Cathie Wood’s flagship fund has had an awful year. Here’s why

With a 153% return in 2020, Cathie Wood’s flagship ARK Innovation ETF became an overnight cult favorite.

But now that the fund is down 35% from its highs, funds are flowing out rather than in, and its longtime investors are left wondering: what’s going on?

To better understand why Wood’s fund has been under so much pressure, let’s use Uniform Accounting to perform a portfolio audit of her largest holdings and answer a simple question – Are her biggest bets priced for outsized growth?

Also below, a detailed tearsheet of the fund’s largest holding.

Investor Essentials Daily:

Friday Uniform Portfolio Analytics

Powered by Valens Research

A little over three years ago, Cathie Wood sat on a CNBC panel and claimed Tesla (TSLA) would become a $700 billion dollar company, with a pre-split $4,000 stock price.

The other panelists peppered her with doubts and whataboutisms, all concealing smirks as they could barely take her bull case seriously.

Famed investor and Shark Tank host Kevin O’Leary posited that if Tesla “walks and talks like a car, then it must be a car.” He claimed that either Tesla will need to return to the 16x P/E of General Motors (GM), or the GM will need to skyrocket in valuation to match Tesla’s 300x P/E levels. He said, “one of those things has to happen.”

Cathie Wood calmly responded by laying her bull thesis out.

She claimed Tesla is fundamentally different from the legacy automakers because it acts more like a software company than a hardware company. She claimed that the future of transportation will be electric, while the legacy automakers were still fully invested in gasoline engines. She claimed that over-the-air updates will help the Model 3 become a fundamentally better product than the competition.

In another CNBC interview several months later, as pre-split TSLA shares traded at $270, she was asked about Elon Musk’s tweet that he was considering taking the company private at $420 per share.

Rather than claiming that the $420 tweet was just a joke, she explained that taking the company private at $420 per share would be lunacy given that her models, which she had sent over to the Tesla board, placed the present value of the company at $2,000 per share.

Tesla is currently worth $800 billion dollars, with a pre-split stock price of $3,200.

This speaks to what investors have realized about Cathie Wood’s investing core competency: She is able to identify innovation ahead of the market.

Tesla was just one of her blockbuster success stories. She also identified Square (SQ) long before it became one of the most expensive companies in the investing universe, along with a Rolodex of other companies that became multibaggers for her various targeted funds.

When Wood bets, she bets big. Her monumental success in 2020 gained her a cult-like following, especially among the Reddit WallStreetBets types, who are also known for making large bets on risky positions.

2021, however, marked a different story for Cathie Wood. After her flagship innovation fund, ARK Innovation (ARKK), plunged over 20% over the course of four weeks from its February highs, the record inflows became record outflows. ARKK has traded sideways to down since.

Recent headlines have not been helping the ARK Invest story. Between Michael Burry’s $30 million purchase of puts against ARKK, her genomics-focused fund ARKG buying up Crispr shares immediately ahead of a 9% plunge, and her sale of a sizable chunk of ARK’s Tesla position, the Cathie Wood high seems to have worn off.

But she remains bullish. For example, as journalists, investors, and management teams worry about inflation, Wood believes it is a non-issue, and that deflation is a more likely outcome amid the urban exodus to lower cost-of-living cities.

Similarly, as various investors claim that the market is overheated and deep within bubble territory, Wood recent went on record saying:

“Many people ask me, are we in a bubble? We couldn’t be further from it. I do not believe that the average investor understands how provocative the next five to fifteen years as [markets] enter exponential growth trajectories that we have never seen before”

Given Cathie Wood’s bullishness, let’s examine her ten largest ARKK holdings under the Uniform Accounting lens. This will help us understand what the market may be missing about her biggest bets, and what sort of growth is already priced into their current valuations.

One cornerstone of the ARK Invest strategy is to invest in companies that aren’t profitable, but are setting themselves up for explosive future growth.

This was exactly the premise behind the company’s bet on Tesla, and is currently its thesis for dozens of others.

To some, the strategy appears to be a shot-in-the-dark bet that a company’s technology investments will one day bring their return on assets (ROA) positive, should the technology be as revolutionary as the company may claim.

The truth, however, is that many of these “unprofitable” companies generate better returns than as-reported metrics imply. Economic productivity, which is just a measure of a company’s use of resources, is massively misunderstood on Wall Street. This is reflected by the 130 distortions in the Generally Accepted Accounting Principles (GAAP) that make as-reported results poor representations of real economic productivity.

These distortions include the poor capitalization of R&D, the use of goodwill and intangibles to inflate a company’s asset base, a poor understanding of one-off expense line items, and flawed acquisition accounting.

It is no surprise that once many of these distortions are accounted for, many of the companies that Cathie Wood invests in are actually robustly profitable, but most investors wouldn’t realize it.

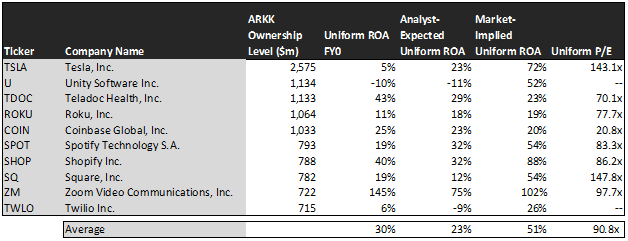

The average as-reported ROA among ARKK’s top ten names is a lackluster 1%, which implies to investors that these companies are generating less economic value than the cost of capital. In reality, these companies perform far better, with a 30% Uniform ROA.

Teladoc Health (TDOC), for example, doesn’t return -3% ROA per year. It actually boasts 43% ROA, in line with what a software-enabled tech company can reasonably be expected to do. The dislocation is primarily caused by the company’s use of stock option compensation, which unfairly deflates earnings.

Similarly, Shopify (SHOP) does not have 2% ROAs. As an e-commerce platform with a tiny asset base, it actually has a 40% ROA.

These dislocations demonstrate that ARK Invest chooses high-quality companies to invest in. But there is another crucial step in the search for alpha. Investors need to also find companies that are performing better than their valuations imply.

Valens has built a systematic process called Embedded Expectations Analysis to help investors get a sense of the future performance already baked into a company’s current stock price. Take a look:

This chart shows four interesting data points:

- The Uniform ROA FY0 represents the company’s current return on assets, which is a crucial benchmark for contextualizing expectations.

- The Analyst-Expected Uniform ROA represents what ROA is forecast to be over the next two years. To get the ROA number, we take consensus Wall Street estimates and we convert them to the Uniform Accounting framework.

- The market-implied Uniform ROA is what the market thinks Uniform ROA is going to be in the three years following the analyst expectations, which for most companies here is 2023, 2024, and 2025. Here, we show the sort of economic productivity a company needs to achieve to justify its current stock price.

- The Uniform P/E is our measure of how expensive a company is relative to its Uniform earnings. For reference, average Uniform P/E across the investing universe is roughly 24x.

Embedded Expectations Analysis of ARKK paints a clear picture of the fund: The stocks it holds are expensive.

While analysts expect average ROA to decline from 30% to 23%, the market is pricing these companies to grow their economic profitability to 51%.

While some companies are able to achieve profitability in the 50%-100% range (and a select few can go even higher), these sorts of returns are typically reserved for high-growth startup-stage businesses, or companies that operate with incredibly light asset bases.

A company like Tesla, which manufactures and sells cars, is unlikely to achieve the 72% Uniform ROAs expected of it, as it makes heavy investments into physical assets like factories.

Cathie Wood’s thesis on Tesla involves its transition to transportation-as-a-service enabled by the company’s initiation of a massive “robotaxi” fleet and subscription revenues for its full self-driving service.

But even if those predictions come true, no company as asset-intense as Tesla can be reasonably expected to reach 72% ROA. The 23% ROA that analysts predict for 2022 is far more realistic, and still represents a significant improvement over current levels.

But if the company fails to achieve the 72% ROAs expected of it, investors may find themselves disappointed.

A similar story applies to a number of the other names ARKK holds. With an average Uniform P/E of 90.8x excluding companies with negative earnings, Cathie Wood has chosen some of the most expensive names on Wall Street, which can be a red flag for investors.

This isn’t to say that companies cannot stay expensive for extended periods. The market is far from rational and doesn’t have the crystal-clear visibility into performance and expectations that our team at Valens does. But investors need to be warned that investing in these sorts of names comes with tremendous downside risk should they fail to meet their embedded expectations.

This can partly explain why ARKK has seen high highs…and low lows.

This just goes to show the importance of valuation in the investing process. Finding innovative, high-quality firms is a crucial first step to long-term success. But getting those names at an attractive price is equally important.

To see a list of companies that have great performance and innovation but also attractive valuations, click here to get access to the Valens Conviction Long List.

Read on to see a detailed tearsheet of ARKK’s largest holding.

SUMMARY and Tesla, Inc. (TSLA:USA)

As one of ARK Innovation’s largest individual stock holdings, we’re highlighting Tesla’s tearsheet today.

As the Uniform Accounting tearsheet for Tesla, Inc. (TSLA:USA) highlights, its Uniform P/E trades at 141.3x, which is above the global corporate average of 24.3x and its own historical average of 108.1x.

High P/Es require high EPS growth to sustain them. In the case of Tesla, the company has recently shown a 27% Uniform EPS decline.

Wall Street analysts provide stock and valuation recommendations that, in general, provide very poor guidance or insight. However, Wall Street analysts’ near-term earnings forecasts tend to have relevant information.

We take Wall Street forecasts for GAAP earnings and convert them to Uniform earnings forecasts. When we do this, Tesla’s Wall Street analyst-driven forecast is for EPS to grow by 1,177% and 66% in 2021 and 2022, respectively.

Based on current stock market valuations, we can back into the required earnings growth rate that would justify Tesla’s $794 stock price. These are often referred to as market embedded expectations.

The company is currently being valued as if Uniform earnings were to grow by 102% annually over the next three years. What analysts expect for Tesla’s earnings growth is above what the current stock market valuation requires for 2021, but below the requirement in 2022.

Furthermore, the company’s earning power is below the long-run corporate averages. However, cash flows and cash on hand are 3x its total obligations—including debt maturities and capex maintenance. Moreover, Tesla’s intrinsic credit risk is 10 bps above the risk free rate. Together, these signal a low credit risk.

Lastly, Tesla’s Uniform earnings growth is above its peer averages, and the company is also trading above its average peer valuations.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Strategist &

Director of Research

at Valens Research