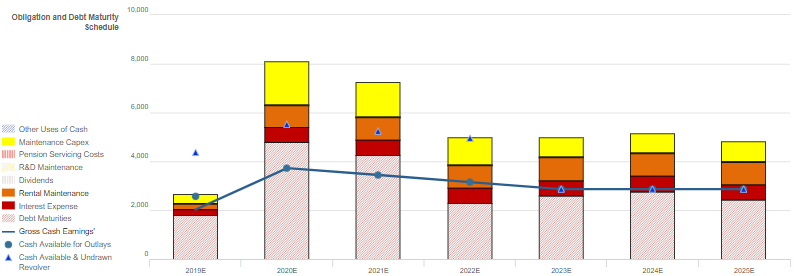

Avis Budget Group (CAR) is another great example. As you can see in the chart below, Avis Budget has consistent and material debt maturities that it will have to refinance to sustain the business.

The company’s current system is reliant on its rental car ownership structure. These are tangible assets that continuously replenish as Avis Budget updates its fleet, and many of the cars have guaranteed buyback prices from the manufacturers.

Since the cars have a fixed price, banks are willing to continue lending even if Avis Budget doesn’t have the cash flows to meet current obligations.

However, this system will continue working only as long as car prices stay stable. Car manufacturers realize they have little incentive to offer such generous buyback prices and have been eager to exit the practice. As this continues, companies like Avis Budget become more reliant on used car prices as a proxy for its collateral.

Over the last six months, used car prices have been declining, which only adds risk that banks will be less willing to lend to Avis Budget. If this continues, the company doesn’t even need a debt crisis to be in trouble.

While it would take a large shock to used car prices to fully scare off the banks, this risk is not being priced in at all for credit holders. This is apparent only when we look at the Credit Cash Flow Prime above.

Once we make the proper adjustments to Avis Budget’s cash flows and annual obligations using Uniform Accounting, we can see that bond yields are far too low. As-reported yields are as low as 1.682% indicating investors are pricing in nearly no risk. That said, Valens’ Intrinsic YTW on the same bond is nearly 100bps higher at 2.652%

It’s easy to get caught off guard by unforeseen risk when using as-reported financial metrics. This shows that credit may not always be as risk-free as it seems.

Credit Markets Continue to Downplay CAR’s Consistent Material Debt Maturities; Wider Spreads Warranted

Credit markets are understating risk with a CDS of 217bps and a YTW of 1.682% relative to an iCDS of 297bps and an intrinsic YTW of 2.652%.

Meanwhile, S&P is understating credit risk with its non-investment grade speculative BB rating three notches above Valens’ HY2 (B) rating.

Fundamental analysis highlights that CAR should have cash flows in excess of operating obligations in each year going forward. However, with consistent material debt maturities beginning this calendar year, including a $4.8bn headwall in 2020, the firm will be unable to service all obligations, and will need to refinance in order to avoid a liquidity crunch.

Moreover, CAR’s neutral 40% recovery rate on unsecured debt implies they may have difficulty accessing credit markets at favorable rates.

Incentives Dictate Behavior™ analysis highlights mostly positive signals for creditors.

Management’s compensation framework focuses on improving revenue growth and margins, but may incentivize management to drive growth by overspending on capex and working capital.

Moreover, most NEOs are material holders of CAR equity relative to their annual compensation, indicating they are likely to align with shareholders for long-term value creation.

Furthermore, management members are not well compensated in a change-in-control event, meaning that they are not likely to pursue a sale of the company, decreasing event risk for creditors.

Earnings Call Forensics™ of the firm’s Q3 2019 earnings call (11/1) highlights that management may lack confidence in their ability to sustain improvements in their net promoter score, and they may be exaggerating the value customers derive from the Avis mobile app.

Furthermore, they may be concerned about the sustainability of growth in the Zipcar Flex product and about the value of their airline partnerships.

Finally, they may lack confidence in their ability to leverage fleet data to make purchasing decisions, drive development in their alternative channels, and reduce fleet costs through their sales program. `

Consistent, material debt maturities and a lackluster recovery rate suggest S&P and credit markets are understating CAR’s underlying credit risk. As such, a ratings downgrade and a widening of credit spreads are likely going forward.

SUMMARY and Avis Budget Group, Inc. Tearsheet

As the Uniform Accounting tearsheet for Avis Budget Group, Inc. (CAR) highlights, the company’s Uniform P/E trades at 18x, which is below global corporate average valuation levels but above historical average valuations.

Low P/E’s require low—or even negative—EPS growth to sustain them. In the case of Avis, the company has recently seen its Uniform EPS to decline by 54%, which may be a signal that below-average valuations are justified.

Wall Street analysts provide stock and valuation recommendations that in general provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Avis’ Wall Street analyst-driven EPS growth forecast goes from a -165% in 2019 to an even lower -182% in 2020

Based on current stock market valuations, we can back into the required earnings growth rate that would justify $48 per share. These are often referred to as market embedded expectations. In order to meet the current market valuation levels for Avis, the company would have to have Uniform earnings shrink by 6% each year over the next three years.

Considering a weak year this year, Wall Street analysts’ expectations for Avis earnings growth are far below what the current stock market valuation requires.

In addition to Avis valuations being low, its Uniform P/E is at peer average levels, while its Uniform EPS growth is below peer averages.

Meanwhile, the company’s earnings power is in line with corporate averages, signaling an average risk to its dividend or operations.

To summarize, Avis Budget Group Inc. is a below average profitability company with significantly low earnings growth potential and muted embedded expectations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research