This cereal company might be in trouble

Investors are looking at defensive stocks like Post Holdings (POST) amid recession fears due to its diversified and historically stable consumer foods business.

Post operates in cereals, refrigerated foods, food service products, and pet food, using acquisitions to drive growth.

However, declining cereal demand, increased consumer preference for healthier food, and recent closures of manufacturing plants raise significant concerns.

The market expects profitability to fall, reflecting justified caution about Post’s future despite its strong cash flow and disciplined management.

Investor Essentials Daily:

Wednesday News-based Update

Powered by Valens Research

In the face of ongoing market uncertainty and lingering recession concerns, investors have increasingly turned to defensive stocks even after tariffs were delayed for 90 days.

Post Holdings (POST) has established itself as one of the most stable consumer staple businesses in the market over the past two decades.

The company operates across multiple food categories with a significant presence in breakfast cereals, refrigerated foods, food service products, and more recently, pet food.

Consumer brands is the company’s largest unit, accounting for over half of revenue, and includes well-known cereal brands like Honey Bunches of Oats, Pebbles, and Grape-Nuts.

This segment also houses the company’s growing pet food operations.

The foodservice segment provides egg and potato products primarily to restaurants, educational institutions, and commercial food service distributors.

This segment has shown strength in both egg and potato categories with particular success in higher value-added goods.

The refrigerated retail segment focuses on refrigerated side dishes, sausage products, and other protein-rich offerings and has been strategically shifting toward higher-margin products.

Weetabix, the British cereal brand acquired in 2017, provides Post with international exposure and a strong presence in the UK breakfast market.

This diversified approach has allowed Post to weather various market conditions effectively.

When one segment faces challenges, others often compensate, providing earnings stability that investors particularly value during uncertain economic times.

Post operates with an almost private equity-like approach to its portfolio management.

The company has a proven track record of acquiring brands, optimizing their operations, and extracting value through improved efficiencies.

The company maintains what management describes as a “very deep” M&A pipeline while remaining disciplined on valuation, typically targeting medium-term low-teens return profiles from its acquisitions.

Post holds strong market positions in several of its categories, particularly in breakfast cereals, where it maintains the third-largest market share in the U.S. behind Kellogg and General Mills.

Despite these considerable strengths, the company does face some significant challenges.

Post recently announced plans to close two of its cereal manufacturing facilities in Ontario and Nevada.

These closures are part of a broader effort by the company to trim excess capacity amid declining consumer demand for cereal products.

Demand for cereal is steadily declining, driven by shifting consumer preferences toward healthier food options and more convenient breakfast alternatives.

Department of Health and Human Services Secretary Robert F. Kennedy Jr. has publicly advocated for healthier food policies, placing additional pressure on companies like Post, whose product portfolios heavily feature cereals and packaged foods that are often high in sugar and processed ingredients.

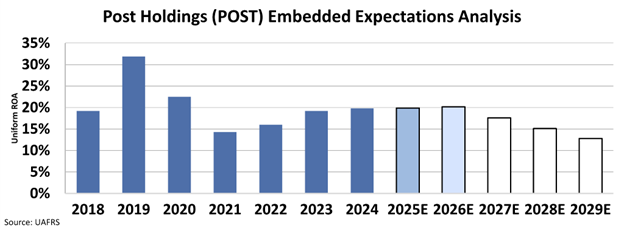

Current market expectations reflect significant skepticism about Post’s ability to maintain steady returns moving forward.

Our EEA model clearly shows this.

The EEA starts by looking at a company’s current stock price. From there, we can calculate what the market expects from the company’s future cash flows. We then compare that with our own cash-flow projections.

In short, it tells us how well a company has to perform in the future to be worth what the market is paying for it today.

At the current stock price, the market expects the company’s Uniform return on assets ”ROA” to decline to 13% from 20% last year.

Post’s recent financial results paint a picture of a company struggling with organic growth while maintaining relatively stable earnings.

The company reported a mere 0.4% year-over-year growth in the latest earnings, suggesting a slight organic decline.

While the foodservice segment benefited from higher volumes and egg pricing, these gains were offset by declines across other segments.

Pet food sales dropped, side dish volumes decreased, and Weetabix experienced reduced non-biscuit and private label sales.

Distribution losses in cheese and egg products further hampered performance.

While Post continues to offer attractive fundamentals in terms of strong cash generation and disciplined capital management, the significant structural challenges facing its core cereal business and broader market pressures suggest that the current cautious market sentiment might indeed be justified.

Best regards,

Joel Litman & Rob Spivey

Chief Investment Officer &

Director of Research

at Valens Research